The foreign exchange markets are quite regular in Asia right now. Whereas shares in China and Hong Kong extending final week’s sturdy rebound, Aussie and Kiwi usually are not following for now. Some merchants are on guard to rumors of reopening in China, particularly with a district in Guangzhou nonetheless extending powerful lockdown. The financial calendar is relative gentle this week. Predominant focus will probably be on client inflation knowledge within the US.

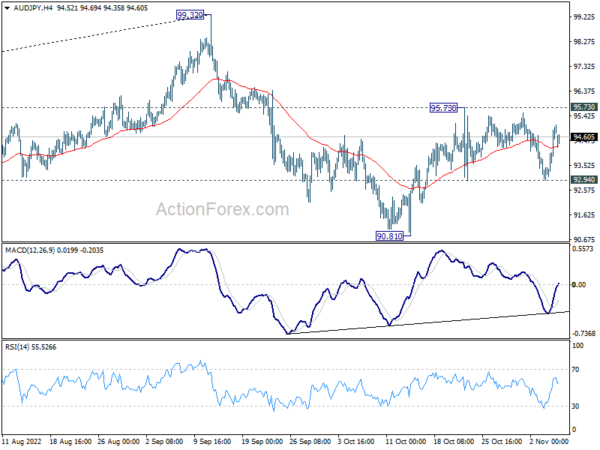

Technically, it’s doable that AUD/JPY’s consolidation from 95.73 has accomplished with three waves to 92.94. That’s, rebound from 90.81 is perhaps able to resume. Break of 95.73 resistance will verify this case and goal 99.32 excessive. For now, a break of 99.32 isn’t envisaged given the specter of intervention in USD/JPY. However that might rely upon the momentum in AUD/USD upon breaking via 0.6521 resistance to finish a head and will backside sample.

In Asia, on the time of writing, Nikkei is up 1.30%. Hong Kong HSI is up 3.42%. China Shanghai SSE is up 0.46%. Singapore Strait Instances is up 0.21%. Japan 10-year JGB yield is down -0.0074 at 0.250.

China exports dropped -0.3% yoy in Oct, imports down -0.7% yoy

In USD time period, China’s exports dropped -0.3% yoy to USD 298.37B in October, properly under expectation of 4.3% yoy. That’s the worst efficiency since Could 2020.

Imports dropped -0.7% yoy to USD 213.22B, under expectation of 0.1% yoy. That’s the the worst since August 2020.

The simultaneous contraction in each exports and imports was the primary since Could 2020.

Commerce surplus widened barely from USD 84.74B to USD 85.15B, wanting expectation of USD 95.95.

US CPI to focus on a “comparatively” gentle week

US CPI highlights a “comparatively” gentle week. Fed Chair Jerome Powell indicated clearly that tightening tempo may sluggish as quickly as in December, however the terminal price could possibly be greater than earlier anticipated. Chicago Fed President Charles Evans later mentioned the projection of peak price is perhaps revised “barely greater” within the upcoming forecasts. However in spite of everything, the trail will stay closely knowledge dependent, particularly on whether or not inflation reveals extra indicators of cooling.

Different knowledge to be watched intently embody US U of Michigan client sentiment; Eurozone Sentix investor confidence, UK GDP. In time period of central financial institution actions, BoJ will publish abstract of opinions. ECB will publish month-to-month bulletin.

Listed here are some highlights for the week:

- Monday: China commerce stability; Swiss unemployment price, international forex reserves; Germany industrial manufacturing; Eurozone Sentix investor confidence.

- Tuesday: Australia AiG companies, Westpac client sentiment, NAB enterprise confidence; New Zealand inflation expectations; Japan common money earnings, family spending, main indicators, BoJ abstract of opinions; France commerce stability; Eurozone retail gross sales.

- Wednesday: Japan present account, financial institution lending; China CPI, PPI; US wholesale inventories.

- Thursday: Australia MI inflation expectations, UK RICS home value stability; ECB financial bulletin; US CPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing index; Japan PPI; Germany CPI closing; UK GDP, manufacturing, commerce stability, NIESR GDP estimate; US U of Michigan client sentiment.

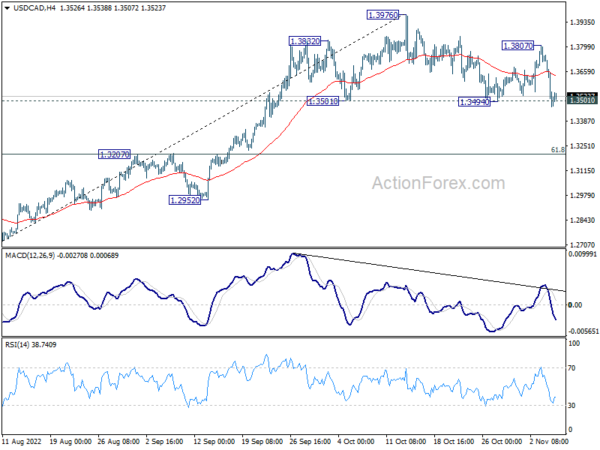

USD/CAD Every day Outlook

Every day Pivots: (S1) 1.3383; (P) 1.3567; (R1) 1.3808; Extra….

Intraday bias in USD/CAD stays on the draw back at this level. A head and will high sample (1.3832; h: 1.3976; rs: 1.3807) needs to be fashioned already. Sustained buying and selling under 1.3494 will verify, and produce deeper fall to .3207 cluster help (61.8% retracement of 1.2726 to 1.3976 at 1.3204. Sturdy help needs to be seen there to carry rebound. However for now, danger will keep on the draw back so long as 1.3807 resistance holds, in case of restoration.

Within the greater image, up pattern from 1.2005 (2021 low) continues to be in progress. Based mostly on present impulsive momentum, it could possibly be resuming long run up pattern from 0.9056 (2007 low). Whether or not it’s or it isn’t, retest of 1.4689 (2016 excessive) needs to be seen subsequent. This can now stay the favored case so long as 1.3222 resistance turned help holds.

Financial Indicators Replace

| GMT | Ccy | Occasions | Precise | Forecast | Earlier | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | Commerce Steadiness (USD) Oct | 85.2B | 96.0B | 84.7B | |

| 02:00 | CNY | Commerce Steadiness (CNY) Oct | 85.2B | 702B | 574B | |

| 06:00 | JPY | Machine Instrument Orders Y/Y Oct | 4.30% | |||

| 07:00 | EUR | Germany Industrial Manufacturing M/M Sep | -0.20% | -0.80% | ||

| 08:00 | CHF | Overseas Forex Reserves (CHF) Oct | 807B | |||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -35 | -38.3 |