Jay Yuno/E+ through Getty Pictures

On this article, I current arguments for allocating capital to a specific slice of the tech sector that presents a very uncommon alternative for long-term compounding potential: Software program.

For my part, this era presents the most effective occasions within the final decade to spend money on public fairness software program. I make the case for this with trade dynamics, the interaction of macro and prices of capital, and valuation paradigms marked by historic knowledge.

The Latest Fall of Software program

Macroeconomic fears, inflation, and geopolitics have led to a broad risk-off atmosphere that got here into buyers’ periscope in late 2021, after which subsequently picked up pace with the onset of higher-than-expected inflation paired with the Russia-Ukraine battle. Meals and oil costs, greater charges to fight inflation, everyone knows the story.

As software program firms by and enormous have a mixture of growth-oriented forecasts, free money flows late into the long run, and valuations constructed on long-duration relatively than short-duration financials, these companies logically offered off.

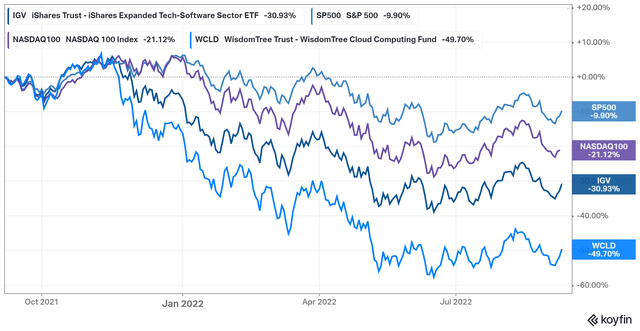

WisdomTree Cloud ETF vs benchmarks (Koyfin)

The chart above exhibits two outstanding software program ETFs:

- IGV – iShares Expanded Tech-Software program ETF

- WCLD – WisdomTree Cloud Computing ETF

IGV holds some GARP=oriented names, whereas WCLD is extra high-growth influenced in its composition. Naturally, each have underperformed the S&P and Nasdaq with WCLD scoring a relatively nasty 50% drawdown from late 2021. For these buyers following this area, you’d have observed 50-70% drawdowns in high-flying names that at the moment are being judged for his or her profitability relatively than their development.

The valuation story, after all, builds on the price of capital. As rates of interest have risen, so have 10-yr treasury yields to the tune of three.5% and relying on their development to maybe 4% or worse if wanted on this macro atmosphere. By monetary idea, this drastically influences discounted money circulate fashions bringing in “intrinsic valuations” decrease. A rule of thumb to comply with right here is that with each 1% level improve within the 10-yr yield, valuations within the high-growth class decline 20% on an intrinsic foundation. 3 proportion factors lead to a 49% drawdown.

Whether or not one agrees with trendy monetary idea and these strategies of valuation could also be considerably irrelevant in a sensible sense, as pension funds and institutional capital make the most of these theories and vote with their capital. Thus the tech sector rotation and the software program implosion.

However this is the humorous factor. Basically, loads of software program companies, notably within the cloud computing area, are going significantly sturdy.

What We Discovered Over The Final Two Quarters

We have now two-quarters of earnings knowledge and transcripts for 2021 throughout nearly all software program firms as I write this. Inside my area of protection, I’ve observed sure patterns. There have been losers, actually, which have seen decelerating development with not-great profitability to indicate for it (TWLO, ZM), however they’ve additionally been winners which are executing on macro-resilience with gentle or no efficient macro headwinds.

The next earnings transcript excerpts present a way of the trade from software program companies working in numerous domains.

- Microsoft – the massive daddy of software program

- HubSpot – a now giant cap, advertising and CRM platform

- Alteryx – mid-cap, knowledge analytics software program

- Monday – mid-cap, a platform for workflow administration and use circumstances

- Snowflake – large-cap, hyper-growth knowledge warehousing

1. Microsoft

However what’s taking place with — in Azure although, is in some sense, companies making an attempt to cope with the general macroeconomic state of affairs and doing — making an attempt to guarantee that they will do extra with much less. So for instance, transferring to the cloud is one of the best ways to form your spend with demand uncertainty, proper? As a result of — and in reality, if something, one of many issues that we’re seeing is an elevated shift in the direction of the cloud.

