MaxImages/iStock Unreleased by way of Getty Photos

Amazon.com, Inc. (NASDAQ:AMZN) has been navigating a tough enterprise surroundings for the previous few years. The pandemic led to skyrocketing demand for the whole lot ecommerce but in addition froze the provision chain. Demand for cloud providers additionally jumped, as companies had been pressured to accommodate clients and distant workers whereas places of work and storefronts had been closed. This led to nice enterprise efficiency for Amazon in 2020 because the retail and AWS segments benefitted vastly. Income elevated 37% within the yr whereas working revenue elevated 57%. The inventory adopted swimsuit and rose 75% that yr.

This introduced Amazon into a large, multi-year funding cycle so they might meet this newfound demand. Responding to buyer wants is a typical Amazon response so these investments made sense on the time, however the scenario was something however typical. Nobody knew the long term results of the pandemic on the worldwide economic system, client habits, or distant work. Nonetheless, Amazon dove headfirst into this funding cycle.

Sadly for Amazon, demand did normalize to extra of a typical development, and earnings subsequently dropped as income progress slowed and working expense progress elevated. This brings us to the current and the present alternative that exists for traders. Is Amazon now structurally much less worthwhile and can earnings stay depressed? Or will Amazon reap the rewards of the large investments it has remodeled the previous two years? I’m inclined to imagine the latter, and I believe Amazon.com, Inc. inventory is undervalued due to it. I come to this conclusion by inspecting the present traits within the financials, and by inspecting earlier funding cycles and their outcomes on Amazon’s earnings.

Previous Funding Cycles

Amazon is rarely too clear about its plan for funding cycles. The overall reply to analyst questions on investments is one thing alongside the strains of “we’re investing for long run progress and we’ll proceed to try this as we see match.” Over the previous ten years there are two distinct funding cycles that I believe are useful to look at to present traders a greater concept of what 2023 holds for Amazon. These two intervals of huge funding had been in 2014 and 2016-2017.

2014

In 2014, capital expenditures grew 42% over the earlier yr. Together with this, working bills grew 33% from the earlier yr. These investments had been made to assist long run progress of the retail phase and AWS. This spending led to a 76% yr over yr discount in working revenue for the yr.

The yr after in 2015, funding slowed as capital expenditure spending declined 6% and progress in working bills decelerated to 27%. Consequently, working revenue elevated 1100%+ that yr and the inventory worth adopted because it posted a achieve of over 100%. The slowdown in working bills was a giant contributor to this soar in working revenue, however a soar in gross margin proportion together with sustained income progress additionally performed a big function.

2016-2017

Amazon.com, Inc. capital expenditures grew 47% and 49% in 2016 and 2017 respectively. In those self same years, working bills grew 31% and 42%. Working revenue did improve 87% in 2016 regardless of this progress in funding spending, however it declined about 2% in 2017.

The identical factor that occurred in 2015 after the 2014 funding cycle, additionally occurred in 2018. Each capital expenditures and working bills grew at a a lot slower fee than the prior years, all whereas income progress was sustained and gross margin jumped one other few proportion factors. This led to a 200% improve in working revenue and a 30%+ improve within the inventory worth in 2018. This isn’t fairly as spectacular because the 100% improve within the inventory worth in 2015 however within the context of a 4% decline of the NASDAQ composite index in 2018 it’s a very robust relative efficiency.

Most Current Cycle

The funding cycle of the previous few years is a little more advanced given the scenario with the pandemic because it created a really unsure international financial surroundings. However at a primary degree, the information of this cycle are the identical as those in 2014 and 2016-2017.

In 2020, capital expenditures elevated a whopping 176% from the prior yr and went up one other 58% in 2021. Working bills additionally grew 29% and 33% in 2020 and 2021. What’s a bit completely different from previous funding cycles is that working revenue grew fairly a bit in each years. That is as soon as once more as a consequence of a giant 37% improve in income in 2020 and rising gross margin proportion. The inventory adopted working revenue and rose 70%+ from the in 2020.

