Vertigo3d

Written by Nick Ackerman, co-produced by Stanford Chemist. This text was initially posted to members of the CEF/ETF Earnings Laboratory on August twentieth, 2022.

It has been a reasonably tumultuous 12 months for investments. Actual property hasn’t been in a position to escape the volatility. Nevertheless, that is often when alternatives come up for investments. Right now, I am seeking to revisit the closed-end REIT-focused funds to see potential alternatives.

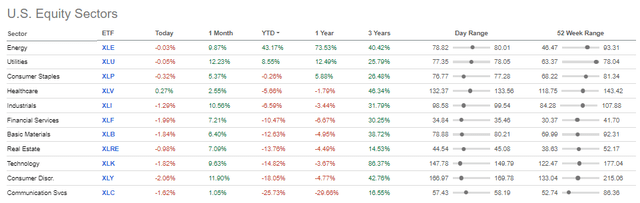

Total, actual property is within the backside half of sector performances and appears a bit counterintuitive. One of many primary causes for the bear market we noticed this 12 months was inflation. Inflation has been working extremely sizzling. Actual property is mostly thought-about a pure hedge towards inflation as property values would typically rise.

Fairness Sector Efficiency 8/20/2022 (In search of Alpha)

Nevertheless, with greater inflation comes greater rates of interest. That may make REIT operations dearer as they typically function with important borrowings to develop their operations.

Moreover, greater rates of interest have a tendency to finish with an financial slowdown or recession. A recession means tenants might have issue paying their hire on time or might fully default.

On high of all this, we at the moment are beginning to see an actual property growth finish. House gross sales fell 6% in July. That has pushed the housing market into its personal recession. Whereas that is simply properties, industrial properties present an identical gross sales decline.

I imagine that these causes are impacting the actual property/REIT sector total, regardless of the pure hedge towards inflation.

Some REIT Fundamentals

Listed here are some primary particulars of CEF REITs from our earlier take a look at the house.

REITs have been delivering a strong quantity of payouts to buyers for the reason that construction was created. This goes all the best way again to 1960. Gone are the times when you need to actively handle your individual actual property empire of bodily buildings. Let an professional workforce do it for you.

Actual property funding trusts (“REITs”) have been round for greater than fifty years. Congress established REITs in 1960 to permit particular person buyers to put money into large-scale, income-producing actual property. REITs present a method for particular person buyers to earn a share of the earnings produced by means of industrial actual property possession – with out truly having to exit and purchase industrial actual property.

Within the closed-end fund house, we will go much more passive. Let the managers decide which REIT could be finest to put money into. Although I personal a number of actual property funds, I admit that I additionally get pleasure from choosing my very own REIT investments and doing a little analysis into them.

One of many causes that REITs have constant and common payouts which can be usually greater than different securities is their construction. The REIT construction says that not less than 90% of their taxable earnings should be distributed to shareholders yearly. This matches completely effectively with regulated funding corporations (“RIC”) CEFs themselves, as they too should distribute most of their earnings. That features earnings and good points.

The Screening And Fundamental Information

In that earlier piece, I had touched on Cohen & Steers’s new fund that was coming to market. Since then, the Cohen & Steers Actual Property Alternatives and Earnings Fund (RLTY) was launched shortly after that posting. So with that, our little world of eight actual property CEFs grows to 9.

The information is primarily from CEFConnect as of 8/19/2022. Extra information was gathered from the sponsor web site for RLTY.