After which, after all, optimizing your invoice. We’re incenting even our personal area to make sure that the payments for our prospects come down. And that, the truth is, even exhibits up in among the volatility in our Azure numbers as a result of that is one of many massive advantages of the general public cloud. And that is why I believe popping out of this macroeconomic disaster, the general public cloud shall be even a much bigger winner as a result of it does act as that deflationary power.

– CEO Satya Nadella – Q2 Microsoft (MSFT) Earnings Transcript

2. HubSpot

Now whereas these traits can have impression within the brief time period, and it’s mirrored inside our steerage, we’re assured in HubSpot’s long-term development alternative for a few causes. First off, whereas these offers are taking longer, they’re coming right down to platform and multi-hub choices. SMBs are determining how you can spend successfully, and so they’re HubSpot because the platform to run their entrance workplace. So we see offers shut favorably however taking a little bit bit longer. And second, we’re not a discretionary level answer.

We are the spine for small and medium companies. All these companies nonetheless must market, they should promote, they should service their prospects. And HubSpot is a system of [indiscernible] and engagement for buyer knowledge. So we’re mission-critical and we’re sticky. So whereas we’re seeing the demand development soften a bit within the brief time period, we’re very assured in our technique and long-term development.

– CEO Yamini Rangan, Q2 HubSpot (HUBS) Earnings Transcript

3. Alteryx

Enterprise leaders are prioritizing analytics and embracing democratization of information to scale their analytics and upskill their workforces. And with the macro atmosphere serving as a forcing perform for companies to optimize and automate analytics, the market is coming to us with better urgency and demanding options that Alteryx is uniquely positioned to offer.

– CEO Mark Anderson, Alteryx Q2 Earnings Transcript

4. monday.com

Additionally in regard to your query about consolidation, I believe that — along with what Eliran stated with the macro economic system, — we see right here an amazing alternative for us as an organization as a result of loads of our prospects understand that they will do way more with monday as a platform. They may have a number of use circumstances, however now they see the potential of the spend on monday all through many extra departments and maybe consolidate a number of completely different instruments underneath monday. So undoubtedly, we’re beginning to see this as a development. In order that’s additionally very fascinating. It is one thing we additionally push in given the macro economic system.

– Co-CEO Eran Zinman, Q2 monday.com Earnings Transcript

5. Snowflake

Final quarter, we referred to as out prospects that have been negatively impacted by headwinds particular to their companies. The Q2 outcomes from these prospects have been combined. Some noticed the weak spot we anticipated whereas others outperformed. We’re monitoring our key enterprise metrics, which we consider are main indicators of the macro economic system impacting our enterprise. We’re not seeing these metrics soften throughout the client base…

Only a fast follow-up. I really assume that the dynamic that you just’re describing, I imply, we’ll see the precise reverse of that. We expect individuals — due to the nervousness that they could have concerning the macro, they will speed up to a cloud computing platform. And the reason being these are elastic fashions. These are consumption fashions, proper?

– CEO Frank Slootman, Snowflake Q2 Earnings Transcript

I have never included essentially the most macro-resilient sector, cybersecurity amongst these firms. These names have all sailed by with minimal interference. However there are a number of themes to notice from the excerpts above that pertain to the broader trade dynamics.

- Macro headwinds are current, however execs assume this solely supplies an elevated worth proposition for cloud computing. Microsoft as an example highlighted the slow-down in old-school options and remarked on the necessity for ongoing digital transformation by Azure.

- Even seemingly macro cyclical software program corresponding to marketing-related software program seems to be moderately positioned in an innovation context. Different non-mission crucial software program corresponding to Monday, successfully a person expertise app on steroids, has performed alright.

- Europe is comparatively worse hit on software program adoption in comparison with the US, seemingly from the battle and ensuing meals and vitality conditions. This issue is just remoted to sure pockets of software program.

