var lang='en';var hname="www.ifcmarkets.com";var bid = 'Bid';var ask =...

LumiNola

Introduction

Sleepy, boring, shares that the market appears to have forgotten are by far my favourite shares to find and to purchase. This has solely grow to be extra true in recent times with hyper-powered social media, meme shares, movie star CEOs, and cash managers who appear to assume staying within the information headlines is a job requirement. I normally find yourself avoiding these kind of shares just like the plague. And in my February eleventh, 2021 article “There Are Bubbles All over the place, However Money Is Not The Place To Be, Right here Are 10 Shares To Purchase Now” I went out of my strategy to warn traders about lots of the common market bubbles I noticed on the time.

There was numerous discuss bubbles within the market these days, and bubbles actually exist. Total valuations of the inventory market, by many accounts, are as costly as they’ve ever been. Crypto-currencies like Bitcoin (BTC-USD) have risen to uncharted territory. The IPO and SPAC market is on fireplace. Residential actual property set new information in 2020. Bond yields are extraordinarily low by most measures. I do not assume any of the above statements are notably controversial. So, I suppose we should not be stunned to see discussions of bubbles turning into extra frequent within the monetary media. For example, for the sake of argument that the entire folks claiming these markets are too costly to put money into proper now as a result of they are going to produce very low or unfavorable medium-to-long-term returns (say, over the course of 5-10 years) are proper. (My good method of claiming, they’re bubbles.) What ought to traders who want to get a possible inflation-beating long-term CAGR from their investments do?

Maybe we must always first invert our pondering, and checklist what NOT to do if we wish to obtain moderately good long-term returns. With a purpose to try this, we will consider issues we must always do if our purpose is to provide poor long-term returns. In the event you actually wish to guarantee you’ll produce poor returns over the following decade it is best to 1) exit and purchase as many current IPOs and SPACs as you may, 2) purchase a number of crypto-currency 3) put greater than 20% of your portfolio in long-duration bonds 4) purchase shares with low earnings yields 5) purchase shares with PEG ratios over 3.0, 6) purchase shares taking up large quantities of latest debt simply to maintain their companies alive, 7) purchase shares who had a brief 2-year elevate from COVID and at the moment are buying and selling at excessive costs, 8) purchase a brand new home that you do not want simply because your inventory portfolio has carried out nicely, 9) purchase the shares of companies which have proven proof they’re being disrupted by new expertise, 10) personal index or mutual funds which can be closely weighted with lots of the above sorts of shares, and final, however not least 11) maintain lots of money since you assume the whole lot is in a bubble.

It is perhaps price analyzing a few of the market proxies for what I warned traders about on the time.