| Title | Ticker | Premium/Low cost | 52 Wk Avg | Distribution Price | Efficient Leverage | Baseline Expense | 5-12 months NAV | 10-12 months NAV | 5-12 months Value | 10-12 months Value |

| Aberdeen International Premier Properties | (AWP) | -3.71% | -4.82% | 9.25% | 21.40% | 1.19% | 2.59 | 5.53 | 5.41 | 7.4 |

| CBRE International Actual Property Earnings | (IGR) | -4.20% | -6.49% | 9.28% | 25.34% | 1.24% | 5.92 | 5.63 | 8.89 | 7.39 |

| Cohen & Steers High quality Earnings Realty | (RQI) | -3.38% | -2.98% | 6.34% | 24.21% | 1.28% | 10.18 | 10.95 | 11.44 | 11.83 |

| Cohen & Steers Actual Property Opp & Inc Fd | (RLTY) | -8.58% | N/A | 7.19% | 31.71% | 2.07%*** | ||||

| Cohen & Steers REIT & Most popular Inc Fd | (RNP) | -3.52% | -3.69% | 6.77% | 26.34% | 1.04% | 8.42 | 10.29 | 10.21 | 11.32 |

| Cohen & Steers Complete Return | (RFI) | 3.46% | 5.27% | 6.56% | 1.52% | 0.89% | 8.74 | 9.07 | 11.39 | 9.92 |

| Neuberger Actual Property Securities Earnings | (NRO) | -4.26% | -2.64% | 8.77% | 24.86% | 1.21% | 3.68 | 6.12 | 5.5 | 7.75 |

| Nuveen Actual Property Earnings | (JRS) | -4.45% | -5.01% | 8.29% | 32.08% | 1.27% | 6.04 | 8.05 | 5.54 | 7.28 |

| Principal Actual Property Earnings Fund | (PGZ) | -9.00% | -12.27% | 9.30% | 33.02% | 2.15% | 1.68 | 1.18 |

Above, we will see the 9 funds which can be recognized as “actual property” by CEFConnect. I’ve included the title, ticker, premium/low cost, 52-week common low cost, distribution fee, efficient leverage and baseline bills. Along with these essential metrics, I’ve additionally included the 5 and 10-year whole NAV and share worth returns in the event that they have been out there.

A number of broad observations:

- The common low cost of the listing is 4.18%, solely narrowed barely from the 4.27% it was on 2/4/2022

- The common 1-year low cost is analogous at 4.08%

- The common distribution yield of those funds involves a wholesome 7.97%, that is meaningfully greater than the 6.8% beforehand

- Efficient leverage employed involves 24.50%, an increase from 21.01% as asset costs have come down, which is actually why the yields have gone up

- The common expense ratio involves 1.2% (***excluding RLTY as they report a 2.07% expense ratio, however that appears to be together with leverage, we’ll get a greater concept once they report their first annual report)

- 5-year common NAV annualized returns come to five.90%, in comparison with share worth annualized returns of seven.44%

- 10-year common NAV annualized returns come to 7.95%, in comparison with the share worth annualized returns of 8.98% (PGZ and RLTY have not been round lengthy sufficient to supply figures right here)

As I discussed, I am simply on the lookout for a fast replace on every of those funds. In order for you the extra primary information, I’ve beforehand coated nearly all of those funds for discussions of their funding insurance policies. I am scripting this with the belief readers have a primary baseline of understanding of those funds already.