The funding cycle got here to an finish in 2022 when Amazon administration realized their investments led capability to exceed demand. Nevertheless we’re not seeing the standard rise in working revenue that comes on the finish of those funding cycles. By way of the primary 9 months of 2022 versus the primary 9 months of 2021, capital expenditures grew solely 10% and working bills grew at a slower albeit nonetheless quick fee of 25%. The primary problem is that up to now in 2022 income has solely grown 10%. Regardless that the gross margin proportion has risen, expense progress grew at greater than double the speed of income progress which has led to a 55% decline in working revenue up to now in 2022. The inventory is down 50% yr up to now so it has as soon as once more adopted working revenue. Clearly, 2022 was a foul yr for many shares, however do not forget that in 2018 when the NASDAQ index dropped for the yr, Amazon’s inventory rose 30% due to the rise in working revenue.

This makes the query for 2023 and past clear: what is going to occur to Amazon’s working revenue?

2023 Forecast

Amazon’s working revenue in 2023 will rise if income grows, bills are managed, and gross margin rises. And if working revenue rises above expectations, the inventory worth will rise.

Income

Income progress is dealing with two primary headwinds in 2023. First, if the greenback stays robust versus different currencies there will probably be FX headwinds. The headwind in 3Q 2022 was 460 foundation factors. Second, basic macroeconomic weak point will harm gross sales progress on all fronts. Each the robust greenback and the present financial weak point are brought on by the actions of the federal reserve so each may probably be solved by actions of the federal reserve. If inflation dissipates convincingly, Jerome Powell and the fed may pivot. Moreover, the ECB can also be getting extra hawkish, which can assist strengthen the Euro towards the Greenback.

The income headwinds of 2022 may flip into tailwinds in 2022. Analysts are predicting 11% income progress in 2023. Including again 4.5% to cancel out the FX results and some proportion factors to account for an improved economic system and income progress might be 18% in 2023.

Working Bills

Wage inflation, particularly amongst tech employees, has added considerably to working bills over the previous few years. Nevertheless, with the latest layoffs and hiring freezes from tech firms, these pressures may ease in 2023. Amazon has already proven resolve to cut back working bills in loss producing segments. They first introduced layoffs of 10,000 workers, many from the Alexa division which was reportedly on tempo to lose $10 billion this yr, however the quantity lately upped to 18,000. That is along with freezing company and AWS hiring into 2023. The dedication to lowering headcount will result in a lot decrease working bills in 2023. The tip of previous funding cycles have introduced upwards of 10% reductions in working bills so working expense progress may decelerate to twenty% in 2023.

Gross Margin

Value of gross sales go up at Amazon as a consequence of “elevated product and transport prices ensuing from elevated gross sales, elevated investments in our achievement community, elevated transportation prices, and elevated wage charges.” Decrease power and gasoline prices, together with a better portion of complete income from the upper margin segments, and fewer hiring and funding for the achievement community will assist decrease gross margin in 2023.

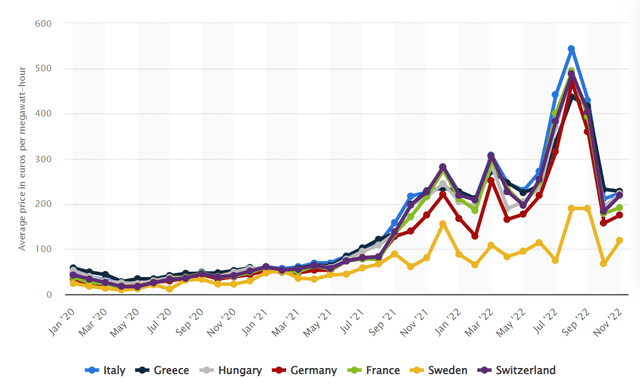

Beneath is a chart of power costs in Europe. They’ve been elevated all through 2022 and have contributed considerably to value of products for AWS.

European Vitality Costs (Statista)

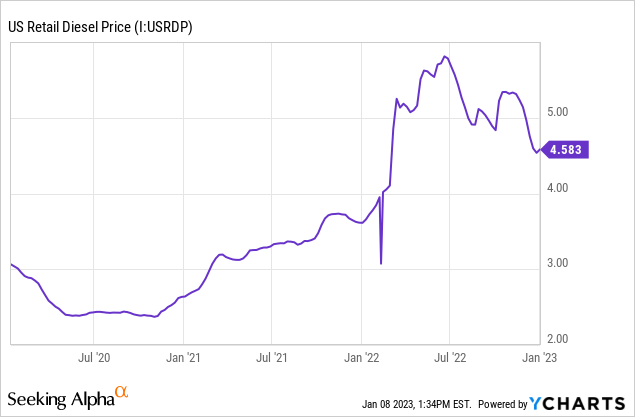

Beneath is a chart of U.S. diesel costs, which add prices to the retail phase. Like electrical energy costs in Europe, these costs have been elevated by 2022 and will probably be a tailwind for gross margin as they proceed to drop by 2023.