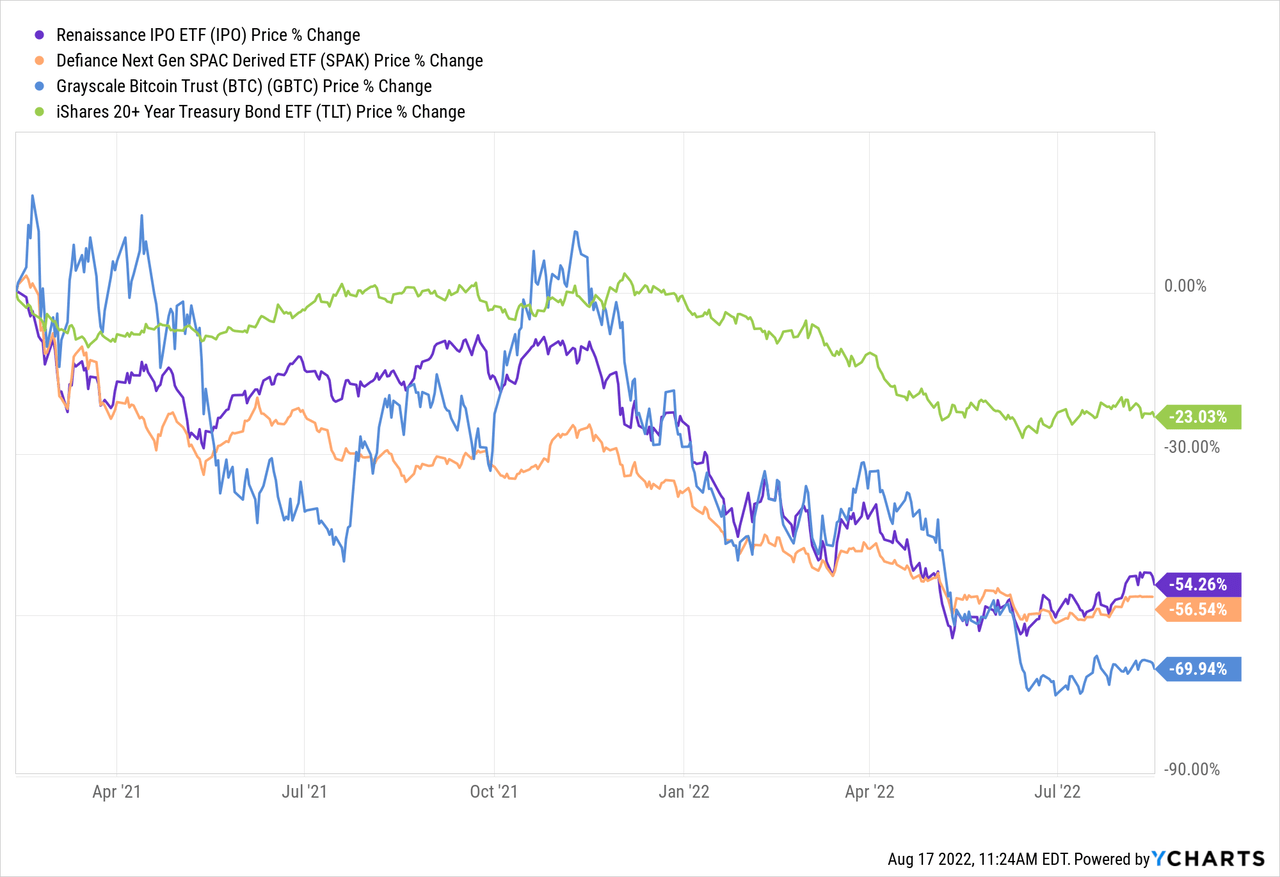

IPO information by YCharts

Right here is roughly how the primary 4 bubbles in IPOs, SPACs, Lengthy-Period Bonds, and Bitcoin have carried out for the reason that article.

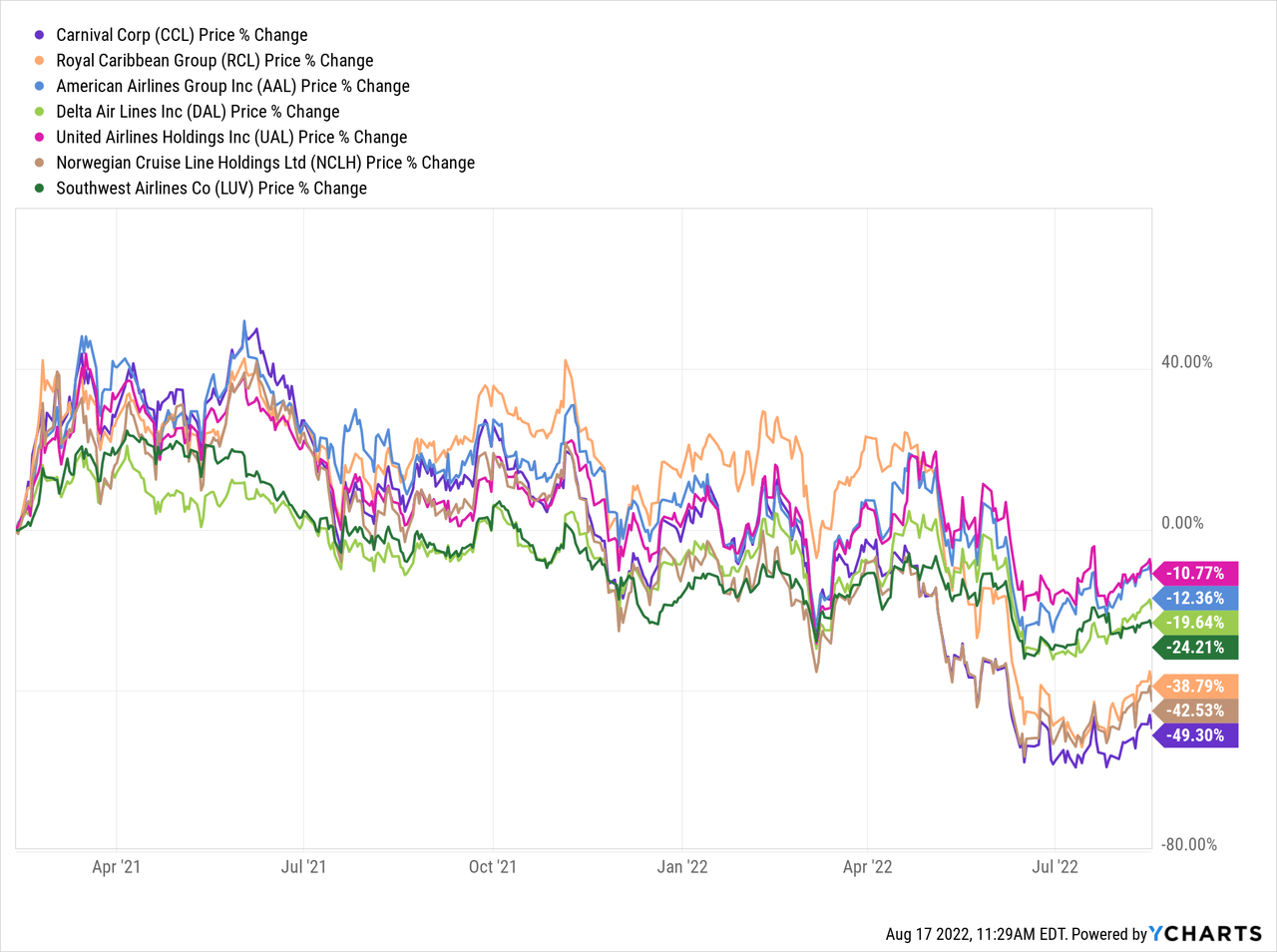

I haven’t got a easy ETF proxy for top valuation/excessive PEG ratio shares, however a lot of these have come down over the previous 18 months. When it comes to firms taking up debt to maintain their companies working, I largely had airways and cruise traces in thoughts.