RLTY And PGZ

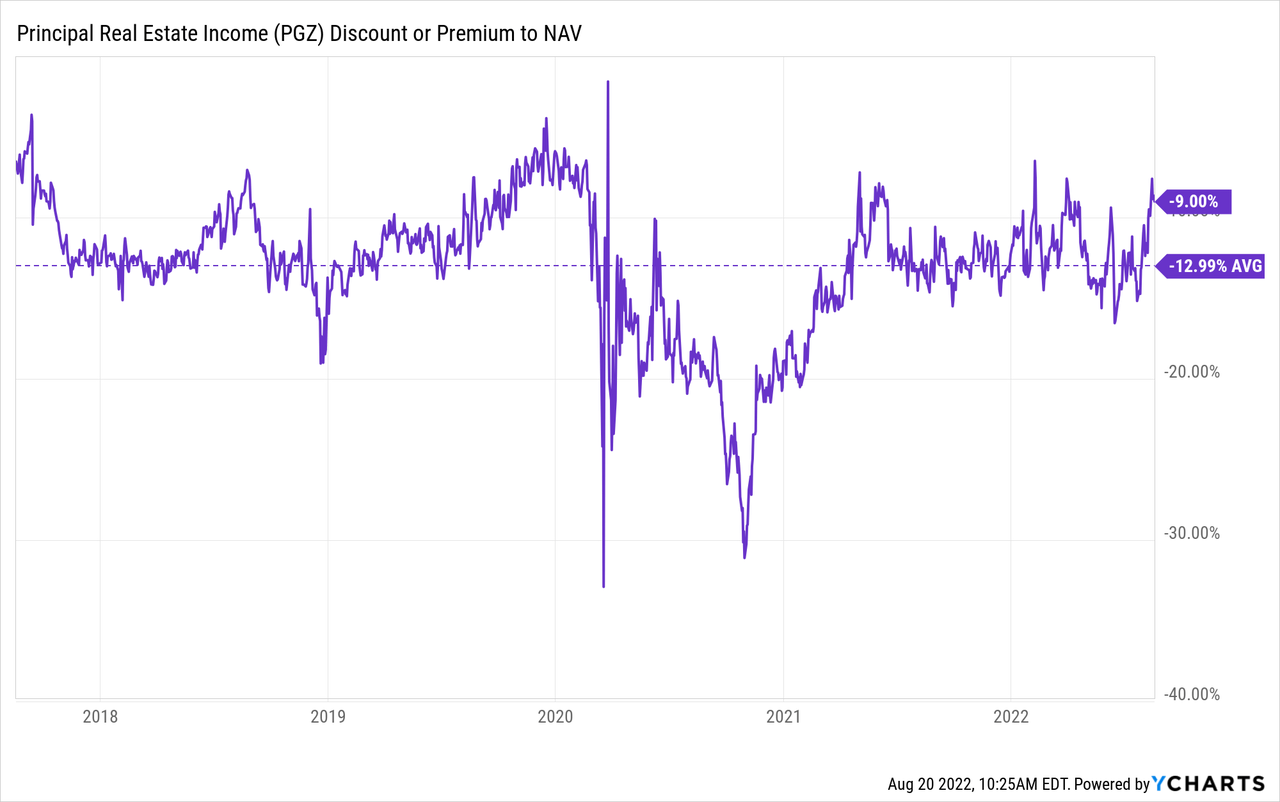

These two actual property funds are fairly totally different from one another however are exhibiting the deepest reductions. RLTY focuses on fairness REITs and most popular holdings. PGZ is the extra distinctive fund right here that focuses closely on CMBS publicity. It is also the fund with the very best distribution fee right now.

RLTY being a brand new fund is a bit anticipated as a result of buyers are inclined to dump the funds till there is a longer monitor document. For PGZ, although, the fund’s low cost could be the widest, however based mostly on the final 12 months’s common, it won’t be a screaming purchase.

Going again even additional, over the past 5 years, we will see that PGZ continues to be elevated. That is typically what we have seen over the complete CEF house currently, valuations narrowing as soon as once more. That was after the broader market had made new lows however has subsequently been recovering since June.

Ycharts

I imagine that RLTY is certainly attention-grabbing at these ranges. It could possibly be value contemplating if an investor is on the lookout for extra retail publicity. As we’ll focus on beneath, its sister funds, RQI, RNP and RFI, have supplied the very best returns of the house.

