wildpixel/iStock by way of Getty Pictures

The main indexes skilled their worst first 9 months of the yr since 2002, with declines within the Dow Industrials of -18.6%, S&P 500 of twenty-two.5% and NASDAQ Composite of 30.5%. These sizable declines are a results of rising curiosity charges pushed by the Federal Reserve’s restrictive financial coverage designed to reverse the best inflation the economic system has registered in 40 years. Fed Chair Jerome Powell communicated unequivocally that the Fed would hold tightening rates of interest with out regard to the market or the economic system in order to not capitulate to market or political pressures because the Fed mistakenly did through the Seventies:

“…my fundamental message has not modified in any respect since Jackson Gap. The FOMC is strongly resolved to deliver inflation all the way down to 2%, and we are going to hold at it till the job is completed. So the best way we’re eager about that is the overarching focus of the committee is getting inflation again all the way down to 2%.”

Since 2009, Federal Reserve insurance policies created artificially and traditionally low rates of interest which led to overvaluations in shares, bonds, and actual property. Due to the file 40 yr excessive inflation, which has developed within the final two years, the Federal Reserve is reversing its extraordinary monetary lodging inflicting shares, bonds, and actual property to expertise worth declines.

The Federal Reserve is making an attempt to gradual the economic system via tightening actions which can cut back demand and decrease inflation. This can be a very robust job as a result of inflation itself is not only the results of extreme lodging. For instance, there are inflationary provide chain points which grew out of the COVID-19 pandemic and power shortages as a consequence of ESG coverage errors in Northern Europe and North America. Sadly, restrictive rate of interest insurance policies don’t remedy semiconductor shortages, produce ample power nor produce ample meals provides. So the Federal Reserve appears to be like to gradual the economic system sufficient that demand ebbs and worth pressures fade.

Markets are adjusting to rising rates of interest and it doesn’t really feel good. Whereas markets are beneath stress, these circumstances present alternatives to purchase securities which can carry out nicely sooner or later. This letter explores how a lot worse inventory and bond markets can get, and what investments make sense.

Inflation

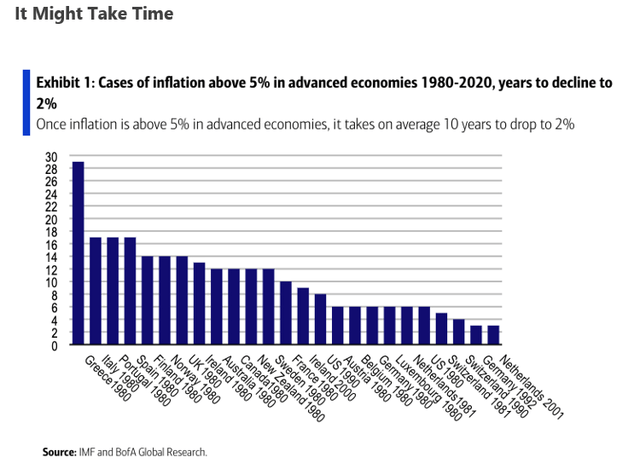

Inflation is a horrible state of affairs that received’t be solved rapidly. Take into account the chart under which analyzes nations the place inflation exceeded 5% and the way lengthy it took for inflation to say no again to 2% — the Federal Reserve’s acknowledged inflation goal charge. “It takes on common 10 years to drop to 2%.”

period of inflation reversion (The Transcript Substack)

Markets in Perspective

Rates of interest instantly correlate with asset costs. Consequently, the query buyers need to know is how way more restrictive financial exercise will probably be wanted to reverse the present development of rising inflation? We don’t know nor does anyone else. What we do know is that world inventory markets have misplaced $24 trillion in worth this yr, house costs are peaking and bond holders are seeing their worst efficiency in 40 years. [Wait! Bonds have been where investors have parked their safe money for decades and now they are losing on their safe money!?] These unhappy info will cool financial exercise.

By reviewing the historical past of rate of interest and inventory market cycles we are going to present market perspective to judge how a lot worse markets may get. In brief, charges can transfer larger nonetheless, however we could also be near an inflection level in rising charges globally.