CCL information by YCharts

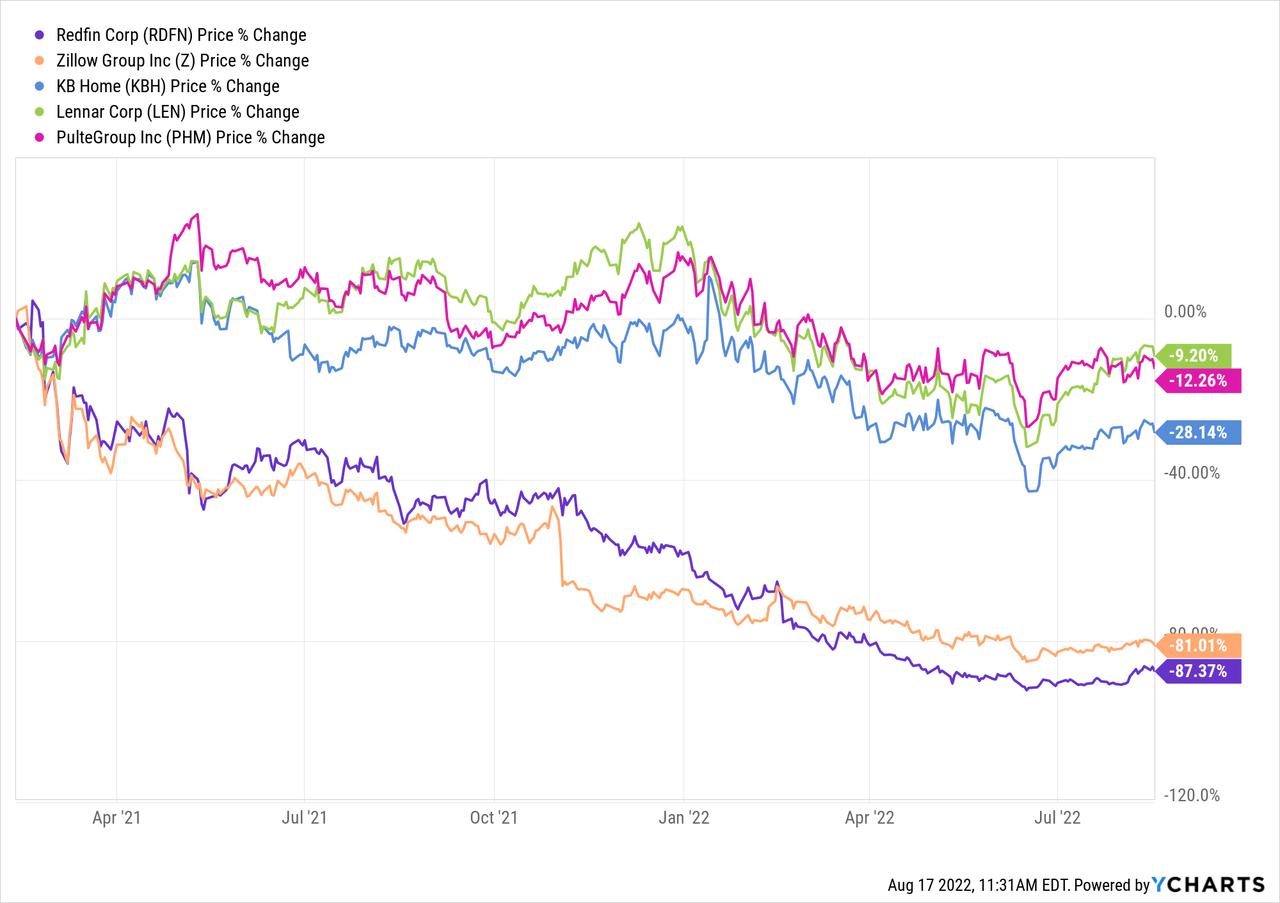

And let’s appears at some housing-related shares as nicely.