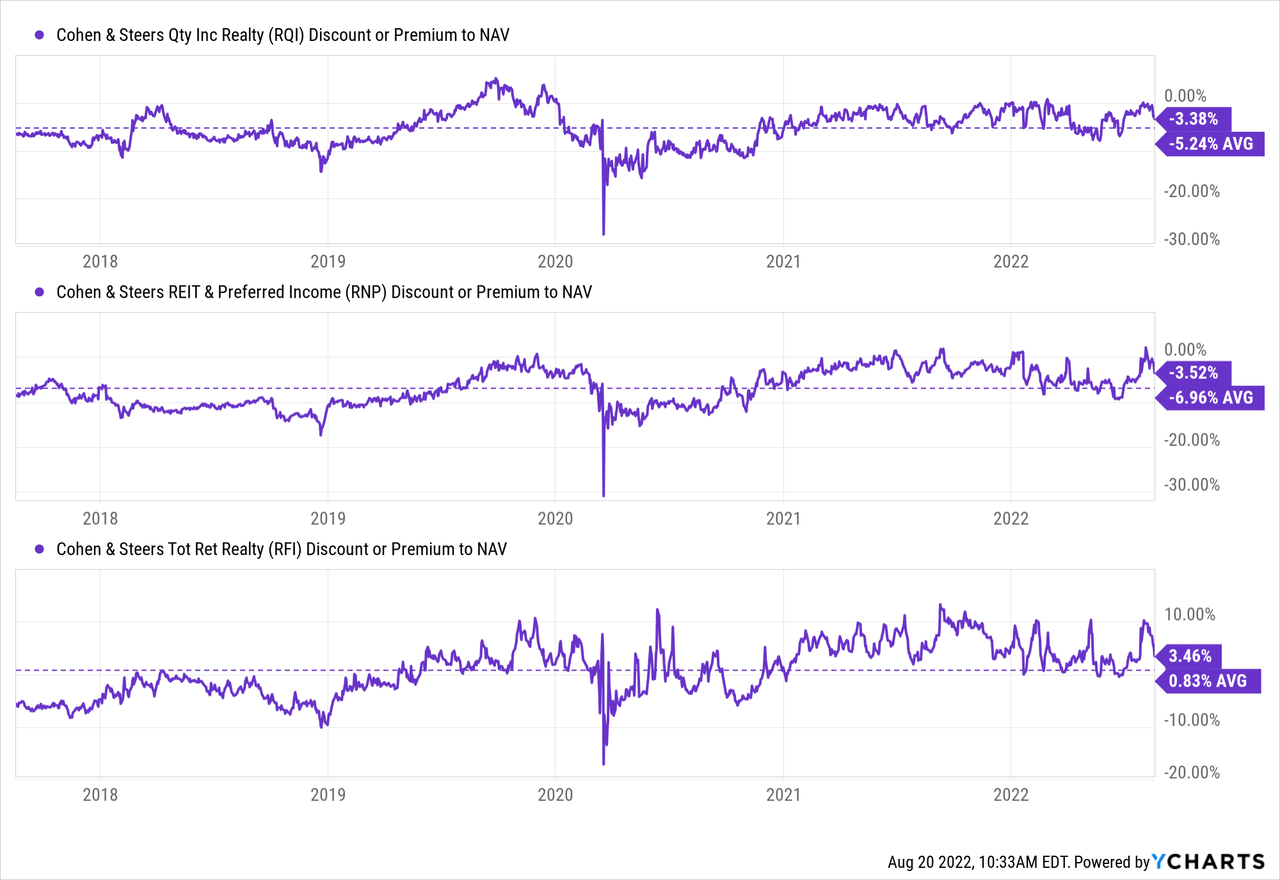

RQI, RNP And RFI

These are the highest performing three funds over the long term. RQI comes out because the strongest on each efficiency metric proven above; the 5-year NAV and share worth, in addition to the 10-year NAV and share worth. That is then adopted by both RNP or RFI in every class. For the longer 10-year interval, it has been RNP. Naturally, actual property has supplied comparatively enticing long-term outcomes, and RQI and RNP are each leveraged. RFI is sort of just like RQI however does not function with leverage.

That being stated, all three of those funds are comparatively costly based mostly on their historic valuation. RFI sometimes instructions a premium out of the group, however even that premium is barely elevated right now. Here is a take a look at the low cost/premiums and the averages of these over the past 5 years.