I may see gross margin rising by 200 foundation factors from these value financial savings. Up to now in 2022 gross margin has been 44.3%, so I’ll forecast gross margin at 46.3% in 2023.

Forecast

Combining my forecasted income progress, gross margin and working expense progress we are able to arrive at an working revenue forecast for 2023. 18% income progress from analyst projections of FY 2022 income of $511 billion is $603 billion. Making use of a 46.3% gross margin to this income determine results in $285 billion of gross revenue. If working bills improve 20% from $216 billion (my projection of 2022 working bills) 2023 working bills can be $259 billion. This could result in working revenue of $20 billion for 2023.

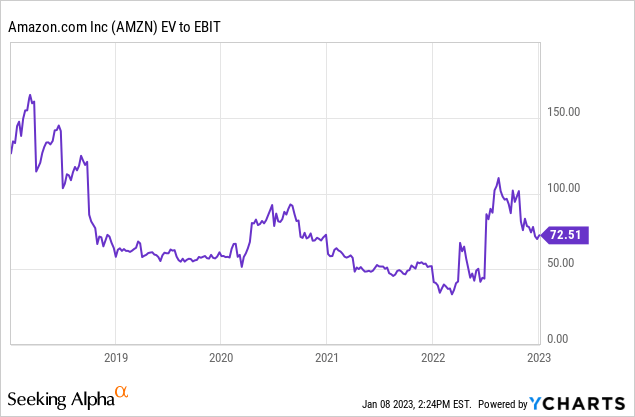

As seen from the chart above, the trough EV/working revenue a number of from the previous 5 years is 60, so making use of this a number of to $20 billion of working revenue brings us to an enterprise worth of $1.2 trillion versus the present enterprise worth of $900 billion. This represents 33% upside for the inventory. In fact my assumptions are optimistic however I like the chance/reward as I believe earnings will proceed to rise within the years past 2023 as the corporate slows general funding and continues to reap the rewards of the pandemic funding cycle.

Dangers

The primary dangers contain the economic system and macroeconomic forces. If the U.S. and the world go right into a deep recession, income gained’t develop 18%. Administration already talked about within the 3Q earnings name that AWS clients had been very targeted on value chopping. On prime of this advert spending would drop considerably.

These elements would harm income progress however may assist with lowering prices as gasoline, power costs, and wages would drop. A recession would trigger inflation to drop, permitting the federal reserve to pause or reduce charges. This might lead the greenback to drop versus different currencies. So whereas value chopping may enhance on this scenario, income progress can be lower than 18% and gross margin would probably not rise as a lot as a consequence of much less progress in advertisements and AWS, the upper margin segments.

Nevertheless the inventory is already at a trough a number of on working revenue from 2022, a yr that Amazon considerably underearned. With value chopping measures and the drop in power costs I’ve a tough time believing that earnings will drop a lot from 2022. This leads me to imagine that potential upside is increased than the draw back and the present setup for 2023 and past is favorable for Amazon traders.

Ultimate Ideas

At immediately’s worth, I believe Amazon inventory provides a beautiful danger/reward. It’s presently buying and selling at a trough a number of on trough earnings and administration is dedicated to chopping prices as seen from latest layoffs and hiring freezes. These measures ought to maintain earnings from falling from these present depressed ranges even when a worldwide recession hits. It could take main a number of compression from an already depressed a number of, to take the inventory down way more from present costs. Alternatively with my optimistic assumptions above, upside might be as excessive as 33% for the inventory in 2023.

Even when the optimistic state of affairs doesn’t play out, an funding in Amazon may be bailed out with a long run holding interval. Administration is continually fascinated with long run progress and for my part, AWS is without doubt one of the greatest companies on Earth. This sort of administration together with these cloud computing tailwinds can solely result in good issues for Amazon over time.