RDFN information by YCharts

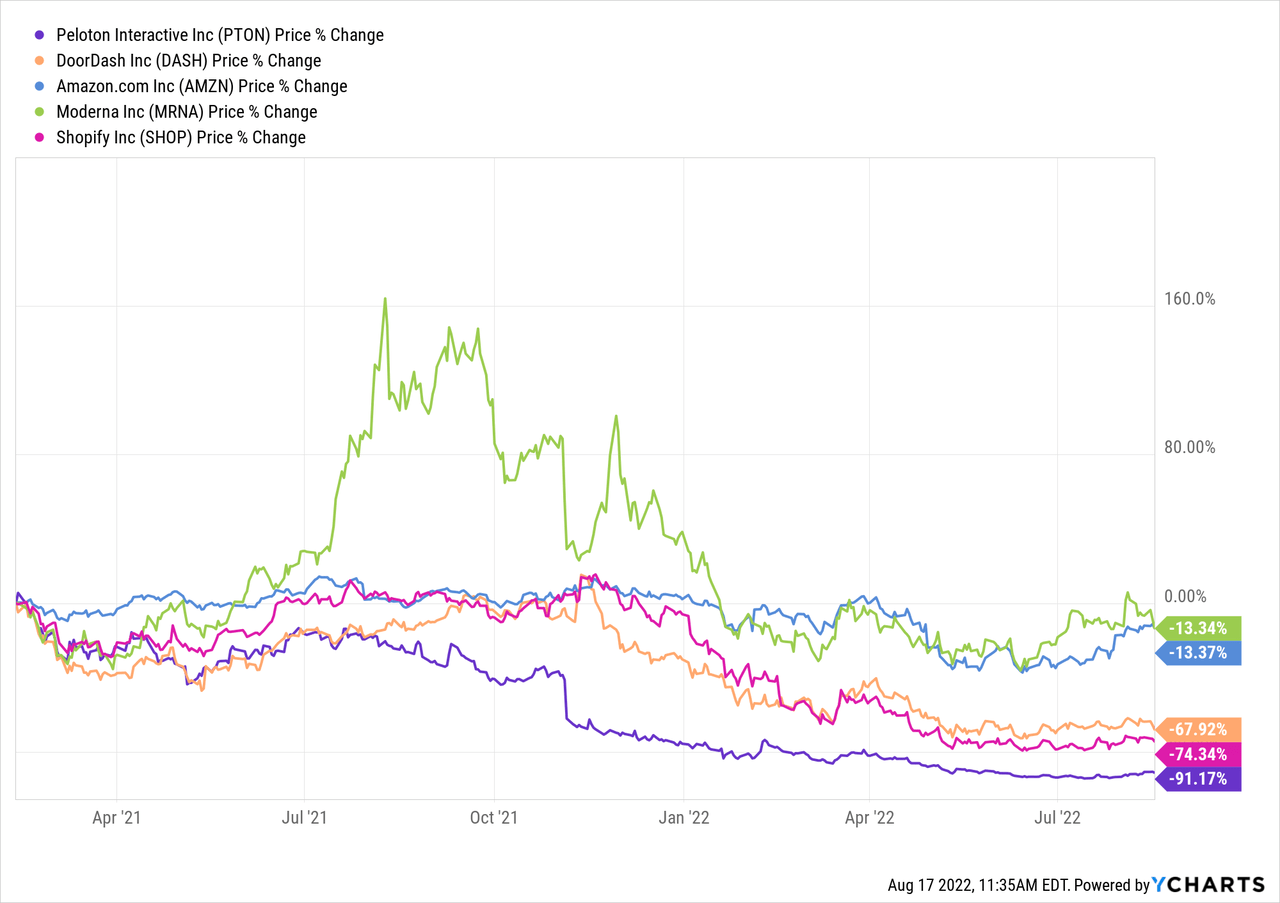

A pattern of short-term beneficiaries of COVID:

PTON information by YCharts

These are just some that got here to thoughts off the highest of my head.

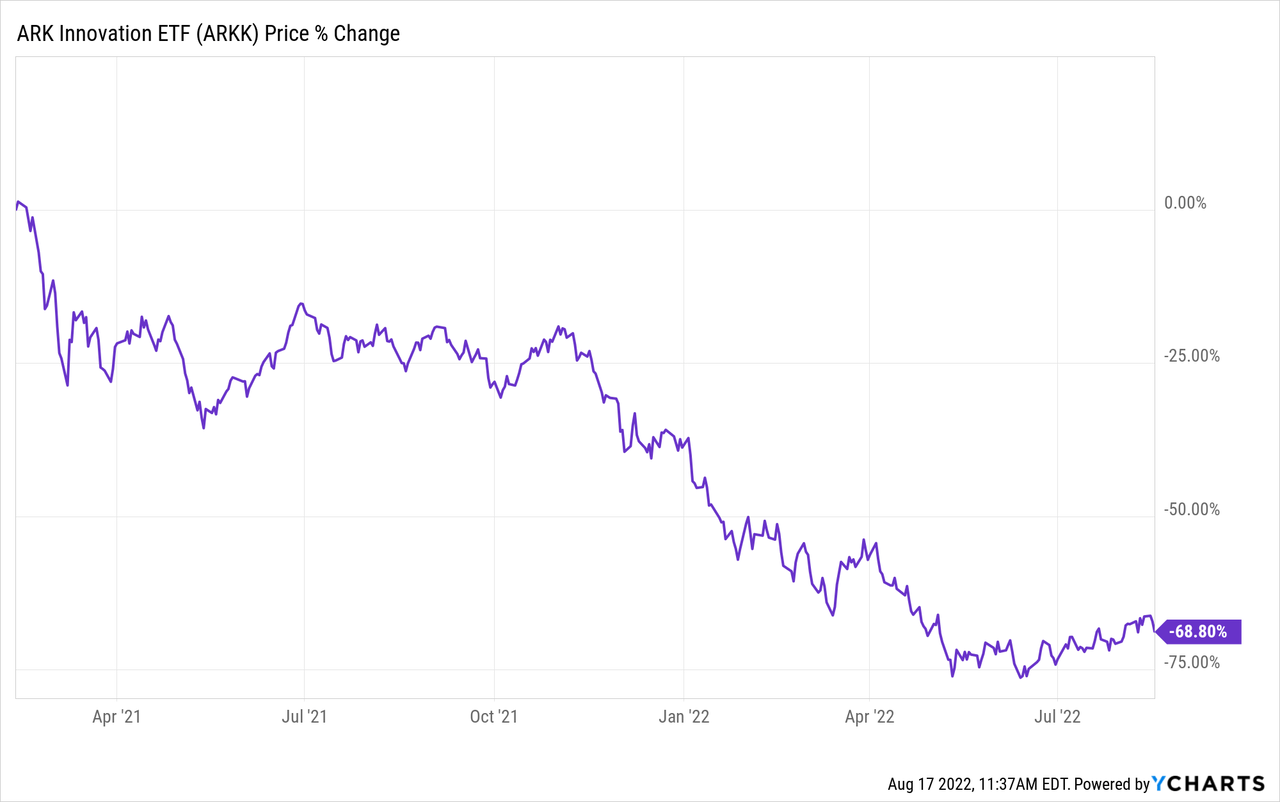

When it comes to ETFs or funds closely weighted to the above sorts of shares, I feel ARK Innovation (ARKK) is the poster youngster for this.