Ycharts

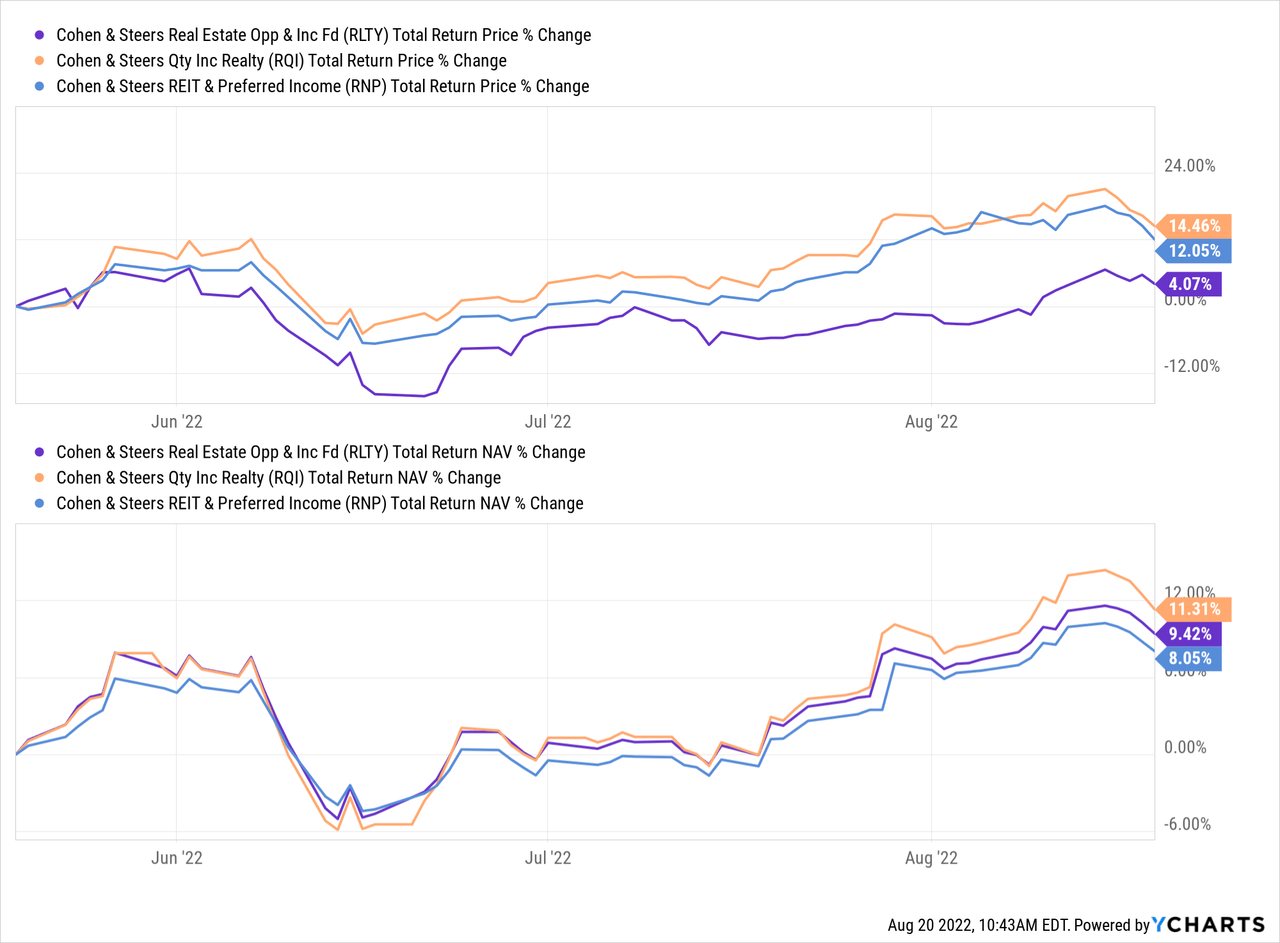

Based mostly on these valuations, RLTY could possibly be of curiosity right now. If they’ll produce their actual property magic prowess as soon as once more, RLTY has the very best probability of being the highest performing within the house going ahead.