Fairness Markets

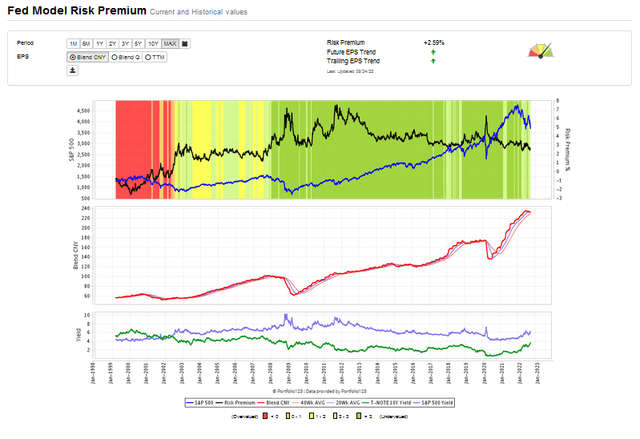

To estimate how a lot additional the inventory market might decline, we use the “Fed Mannequin” or Threat Premium Mannequin as a result of it hyperlinks the valuation of shares with bond yields. This mannequin under is very highly effective when the earnings development of the S&P 500 is highlighted. Earnings finally energy inventory costs. As we speak, these earnings estimates are turning down. The important thing query is will the Federal Reserve tighten a lot that the economic system begins contracting and corporations should lay off staff. If employment begins to say no sharply, an financial downward spiral might begin which might result in a 50% decline in earnings. The Fed hopes to gradual the economic system sufficient to reverse inflation however not create a recession, particularly a recession that’s world, deep, and or prolonged. [Think of the 1970s.]

Take a look at the earnings declines within the charts under that accompanied the three main declines since 1999. In 2000, on the top of the Tech Bubble, earnings peaked and led to declines of 83% within the NASDAQ 100 and 50% within the S&P 500. In 2007 earnings peaked once more, because the Nice Monetary Disaster commenced, and the economic system contracted and led to say no of 53% within the NASDAQ 100 and 54% within the S&P 500. In 2020, the COVID-19 pandemic triggered an financial collapse and a speedy decline in earnings with the shutdown, and the S&P 500 index declining 36% and NASDAQ 100, 31%.

As we speak’s setting resembles the Tech Bubble the place earnings usually are not collapsing, however the economic system is in a protracted decline, the increase in know-how shares has ended, however power, worth shares, and inflation beneficiaries are main the inventory market.

Fed Mannequin (Portfolio 123.com)

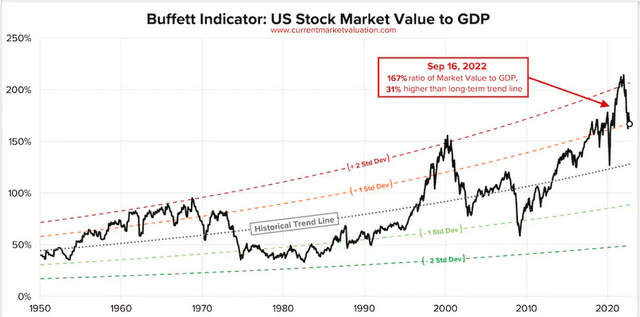

One other measure of draw back is “Buffett’s so known as Favourite Indicator” which compares the entire market worth of equities to the GDP. The chart under means that there could possibly be 31% additional draw back which we imagine is cheap however doesn’t assume problematic and chronic inflation nor consequential geopolitical developments. Our view is that we are going to expertise a yr and a half of enormous sideways to downward swings which can present alternatives for portfolio repositioning whereas the tempo of inflationary reversion is to be decided.