ARKK information by YCharts

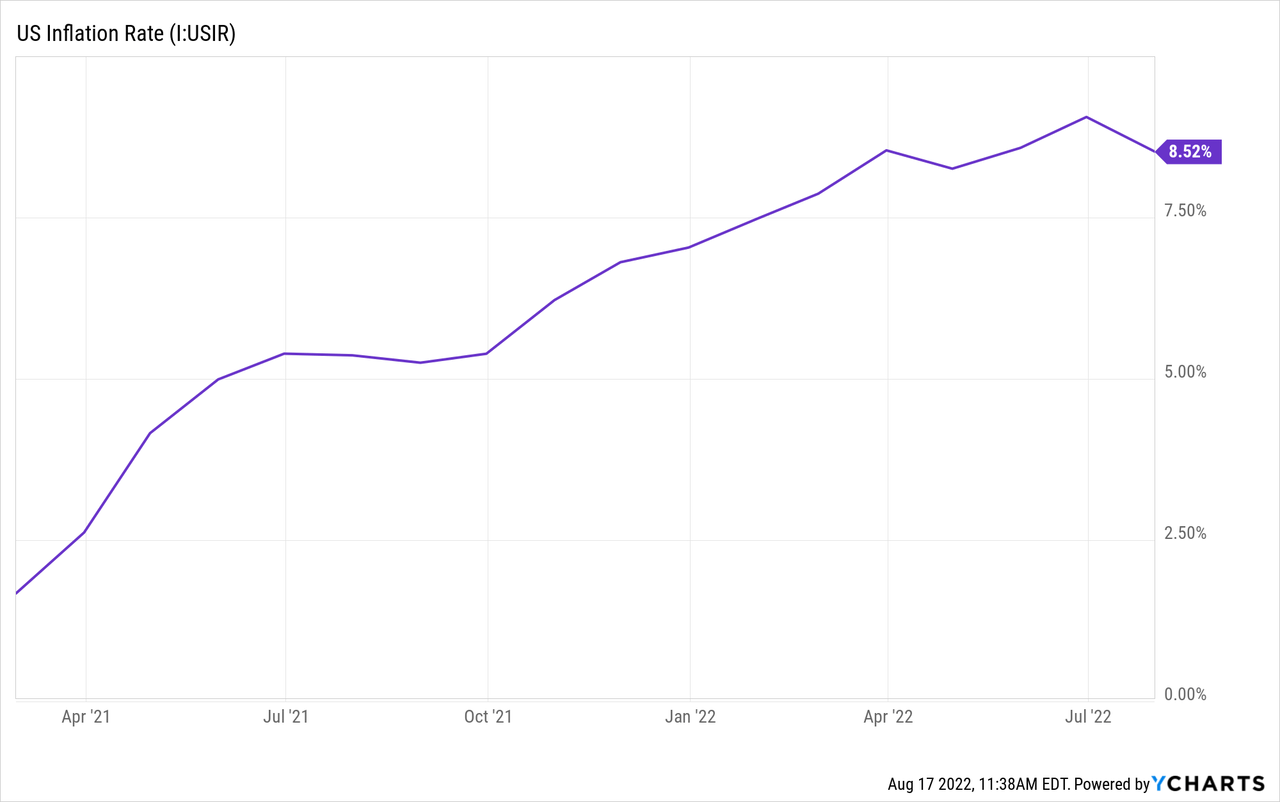

And final however not least, we will take a look at money by evaluating it to inflation, which was 4.7% in 2021 and is working about 8.5% this 12 months. Let’s simply say a lack of buying energy of -10% or so over the previous 18 months.

US Inflation Fee information by YCharts

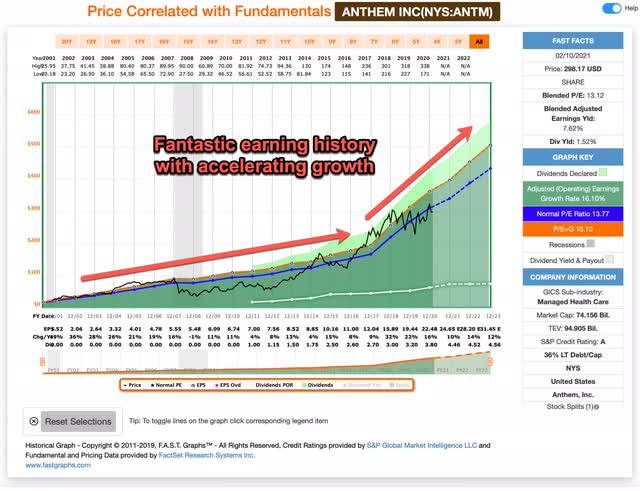

The explanation I carry all this up, is as a result of in that bubble article, I additionally shared 10 inventory concepts that I assumed, even at the moment of many bubbles out there, have been nonetheless affordable buys. A type of shares was Anthem, which has since modified its identify to Elevance Well being (NYSE:ELV). Here’s what I needed to say about it on the time.

Anthem is a well being insurer with a incredible return file at the moment buying and selling at depressed costs. I’ve beforehand written about it on In search of Alpha and I feel it has good medium and long-term potential. Like TROW, Anthem has a PEG ratio close to 1.