On a complete NAV return foundation, RLTY’s efficiency is correct between RQI and RNP.

Ycharts

That is per what I considered as RLTY being an in-between fund of RQI and RNP. RQI holds principally fairness REITs with solely a small publicity to preferreds. RNP is a fund that is typically break up round 50/50 between the 2 property. RLTY is the center floor of round a 70/30 break up of fairness and most popular.

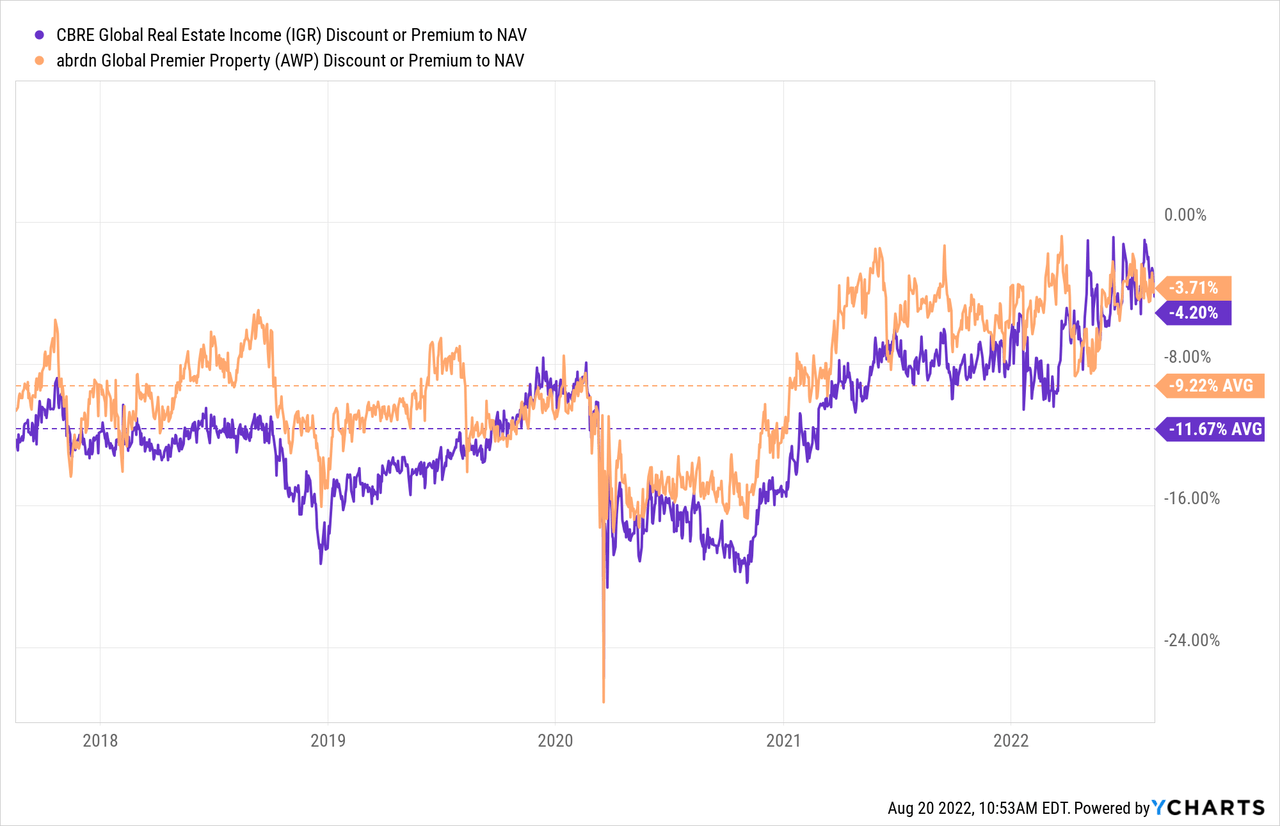

IGR And AWP

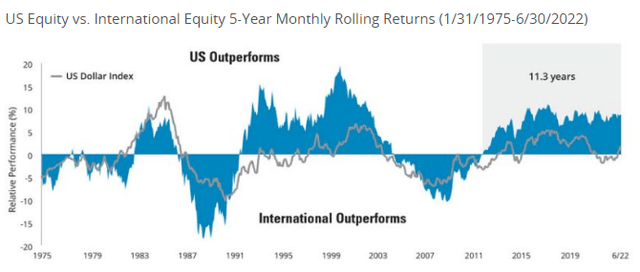

These are the global-oriented funds of the house. They’ve typically completed the poorest of the group. On a complete NAV return foundation, it goes AWP because the worst and IGR because the second worst. For the five-year whole NAV return foundation, it has AWP because the worst, then NRO after which IGR.

The explanation for this appears pretty easy, U.S. investments have been outperforming their worldwide counterparts for many of the final decade. That is not to say that this occurs on a regular basis, so making an attempt to keep away from recency bias is essential. There have been a number of intervals the place the reverse has been true.

U.S. Vs. Worldwide (Hartford Funds)

Based mostly on valuations being much more depressed than U.S. investments, it might assist result in worldwide being the highest performing as soon as once more.

That being stated, IGR and AWP are pushing towards their historic valuations. It could seem different buyers have the identical concept in thoughts, that worldwide investments are cheaper and will outperform. Due to this fact, they appear to be crowding into these funds way more than typical.

Different CEFs as an entire went to traditionally elevated valuations in 2021, then widened out in 2022. IGR and AWP appeared to have bucked that development and simply stored going greater. AWP did dip barely first, then head greater, although.