Buffett “favourite indicator” (www.currentvaluations.com)

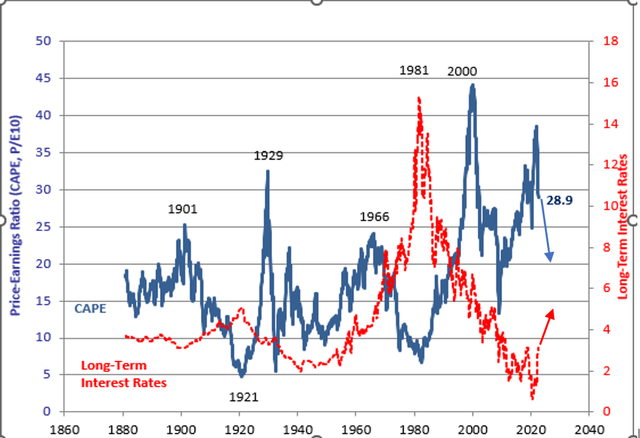

Buyers are prone to recency bias, that means that the majority buyers fail to have a look at markets inside a useful long run market perspective. The chart under of Robert Shiller’s long run CAPE ratio and bond chart under, present that PE ratios can afford to contract additional, and rates of interest might rise a very good bit additional when seen within the context of a 140 yr perspective.

CAPE ratio and bonds (CAPE chart by Shiller w bonds over 140 yrs)

Curiosity Charges

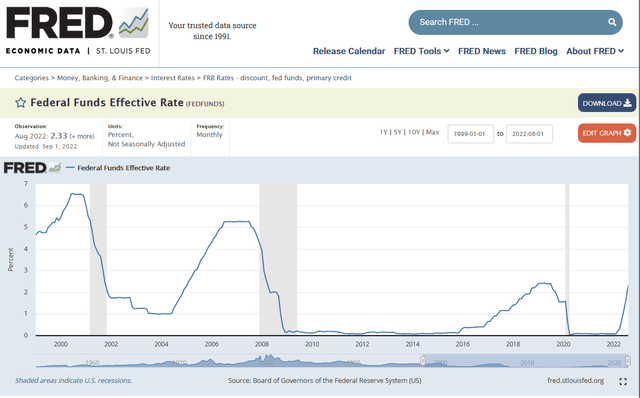

The Federal Reserve’s principal instrument is the Fed Fund charge. The chart under reveals the Fed Fund charge rising from close to zero to three.08%. This present charge rise is way sharper than the three earlier tightening cycles. The Fed expects the speed to rise to 4% by yr finish, but when its present actions don’t end in moderating inflationary information, the Fed Fund Price might rise into the 5 – 6% vary.

Fed Fund charge historical past (Saint Louis Federal Reserve Database)

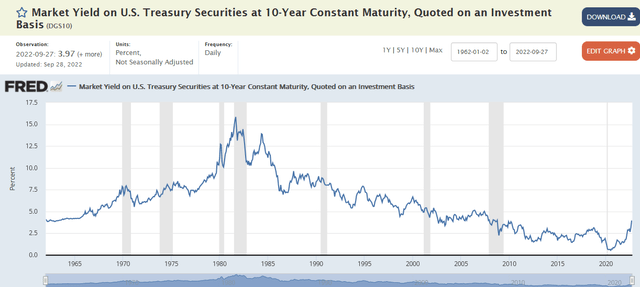

The chart under reveals longer maturity bond yields just like the 10-year US Treasury, reflecting what rates of interest are for mortgages and companies. The upper the yield on the 10-year US Treasury, the extra counter-cyclical or restrictive rates of interest are for a lot of the economic system. The chart under reveals 10-year US Treasury charges have soared from 0.5% to 4% within the final two years. Extra importantly, in the present day’s close to 4% yield continues to be nicely under regular cyclical reversions which may lead 5% or 6% yields.

10year treasury yield chart (Saint Louis Federal Reserve Database)

Supply: Saint Louis Federal Reserve Knowledge Base.