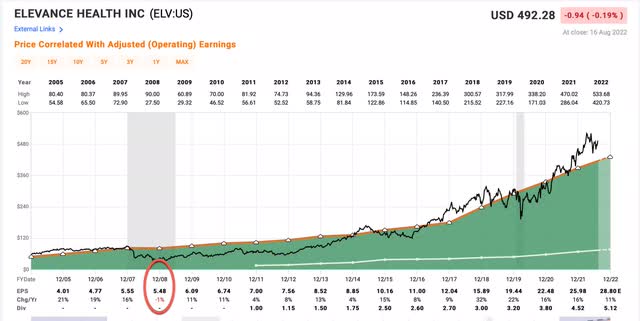

FAST Graph from February 2021 (FAST Graphs)

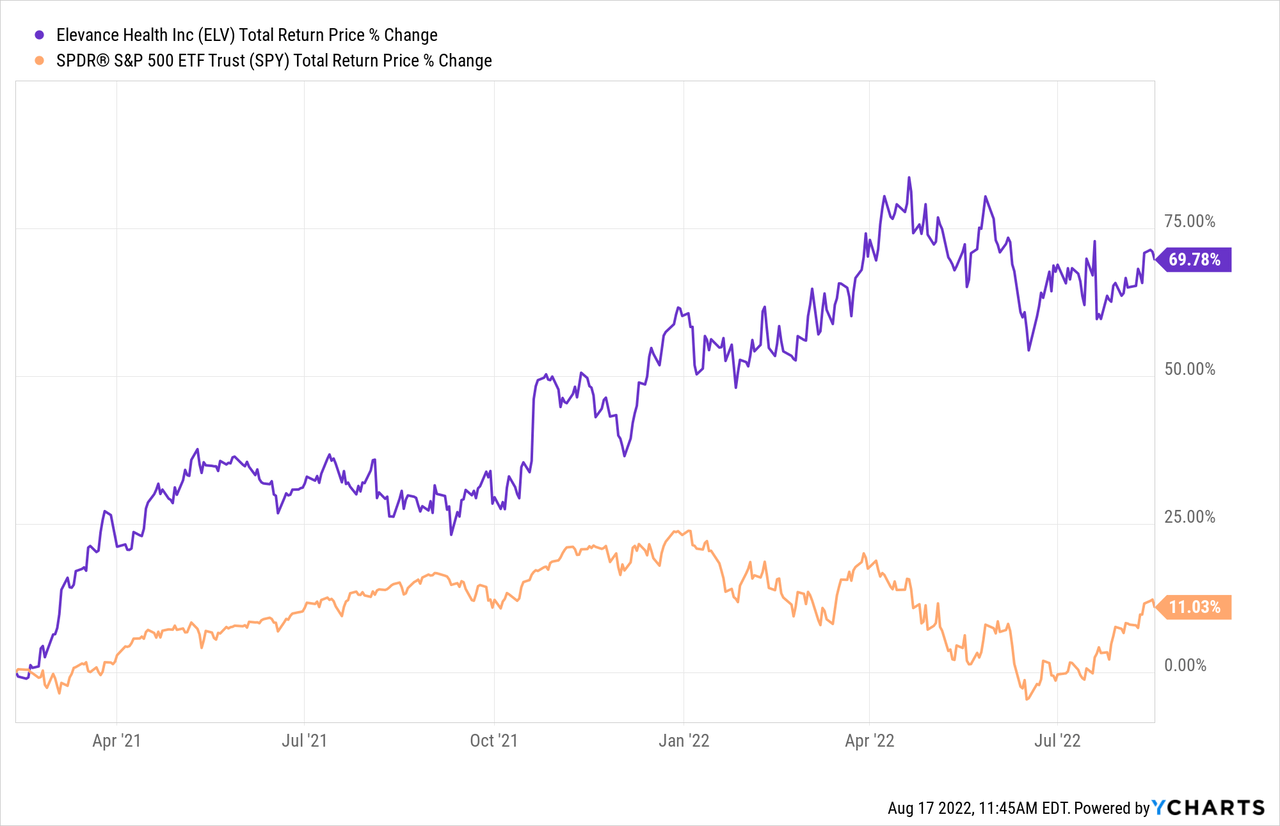

Because the publication of that article, right here is how Anthem, now Elevance Well being inventory, has carried out:

ELV Whole Return Value information by YCharts

Not solely has this sleepy, boring inventory outperformed all of the bubble shares and ETFs, it has additionally supplied 6x higher returns than the S&P 500 index.

One of many details that I wish to make right here is that the medium-term returns of common shares with nice tales however no fundamentals to again up these tales will normally produce poor returns. But when traders completely ignore what social and monetary media needs you to concentrate to, and as a substitute focus primarily on the numbers in comparison with historic traits, you may systematically discover shares similar to Elevance Well being again in February of 2021. (We really purchased this one on 12/21/20 in my market service, The Cyclical Traders Membership, and we nonetheless personal it.)

On this article, I will share the very same valuation course of for Elevance that I used to initially determine and purchase the inventory. It’s by monitoring a number of hundred prime quality shares utilizing this technique that I’m able to discover good investments, even inside the S&P 500, that the market merely is not listening to.

My Valuation Technique For Elevance Well being

The valuation technique I take advantage of for Elevance Well being first checks to see how cyclical earnings have been traditionally. As soon as it’s decided that earnings aren’t too cyclical, then I take advantage of a mixture of earnings, earnings progress, and P/E imply reversion to estimate future returns based mostly on earlier earnings progress and sentiment patterns. I take these expectations and apply them 10 years into the long run, after which convert the outcomes into an anticipated CAGR proportion. If the anticipated return is actually good, I’ll purchase the inventory, and if it is actually low, I’ll usually promote the inventory. On this article, I’ll take readers by every step of this course of.