- Platforms win, not particular person apps on this economic system. HubSpot and Monday, each highlighted their relative power for multi-faceted use circumstances throughout a streamlined platform. If enterprises can do loads of issues by one product for and save prices, it is good.

- Cloud transformation, is the truth is, a approach to save prices. And the ROI does not accumulate after a number of years – advantages are realized quickly

I see the atmosphere as glorious for pro-innovation software program, notably cloud firms. Use circumstances for these merchandise are sometimes exceptional, and the next-gen digital transformation firms are harbouring some lofty worth propositions. So as to add, I can’t overstate the variety of occasions the time period “mission-critical” appeared throughout earnings transcripts, with nice monetary outcomes to again them up. A Ctrl+F on the transcripts, and an excellent likelihood essentially the most macro resilient companies would be the ones that hark on about “mission crucial”.

Whereas the market contributors are crying out for earnings proper now, they need to additionally observe that development is prone to proceed, and it is price in search of out respectable money circulate era and even burn towards a well-funded stability sheet. I say this as a result of enterprise execution is okay, and the expansion pathways for continued market seize towards lengthy TAMs are nonetheless intact. As an example, Monday is burning money reasonably however has $800m on stability towards a $400m gross sales run charge, compounding at 70%+ YoY. Some burn towards this stability sheet is strategically clever in an effort to seize market quicker.

Valuations In opposition to Historical past

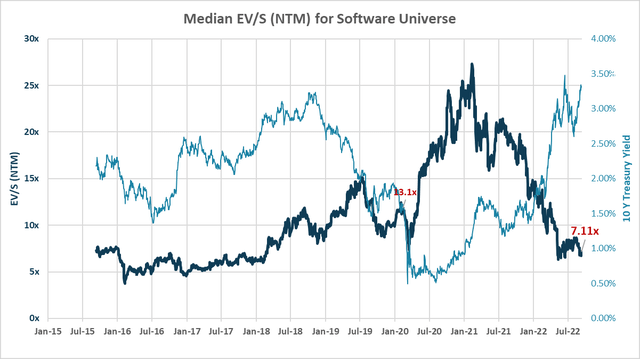

Alright, so what about valuations? These treasury yields are awfully excessive. Nicely, let’s put that into context.

I crunched the info on EV/S (Subsequent Twelve Months) from about 50 software program shares (each outdated and new) to search out the universe’s median valuations towards a 7-year time interval. The 10Y yield is mapped in mild blue. Notice that I’ve excluded outdated sluggish giants like IBM and CSCO that do not go well with my goal universe.

EV/S NTM Median multiples for a 50 inventory universe (Writer (knowledge from Koyfin))

This chart singularly captures loads of my reasoning for going lengthy software program now. Listed here are a number of knowledge inferences:

- The pre-pandemic peak got here in 2019 at about 15x at a 2% yield and declining; proper earlier than the pandemic hit, the chart peaked as soon as extra at 13.1x

- With crushed yields and the raging bull run, we noticed software program medians attain as excessive as 25x ahead metrics; mid-2021 noticed inflation and yields on the horizon and late 2021 noticed the onset of the macro we’re in proper now

- 2015-2017 was pretty steady for multiples at a comparatively low yield, the chart started transferring up as cloud transformation shares have been on quickly rising historic trajectories influencing the long-duration multiples taking averages up.

- We at the moment are at 7.1x NTM EV/S on the universe, beneath the pandemic backside, and again to 2017-2018 multiples.

The connection between the treasuries and valuations charts appears logical. On the flip of 2018, we crossed the 7x threshold as yields. 2017 was thought-about on my own and plenty of as a goldilocks interval for valuations with development, earnings, and stability put up the Trump 2016 election proved beneficial for the markets. As of right this moment, the multiples have shot again to late 2017 or early 2018 numbers.

