The massive query on traders’ minds proper now’s, the place will inflation go? And the associated follow-up query, for everybody, is, how far will the Fed hike charges in response? The potential solutions cowl the complete vary of potentialities, from President Biden’s pleased speak about ‘zero p.c inflation,’ to the market bears predicting a full-blown financial melancholy.

Rely JPMorgan’s chief asset administration strategist David Kelly among the many bulls. He’s not satisfied by the doomsayers, and sees the latest drop in inflation as an indication that the worst is getting behind us. Whereas present situations are nonetheless laborious, Kelly believes that the inventory market can and can present extra energy going ahead. In his phrases, “I’d be absolutely invested in equities at this level as a result of I do suppose that equities can transfer larger right here.”

So let’s comply with JPM a little bit additional down this path. The banking big’s inventory analysts have picked out two shares that they consider are able to surge forward – by the order of 40% or extra. In truth, the JPM specialists aren’t the one ones singing these shares’ praises. In line with the TipRanks platform – they’re rated as Sturdy Buys by the Avenue’s analysts. Let’s take a better look.

BeiGene (BGNE)

The primary JPM decide is BeiGene, a clinical-stage biopharmaceutical firm, with, in its phrases, ‘a broad and deep pipeline’ that takes a shotgun strategy to the sector of oncology. The corporate is growing an incredible variety of drug candidates, greater than 50, each in-house and as collaborative efforts, to deal with remedy wants in some 80% of most cancers malignancies. A pipeline that dimension offers the corporate a aggressive benefit when in comparison with friends.

BeiGene is a very worldwide biotech agency, working in Asia, in Europe, and within the Americas, and boasting administrative places of work in Beijing, China, Cambridge, Massachusetts, and Basel, Switzerland. From these places of work, the corporate oversees its growth actions, and the commercialization actions for its line of authorized commercial-stage merchandise.

The main authorized merchandise are zanubrutinib, branded as Brukinsa, pamiparib, branded as Partruvix, and tislelizumab, branded beneath its personal title. As a gaggle, these medication are authorized in a number of worldwide jurisdictions for the remedy of varied hematological cancers and strong tumors. BeiGene has been actively commercializing them for a number of years now, and in 2Q22 the corporate realized $304.5 million in complete gross sales income. This quantity included $128.7 million from Brukinsa and $104.9 million in gross sales of tislelizumab in China. The corporate’s complete income, which incorporates collaboration charges, reached $341.6 million, in comparison with $150 million within the year-ago quarter.

Overlaying the inventory for JPMorgan, analyst Xiling Chen believes BGNE presents a compelling threat reward. Kumar charges the inventory an Obese (i.e. Purchase) together with a $296 worth goal that means a 50% one-year upside.

Backing his bullish stance, Chen writes: “We see BeiGene shares as undervalued given high quality of belongings/development and spotlight the inventory as considered one of our prime picks within the sector… BeiGene has grown into a totally built-in biopharma firm with best-in-class scientific growth capabilities, one of many largest and finest oncology industrial platforms in China, and unmatched partnership expertise with international biopharma corporations. We anticipate the corporate’s 16 industrial belongings and broad pipeline to drive very enticing, diversified long-term development. Whereas we stay reasonably under consensus on long-term gross sales, we see extra pipeline traction as upside to our estimates…”

General, 6 Wall Avenue analysts have chimed in on this biotech big, and left 5 Purchase suggestions towards 1 Maintain for a Sturdy Purchase consensus score. The shares are priced at $192.77 and their $253.76 common worth goal signifies an upside potential of ~29% within the coming months. (See BGNE inventory forecast on TipRanks)

Xenon Prescription drugs (XENE)

The second inventory we’re taking a look at is Xenon, one other biopharma agency on the scientific stage. Xenon is engaged on new therapeutic brokers within the discipline of neurology, searching for novel medication to deal with neurological situations with excessive unmet medical wants. The corporate has a specific give attention to remedies for epilepsy.

Xenon has two main drug candidates on this discipline, XEN496 and XEN1101, at Part 3 and Part 2 trials phases respectively. XEN496 is Kv7 potassium channel opener, and is being investigated for a uncommon pediatric type of epileptic seizure dysfunction. The corporate expects to finish the Part 3 EPIK research of XEN496 throughout 2023.