Importantly, as soon as it’s established {that a} enterprise has an extended historical past of comparatively secure and predictable earnings progress, it would not actually matter to me what the enterprise does. If it constantly makes extra money over the course of every financial cycle, that is what I care about — numbers over tales.

FAST Graphs

Elevance’s historic earnings are represented by the darkish inexperienced shaded space within the FAST Graph above. Over the previous 20 years, Elevance solely had a single 12 months, in the course of the Nice Recession in 2008, when EPS progress declined, and it was solely by -1%. This basically makes Elevance a secular progress enterprise. Moreover we will see that earnings progress has accelerated since 2018 and has been constantly rising double digits.

As a result of earnings have nearly no cyclicality to them, it makes Elevance a very simple inventory to investigate through earnings and earnings progress, which is what the “Full-Cycle Earnings” evaluation I am about to share does. If earnings had been extra cyclical, then I’d have used a special kind of research.

Market Sentiment Return Expectations

With a purpose to estimate what kind of returns we would count on over the following 10 years, let’s start by analyzing what return we may count on 10 years from now if the P/E a number of have been to revert to its imply from the earlier financial cycle. For this, I am utilizing a interval that runs from 2015-2022.

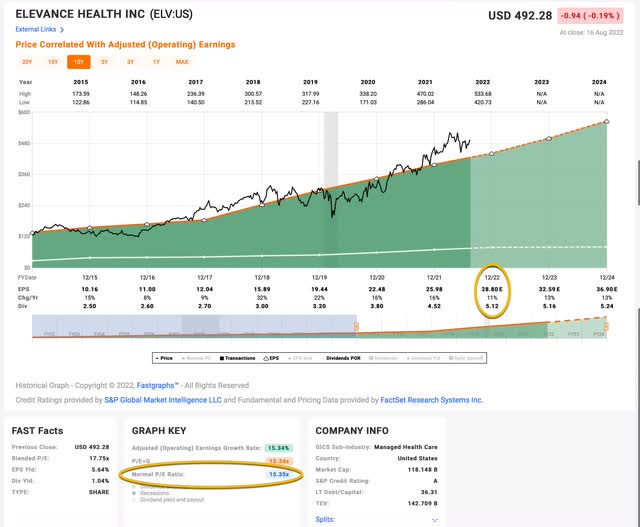

FAST Graphs

Elevance’s common P/E from 2015 to the current has been about 15.35 (the blue quantity circled in gold close to the underside of the FAST Graph). Utilizing 2022’s ahead earnings estimates of $28.80 (additionally circled in gold), ELV has a present P/E of 17.10. If that 17.10 P/E have been to revert to the typical P/E of 15.35 over the course of the following 10 years and the whole lot else was held the identical, ELV’s worth would fall and it could produce a 10-12 months CAGR of -1.07%. That is the annual return we will count on from sentiment imply reversion if it takes ten years to revert. If it takes much less time to revert, the return can be decrease.

Enterprise Earnings Expectations

We beforehand examined what would occur if market sentiment reverted to the imply. That is fully decided by the temper of the market and is very often disconnected, or solely loosely linked, to the efficiency of the particular enterprise. On this part, we’ll look at the precise earnings of the enterprise. The purpose right here is straightforward: We wish to know the way a lot cash we might earn (expressed within the type of a CAGR %) over the course of 10 years if we purchased the enterprise at as we speak’s costs and saved the entire earnings for ourselves.

There are two predominant parts of this: the primary is the earnings yield and the second is the speed at which the earnings could be anticipated to develop. Let’s begin with the earnings yield (which is an inverted P/E ratio, so, the Earnings/Value ratio). The present earnings yield is about +5.86%. The best way I like to consider that is, if I purchased the corporate’s complete enterprise proper now for $100, I’d earn $5.86 per 12 months on my funding if earnings remained the identical for the following 10 years.

The subsequent step is to estimate the corporate’s earnings progress throughout this time interval. I try this by determining at what fee earnings grew over the past cycle and making use of that fee to the following 10 years. This includes calculating the historic EPS progress fee, taking into consideration every year’s EPS progress or decline, after which backing out any share buybacks that occurred over that point interval (as a result of lowering shares will improve the EPS as a consequence of fewer shares).