Ycharts

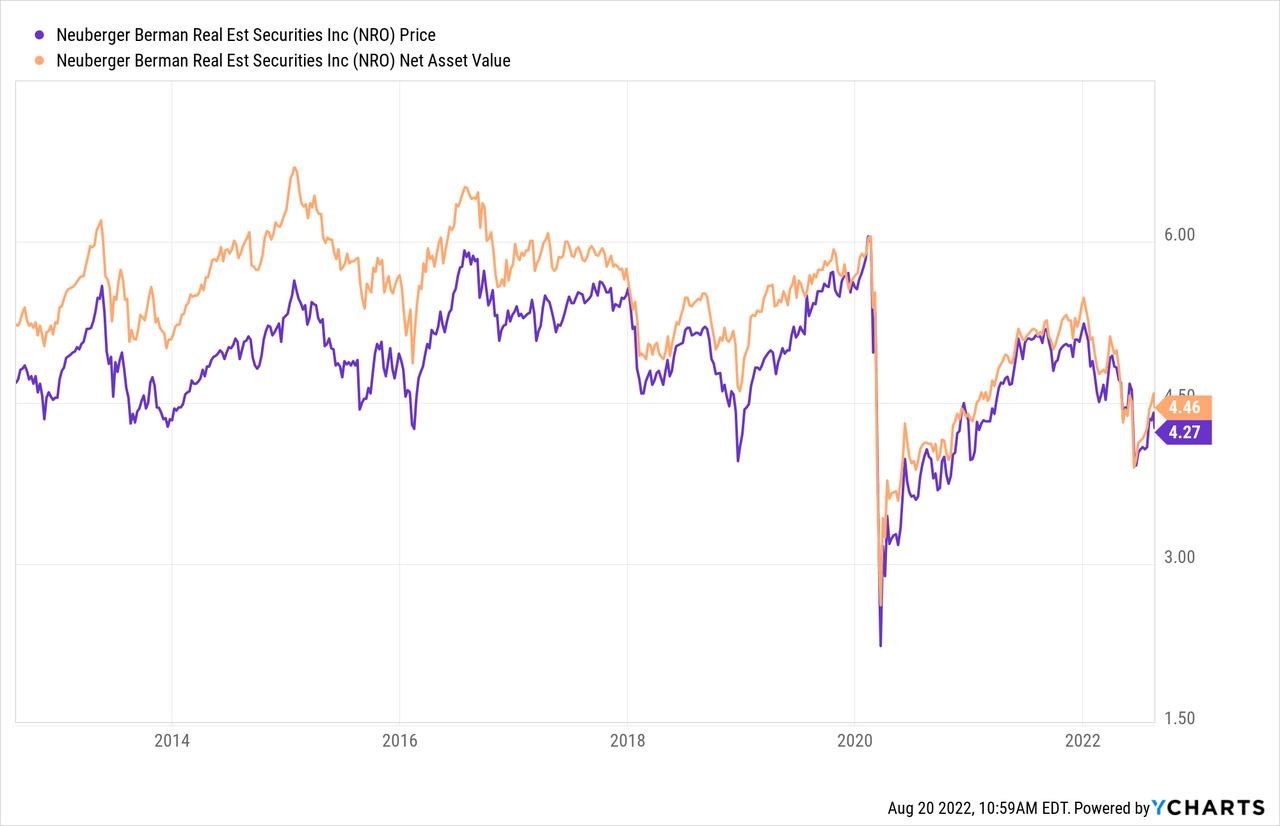

NRO

NRO has the excellence of being one of many extra performing actual property funds. Since they’ve a sizeable allocation to preferreds, we might anticipate the outcomes to be extra tempered. Nonetheless, RNP has a equally weighted portfolio, and so they’ve been one of many high performing within the house.

One factor that has damage NRO over time has been deleveraging. In 2017, they’d $124.9 million in borrowings. This then went to $100 million in 2018 and 2019. With the extreme sell-off as a consequence of COVID in 2020, they have been compelled to slash their borrowings to only $45 million. That brought about everlasting injury as every part rebounded sharply off these lows.

Ycharts

Right now, they sit at $70 million in borrowings, by no means recouping the degrees beforehand attained. It seems that being extra reasonably leveraged, round 25% lately, would depart them in a extra versatile place of not being compelled to deleverage. When a fund deleverages, it usually damages the fund completely. I do not suspect NRO will ever recuperate to these prior highs.

That being stated, I would not thoughts proudly owning NRO once more for brief intervals. It must be at a a lot deeper low cost. I would really feel comfy round 10%+. When you possibly can make investments with the very best, why mess with the remaining? On this case, RLTY is an excellent higher take care of a fund sponsor with a significantly better monitor document. In fact, previous outcomes do not assure future returns.

JRS