XEN1101, nevertheless, is the corporate’s flagship drug candidate. It’s at present present process a number of Part 2 trials, for focal onset seizure epilepsy (FOS), main generalized tonic-clonic seizures (PGTCS), and main melancholy. The Part 2b X-TOLE trial, towards FOS, is anticipated to be accomplished this 12 months, and the corporate has two equivalent Part 3 trials, X-TOLE2 and X-TOLE3, in preparation to run when the present trial is accomplished. The Part 3 trials will run in parallel and enroll as much as 360 sufferers.

Xenon can also be planning the X-ACKT Part 3 trial, to proceed its research of XEN1101’s efficacy towards PGTCS. This research will run concurrently with the X-TOLE trials.

Lastly, Xenon has the Part 2 X-NOVA research ongoing to guage XEN1101 towards main depressive dysfunction. Topline outcomes from this X-NOVA research, which has enrolled 150 sufferers, are anticipated in 2023.

JPM analyst Tessa Romero sees XEN1101 as the important thing issue on this inventory, and lays out a transparent case why: “Bolstered primarily by compelling section 2b X-TOLE information in addition to optimistic doctor suggestions, we view XEN1101 as having a excessive chance of success as an adjunctive remedy in its lead indication of focal onset seizures (FOS). On the similar time, we additionally see the potential for XEN1101 to work in each sufferers with focal and/or generalized seizures and forecast ~$1B in peak gross sales within the U.S. alone within the mixed epilepsy indications (~$700M of which is FOS) the place our estimates may show conservative.”

“We consider there is a chance in XENE shares at present ranges which under-reflect the potential of XEN1101 to develop to extra excessive unmet want indications past FOS the place there may be convincing rising rationale,” the analyst added.

Romero charges shares in XENE as Obese (i.e. Purchase), and her $55 worth goal implies a 46% upside by the tip of subsequent 12 months. (To observe Romero’s monitor report, click on right here)

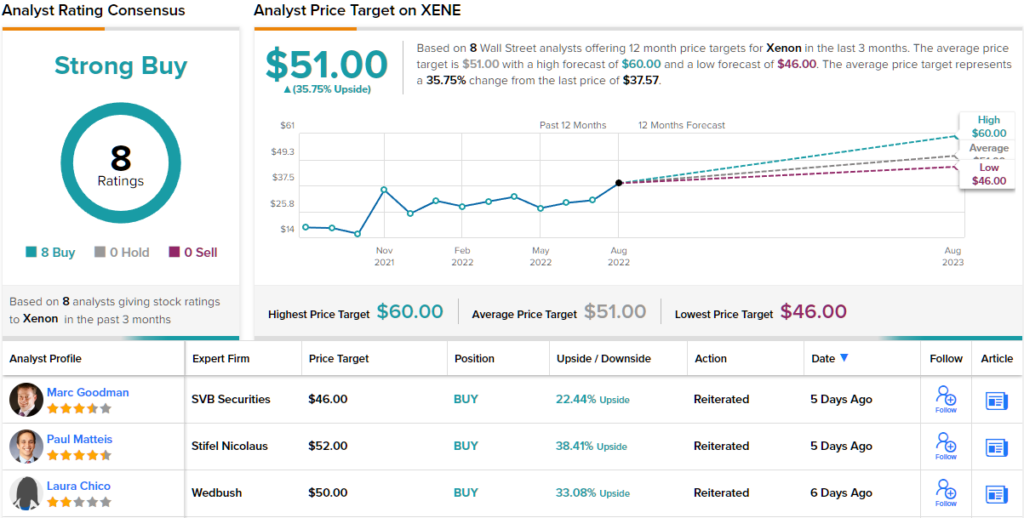

Wall Avenue is clearly upbeat on this biopharma, as all 8 of the latest analyst evaluations are optimistic – for a unanimous Sturdy Purchase consensus score. The inventory is promoting for $37.57 and its $51 common worth goal suggests ~36% one-year upside potential. (See Xenon inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely necessary to do your personal evaluation earlier than making any funding.