Iryna Tolmachova/iStock Editorial through Getty Photos

Funding Thesis: Income and earnings development for Loblaw Firms Restricted has been encouraging. Nonetheless, I take the view that an enchancment briefly and long-term stability sheet metrics would make for a stronger bullish case within the inventory going ahead.

Loblaw Firms Restricted (TSX:L:CA) is a number one Canadian retailer that serves as one of many largest meals distributors within the nation, in addition to working throughout the well being, style and funds sectors.

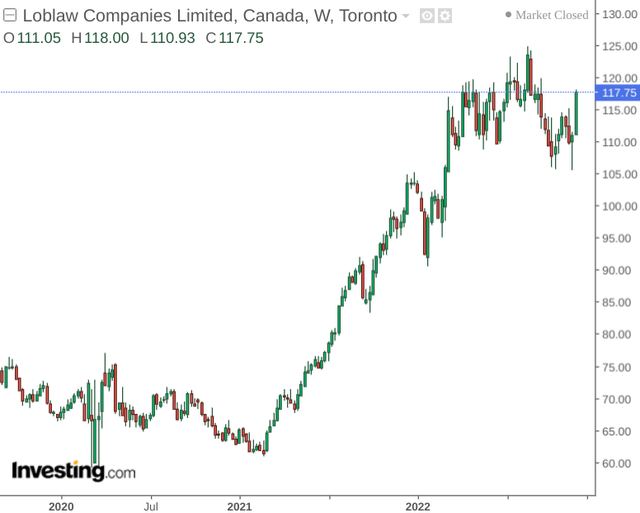

As we are able to see, the inventory noticed sturdy upside in 2021, however has seen kind of stationary efficiency this 12 months.

investing.com

The aim of this text is to evaluate whether or not the inventory may begin to see upside as soon as once more, taking latest efficiency and macroeconomic situations into consideration.

Efficiency

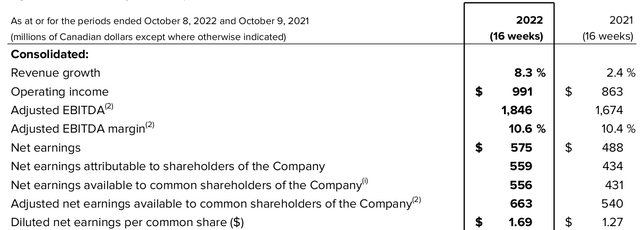

When Q3 2022 efficiency, we are able to see that diluted earnings per share noticed a powerful enhance as in comparison with the identical interval for 2021.

Loblaw Firms Restricted: 2022 Third Quarter Report back to Shareholders

Moreover, earnings are considerably increased as in comparison with the CAD $0.90 degree as seen for Q3 2019.

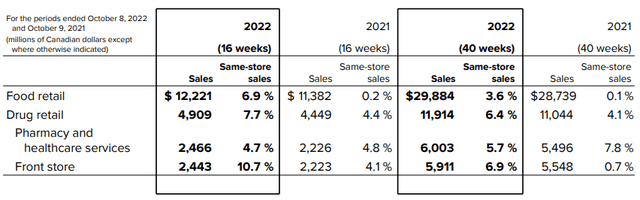

When gross sales efficiency throughout the retail section, we are able to see that over a 40-week interval – the Drug retail section noticed essentially the most development on an absolute foundation, with the entrance retailer exhibiting essentially the most share development of 6.9%.

Loblaw Firms Restricted: 2022 Third Quarter Report back to Shareholders

With that being mentioned, meals retail gross sales are nonetheless up strongly by 6.9% on a 16-week foundation. For context, the corporate had solely seen development of 0.1% on a 16-week foundation from Q3 2018 to Q3 2019. On this regard, it doesn’t seem as if inflationary pressures have dampened demand on the a part of shoppers – income continues to develop at a wholesome tempo.

From a stability sheet standpoint, we are able to see that the corporate’s fast ratio (calculated as complete present belongings much less inventories throughout complete present liabilities) has remained at 0.75.

| October 2021 | October 2022 | |

| Complete present belongings | 12,010 | 13,014 |

| Inventories | 5,214 | 5,763 |

| Complete present liabilities | 9,002 | 9,709 |

| Fast ratio | 0.75 | 0.75 |

Supply: Figures sourced from Loblaw Firms Restricted 2022 Third Quarter Report back to Shareholders. Figures supplied in tens of millions of Canadian {dollars}, besides the fast ratio. Fast ratio calculated by creator.

Whereas the truth that the fast ratio has not decreased is encouraging – it might be preferable to see the ratio rise above 1 – as this is able to point out that the corporate has greater than enough liquid belongings to satisfy its present liabilities. Certainly, I take the view that buyers could begin to pay extra consideration to such stability sheet metrics over income development going ahead, as a way to be sure that the corporate is successfully changing income development into money stream.

We will see that when evaluating Q3 2019 with Q3 2022 – the long-term debt to complete belongings ratio has additionally risen barely.

| Q3 2019 | Q3 2022 | |

| Lengthy-term debt | 6,105 | 6,978 |

| Complete belongings | 35,463 | 37,695 |

| Lengthy-term debt to complete belongings ratio | 0.17 | 0.19 |

Supply: Figures sourced from Loblaw Firms Restricted 2019 and 2022 Third Quarter Report back to Shareholders. Figures supplied in tens of millions of Canadian {dollars}, besides the long-term debt to complete belongings ratio. Lengthy-term debt to complete belongings ratio calculated by creator.

Whereas Loblaw Firms Restricted has continued to point out sturdy income and earnings development – it’s my view that an enchancment in sure stability sheet metrics would offer a stronger case for upside.

Wanting Ahead

Going ahead, Loblaw Firms Restricted ought to be in a superb place to face up to inflationary pressures, given its dominant function throughout the Canadian retail business and inspiring income development up to now.

With that being mentioned, there’s the danger that the sturdy efficiency now we have been seeing has been artificially lifted by inflation – as opponents have additionally seen stronger efficiency on account of rising costs.

It’s unclear whether or not the rationale for the enhance in gross sales development is linked to inflation, or what particular product classes are resulting in increased income. Consequently, there’s all the time the likelihood {that a} plateau in inflation may additionally result in a plateau in income development.

Conclusion

To conclude, Loblaw Firms Restricted has seen sturdy income and earnings development. Nonetheless, it’s unclear as to what portion of the sturdy efficiency now we have been seeing has been linked to inflation, and whether or not such efficiency may plateau within the brief to medium-term.

Moreover, whereas earnings development has been encouraging, I take the view that an enchancment briefly and long-term stability sheet metrics would make for a stronger bullish case within the inventory going ahead.