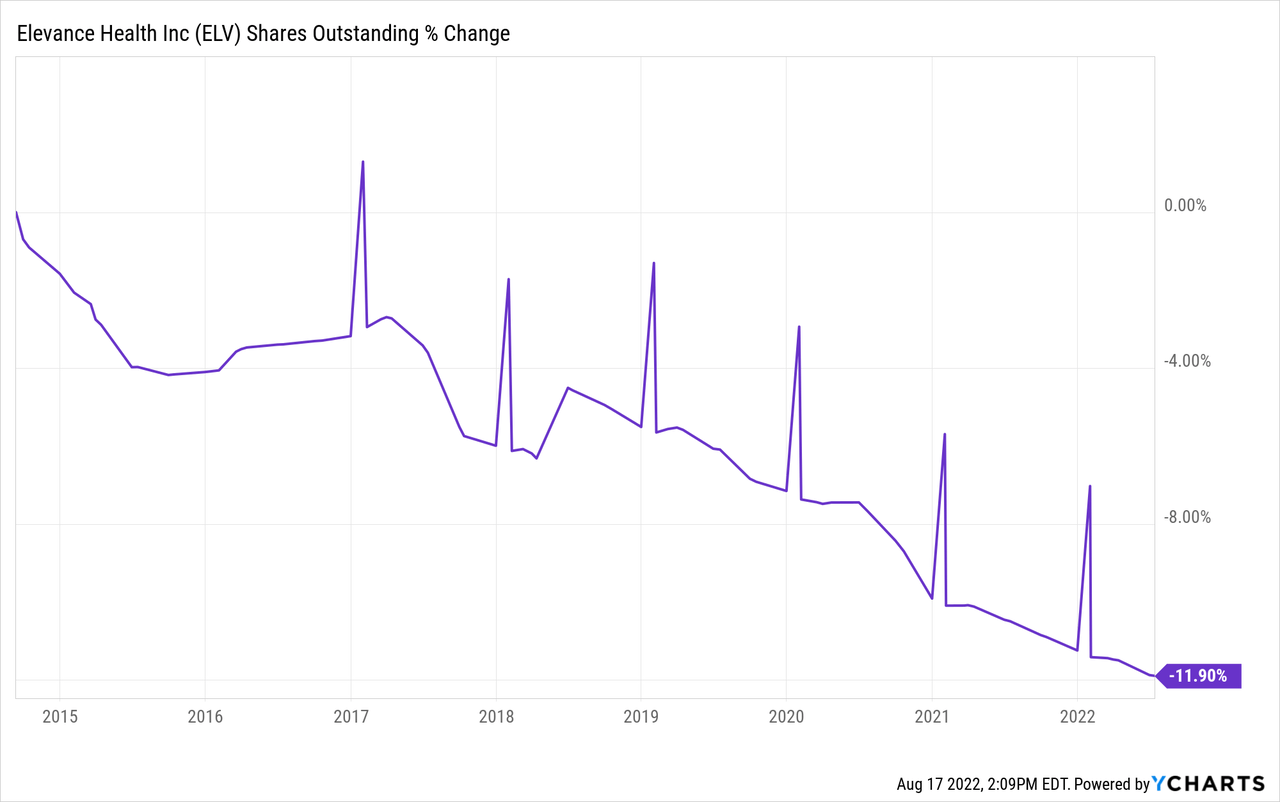

ELV Shares Excellent information by YCharts

Elevance has purchased again about 12% of the corporate since this level in 2015. I am going to make changes for this when estimating the earnings progress fee. After taking the buybacks into consideration, I’ve an earnings progress estimate for Elevance of about +14.09%.

Subsequent, I am going to apply that progress fee to present earnings, wanting ahead 10 years with a view to get a closing 10-year CAGR estimate. The best way I take into consideration that is, if I purchased ELV’s complete enterprise for $100, it could pay me again $5.86 plus +14.09% progress the primary 12 months, and that quantity would develop at +14.09% per 12 months for 10 years after that. I wish to know the way a lot cash I’d have in complete on the finish of 10 years on my $100 funding, which I calculate to be about $229.82 (together with the unique $100). After I plug that progress right into a CAGR calculator, that interprets to a +8.68% 10-year CAGR estimate for the anticipated enterprise earnings returns.

10-12 months, Full-Cycle CAGR Estimate

Potential future returns can come from two predominant locations: market sentiment returns or enterprise earnings returns. If we assume that market sentiment reverts to the imply from the final cycle over the following 10 years for ELV, it can produce a -1.07% CAGR. If the earnings yield and progress are just like the final cycle, the corporate ought to produce someplace round a +8.68% 10-year CAGR. If we put the 2 collectively, we get an anticipated 10-year, full-cycle CAGR of +7.61% at as we speak’s worth.

My Purchase/Promote/Maintain vary for this class of shares is: above a 12% CAGR is a Purchase, under a 4% anticipated CAGR is a Promote, and in between 4% and 12% is a Maintain. A +7.61% CAGR expectation makes Elevance Well being inventory a “Maintain” at as we speak’s worth, and nearly proper in the midst of what I’d think about the truthful worth vary.

We will see the significance of shopping for a inventory like this at a really engaging valuation. It permits for a scenario like this, the place the inventory worth can rise over +60% in lower than two years, and nonetheless not be overvalued. In truth, it is not unthinkable that this inventory may see double-digit progress for a few years to return and all an investor must do is hold on to it.

Conclusion

Boring shares that just about no person is listening to can usually make nice investments if they are often bought on the proper worth. Not solely is it unlikely the inventory worth will fall tremendous deeply, however in addition they have the potential to offer market-beating returns, even whereas shares that have been as soon as media darlings get crushed. One of the best ways to search out these boring shares (apart from by following writers like me) is to at first, concentrate on the numbers and certain returns reasonably than the “tales” we, as people, love a lot. Elevance was extraordinarily simple to determine as a very good worth in late 2020 and early 2021. Merely wanting on the PEG ratio and former earnings progress stability ought to have attracted a number of traders. And, ultimately it did. However solely after the fads and story-stocks of the day largely fell by the way-side.

It is attainable that if we’ve a recession subsequent 12 months that Elevance may fall to buyable ranges once more. At the moment, my purchase worth for the inventory for brand spanking new cash is about $377 per share if we aren’t in recession, but when we’ve a mean recession, the value may fall as little as $270, and which level it could be a steal for these traders who’re paying consideration.