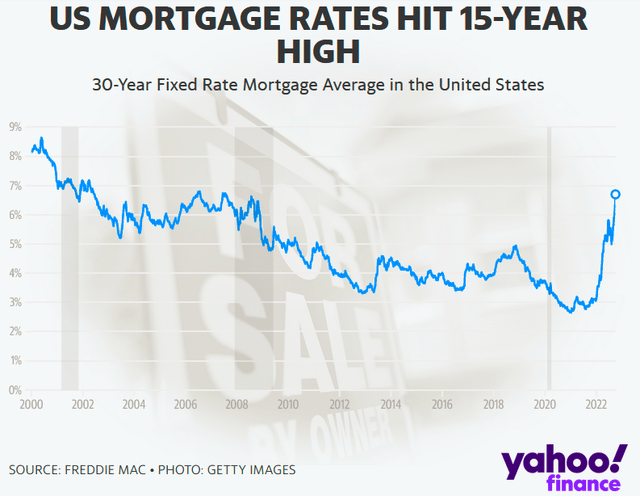

Whereas most buyers could not take into consideration what US companies pay to challenge debt, most households do know the way necessary proudly owning a house and having a low mortgage charge is. 30-year fastened charge mortgages have greater than doubled within the final yr. This rate of interest rise has dramatically modified the affordability of houses. Successfully, your typical mortgage purchaser of houses should purchase solely half the house he might a yr in the past. The collapse of this ubiquitous type of finance implies that actual property costs have stopped appreciating and now are starting to say no.

30 yr mortgage yield chart (Yahoo Freddie Mac)

The place to Make investments?

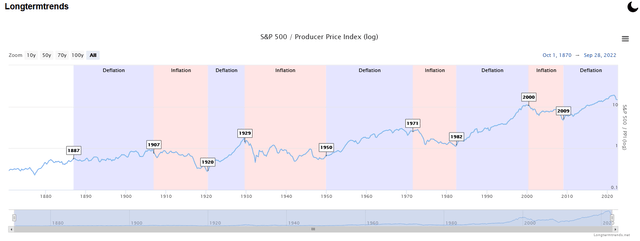

We now have entered an inflationary interval the place the S&P 500 underperforms relative to inflation. The chart under reveals distinct durations of inflation and deflation. The final two inflationary cycles had been 1971-1982 and 1999 – 2008. Each durations had been related to rising oil costs and decrease returns from the S&P 500. Consequently, lengthy period property resembling progress shares, know-how shares or lengthy period bonds will underperform and worth shares, power shares and inflation beneficiaries will outperform.

inflation and deflation historic chart (Longtermtrends.com)

Our major takeaway is that this inflationary interval will probably be protracted. The final two inflation cycles had been on common 10 years. Moreover, the prior illustration reveals it takes 10 years on common for inflation to revert to 2% after exceeding 5%. Consequently, we imagine that previous efficiency information of outperformance in lengthy period property together with know-how shares, progress shares and long term bonds will lose their attraction and be more and more de-emphasized in portfolio allocations. That is very true with the 60% inventory 40% bond allocation that has been the important thing stone technique to funding allocations of the final 40 years.

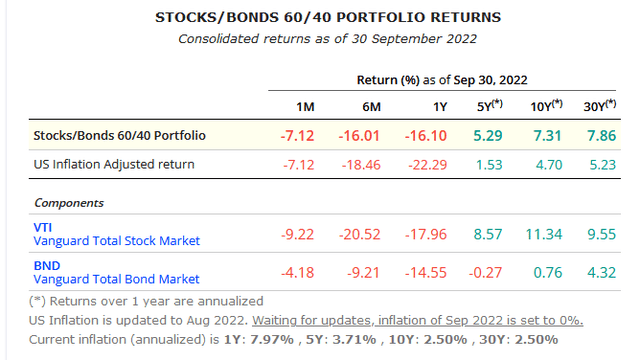

The chart under of the efficiency of the 60% fairness 40% bond allocation portfolio reveals how poorly this technique is working now that bonds are declining, and shares are declining as nicely. What’s worse, is while you take a look at the true return for the balanced portfolio and assume inflation will probably be within the 5% to three% vary for the following a number of years, this traditional technique will probably be a really poor supplier of actual (after inflation) diversified portfolio return.