JRS has suffered an identical destiny to NRO, having to deleverage throughout tough patches. Right now, CEFConnect studies greater leverage than their web site. The distinction right here seems to be that they took down a few of their leverage since they final reported. I think we as soon as once more noticed that with the June lows, their leverage elevated an excessive amount of, and so they needed to dump a few of their portfolio. That is what I highlighted in my latest JRS replace.

Sadly, it does not seem that the administration workforce with JRS has discovered any classes with their elevated leverage use. I say sadly as a result of that is one which I proceed to carry myself. Since my replace, the low cost has narrowed a bit, making it much less interesting to purchase now.

I proceed to carry this place as a result of I like that it brings totally different actual property publicity to the desk. It, too, has a versatile technique of investing in fairness REITs and most popular inventory. On this case, they create sizeable allocations to residential and workplace REITs. I am not a lot of a fan of workplace REITs, however some publicity is not essentially horrible.

If we take a look at RQI and RNP, we see much less publicity to those areas. As an alternative, they appear to give attention to extra growth-focused REITs.

Conclusion

Actual property hasn’t been a spot to take shelter in 2022. Nevertheless, no place apart from power and utilities has been a very robust space to put money into both. For the CEF house, I imagine that RLTY brings up a compelling alternative for these seeking to put some capital to work within the REIT house. As a more moderen fund, I would not anticipate the low cost closing quickly. It’s a potential bonus if or when it does, although. If we get an extra pullback from the most recent rally and reductions widen, I feel RQI, RNP and RFI would supply enticing long-term alternatives too.