The query one needs to be asking is what is suitable for right this moment’s situations. Ought to we get again to a 5x vary? If yields head to 4.5% or extra, that appears doable and loads is dependent upon inflation and stability. Nevertheless, I would additionally argue that the software program panorama has radically modified for the reason that mid-2010s. At this time’s universe is plagued by high-growth and hyper-growth shares that present no indicators of slowing down. Anchoring to a 2015 software program atmosphere is considerably negligent of the development in enterprise fashions and gross sales machines that drive right this moment’s companies. The EV/S ahead multiples listed above are likely to underestimate long-term excessive development, solely seeking to the subsequent twelve months.

So as to add, consider the next train: mark the chart above on New 12 months’s 2018, the place multiples have been round 7x, which is about the identical as the place they’re now. Here’s a checklist of software program firm returns since then that beat the markets from then to now:

- MongoDB (MDB): +818%

- Palo Alto Networks (PANW): +280%

- HubSpot (HUBS): +271%

- ServiceNow (NOW): +257%

- Microsoft (MSFT): +225%

- Twilio (TWLO): +187%

- Alteryx (AYX): +161%

All this in comparison with Nasdaq’s +89% and the S&P 500’s +52% over the identical interval. Now, this checklist actually exhibits a cherry-picked survivorship bias and I do not imply to color the entire trade with it as some future expectation of returns. Nevertheless, my level is that it’s certainly doable to choose some progressive movers and have immense returns regardless of these flat valuation paradigms over a 5-year interval. Funnily sufficient, even the now despised Twilio (TWLO) nonetheless outperformed the market. I do not see a purpose why there will not be different names in software program like these over the subsequent 5 years when contemplating right this moment’s trade dynamics and earnings name discussions throughout a bunch of mid/large-cap equities.

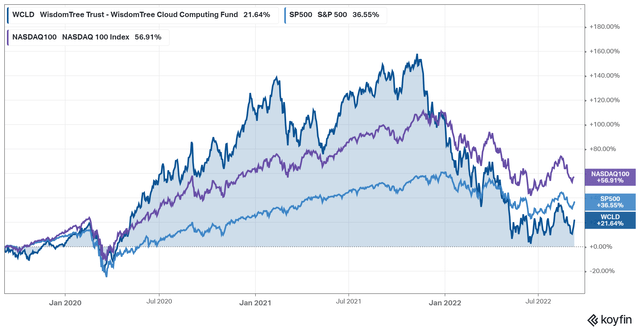

This development of relative outperformance on multiples will be additional defined by the next chart – which exhibits the whole returns of the WisdomTree Cloud Computing ETF towards the favored benchmarks.

WisdomTree Cloud ETF vs Benchmarks (Koyfin)

WCLD has underperformed the usual market benchmarks since its inception on sixth September 2019. Nevertheless, one also needs to observe that the ETF fought the median a number of compression from 11.9x on its first buying and selling day to about 7.1x now. Had the valuation paradigm stayed at 11.9x, you’d have a geometrical compounding of +67% extra, theoretically pushing the +21.6% return proven above to about +100%, nicely above the Nasdaq & S&P.

There’s spectacular relative outperformance to the a number of paradigms due to natural gross sales development within the class.

At right this moment’s 7x, regardless of the macro situations and the present treasury yield, I believe it is time to get into software program for many who aren’t in it already. We have now come full circle, the harm is finished, and whereas it might look like you are catching falling knives, the basics paint a vastly completely different image in comparison with the economic system. Software program is not a complement to an enterprise’s operations. It IS an enterprise’s operations – the spine of each sizeable enterprise. The transformation is much from over.

Even when the 7x vary pushes downward, shares which are organically rising will seemingly struggle these multiples throughout time. Development investing is time arbitrage in any case.

The place Are The Looking Grounds?

If one’s nonetheless involved about macro, cybersecurity gives a macro resiliency like no different although I would say the market has recognised and priced the gamers appropriately with excessive valuations. You may’t actually go too mistaken with massive names like Microsoft which is extra deeply built-in into the operations of contemporary enterprises than every other firm. Amazon appears good on account of AWS, countered by their e-commerce operations that do not appear to ever make any actual cash.