As a result of the 60% fairness 40% bond technique will supply a weak danger adjusted actual return and primarily based on our examine of earlier inflationary cycle winners, we count on that rising markets, treasured metals, MLPs, excessive yield bonds, and inflation beneficiaries can have superior funding efficiency going ahead. Moreover, we imagine that the brand new bull markets needs to be protracted, and the previous main methods won’t return to their former distinctive return histories.

60 40 allocation return historical past (Lazy Portfolio ETF)

“Markets will probably be Risky”

John Pierpont Morgan famously stated markets will probably be risky when he was requested for his market prognosis. Acknowledged in another way, we are going to proceed to expertise interval of sentiment swings and over purchased and over bought circumstances. We need to be patrons of panic and ache and sellers of euphoria and reduction.

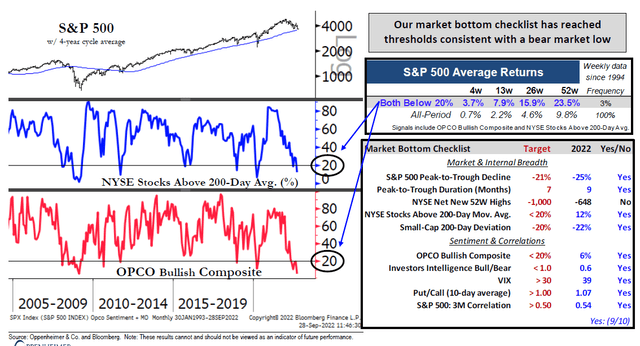

The markets are close to a buying and selling purchase stage. That is thoughtfully illustrated by Ari Wald of Oppenheimer under the place he reveals shares are each oversold, and sentiment is bearish. Very similar to the June backside, a rebound from current promoting ought to result in a tradable rally.

market with sentiment and oversold indicator (Oppenheimer Capital)

We proceed to advocate inflation beneficiaries resembling power, minerals which will probably be obligatory for the inexperienced transition infrastructure, MLPs for enticing earnings, excessive yielding investments, and treasured metals for a confirmed asset with sturdy buying energy preservation qualities.

Amongst particular names which we personal for our clients that we’re eager on are:

Vitality: Antero Sources Company (AR), Tellurian Inc. (TELL), Warrior Met Coal, Inc. (HCC), and Hallador Vitality Firm (HNRG).

Minerals: Rio Tinto Group (RIO), BHP Group Restricted (BHP), and Albemarle Company (ALB).

MLPs: Vitality Switch LP (ET), Enterprise Merchandise (EPD), MPLX Companions (MPLX), and Magellan Midstream (MMP).

Excessive Yielding investments: Antero Midstream Inc. (AM), Icahn Enterprises LP (IEP), and GAMCO Gold, Pure Sources & Revenue Belief (GGN).

Valuable Metals: Barrick Gold Company (GOLD), Sibanye Stillwater Restricted (SBSW), Van Eck Gold Miners ETF (GDX), SPDR Gold Shares (GLD) and iShares Silver Belief (SLV).

Conclusion

We’re within the midst of a cyclical and secular rotation away from 40 years of declining rates of interest. The final 13 years have witnessed traditionally low rates of interest which led to bubble valuation ranges in shares, bonds and actual property. The Federal Reserve is especially answerable for this financial coverage failure, however rampant Federal spending has additionally contributed to in the present day’s inflation nightmare.

Investing with an eye fixed towards new industries and sectors which have beneath carried out in deflationary durations and outperformed in inflationary durations will probably be important to future funding success. Our expertise and analysis have proven that investing in power, mineral, treasured metallic, MLPs and excessive yielding investments can present materials outperformance; moreover, these hanging onto outdated main shares, sectors, long run bonds and standard technique just like the 60% inventory 40% bond portfolios will discover themselves with poor portfolio efficiency as a consequence of recency bias.

Superior investing requires braveness, diligence, and independence. Buyers want to purchase panic and concern however promote into reduction and euphoria. Contrarian investing is rarely straightforward as a result of man is a herd animal. As we speak’s dismal market efficiency is a reminder that investing is a dynamic course of and there are not any easy methods. We advocate accumulating inflation beneficiaries on weak point and promoting previous deflationary leaders on energy.