Nevertheless, in case you are trying to find the subsequent MongoDB, HubSpot, or ServiceNow, you may need to work a little bit more durable. In my commentary, it’s considerably harder to go from a $50B firm to a $200B firm than it’s for a $5B firm to go to a $20B firm. For pure alpha, search within the mid-cap (<$10B) area and dig deep into rising sub-technologies throughout the software program class. Stellar administration, product differentiation, and excessive high quality engineering all assist. Services and products ought to have worth propositions that seem like no-brainers from a buyer’s standpoint. As an example, the infrastructure and warehousing value financial savings from switching to Snowflake are frankly ridiculous for a lot of pre-cloud or multi-cloud firms which have siloed up their knowledge. There is a purpose why Snowflake boasts a 170% retention charge and 80% gross sales development.

At The Summary Portfolio, I am used to searching within the high-growth area the place the long-term time-arbitrage is commonly highest however so is the chance of underperformance, capital loss, and uncertainty. It comes as no shock that valuation multiples within the brief time period are additionally the best right here, however when correctly contextualized, they will look very low-cost towards a 5-year forecast. Some rising software program areas I am preserving monitor of are:

- Software program for Software program: DevOps, Observability, and Automation Software program

- Workflow Administration Platforms

- New Advertising/Engagement Platforms

- Information Science and Synthetic Intelligence, and something actually that touches knowledge

- Cloud-based cybersecurity

- Israel-domiciled software program – the place engineering salaries do not eat a lot into backside strains regardless that the product high quality is superb

- Companies that may’t be in comparison with anything – by differentiation, these firms have moats

In essence, there are areas of enterprise which are lower than 1 / 4 of the best way up their class’s S curve. Meaning they’ve a market alternative a number of multiples greater than their present gross sales. Some operators within the above areas have the possibility to 5x or 10x their gross sales as they exponentially develop.

For extra risk-averse buyers, mature free money circulate generative firms with 20-40% development look like good areas however I would stress on figuring out critical aggressive benefits and a few semblance of development along with management. Tech is a “develop or die” sector and economies of scale work scarily nicely in software program making the third/4th finest participant in a class typically die a drawn-out demise or low-cost buyout. If it is too low-cost, run the opposite manner in case of a worth entice. There are, after all, exceptions to those guidelines for stylish stock-pickers.

On the ETF aspect, SKYY, CLOU, and NASDAQ:WCLD seem like respectable candidates providing growing ranges of danger. If nothing else, Microsoft is a staple for any portfolio at an affordable 26x Ahead P/E in the meanwhile should you’re shopping for and forgetting for the subsequent 5 years.

Concluding Remarks

Marc Andreessen famously stated: “Software program is consuming the world”. Whereas many would have approached this high-valuation sector with apprehension within the face of weakening macro, excessive inflation, a recession, rising rates of interest and yields, the precise fundamentals of a number of software program companies are demonstrating resilience. Durations of change and uncertainty increase the adoption of deflationary progressive applied sciences, regardless that this appears contradictory from a macro standpoint. I urge buyers to look previous the subsequent 3-5 years.

It’s completely doable that inflation persists and treasury yields head greater, pushing the logical foundation for valuing long-duration shares decrease. That stated, the chance/reward is immensely in our favour as multiples have shot again to the late 2017 paradigm – when the class was smaller, slower, and never fairly as exponential-growth-oriented. Regardless of the huge tech re-rating, cloud transformation stays crucial together with lots of its rising sub-industries for almost all of enterprises on the market. Whereas I am removed from a macro investor, it is price noting that oil costs have peaked, and a counter-trend on the accelerating inflation is nicely underway. Meals and vitality, the 2 relatively inelastic world provide chains tend to re-orientate for provide to satisfy demand by the regulation of the free markets. It is a matter of time.

At a time when the know-how sector is not favoured by latest traits and institutional capital, it is sensible to be a contrarian given the info and fundamentals at hand. Software program stays sturdy and also you’re getting it at a uncommon low cost right this moment – making it the very best time prior to now a number of years to speculate on the best aspect of this generational secular development.