Leonid Sorokin

This fall 2022 Worth Investor’s Quarterly Letter

“Now we have bought to get inflation behind us. I want there was a painless manner to do this. There isn’t.”

― Jerome Powell, September 22, 2022

In August at Jackson Gap, Wyoming, present Chairman of the U.S. Federal Reserve Jay Powell stated that the nation’s central financial institution, “should maintain at it till the job is finished.” The phrase “maintain at it” paid tribute to former Chairman of the Federal Reserve Paul Volcker and his memoir Retaining At It: The Quest for Sound Cash and Good Authorities. In 1979, when Paul Volcker was appointed Chairman of the Federal Reserve, rates of interest have been traditionally excessive, but inflation was nonetheless larger. With its institutional behavior of creating small, incremental modifications to the low cost fee, Volcker thought that the Federal Reserve was dropping credibility.[1] If inflation is simply too many {dollars} chasing too few items, fewer {dollars} would imply much less inflation; subsequently, Volcker determined to straight goal the cash provide.

Volcker unveiled his new insurance policies throughout a uncommon press convention on October 6, 1979, the Saturday earlier than Columbus Day.[2] The Federal Reserve elevated the low cost fee to 12% and elevated deposit reserve necessities as nicely. Volcker ‘saved at it’ till U.S. Treasury-Payments maturing inside ninety days reached yields of 17%. Volcker needed short-term charges to rise however for long run charges to stay decrease, a sign that the market was assured the Federal Reserve might management inflation. Underneath Chairman Volker, the Federal Reserve ultimately raised the federal funds lending fee to twenty% to fight inflation that had soared to 13.5%–attributed to a spike in oil costs that pushed the price of items up and ignited a persistent improve in shopper costs. Three years later, inflation had plummeted to three.2%. With this success, the Federal Reserve regularly decreased the federal funds fee, prompting a declining-interest-rate surroundings that prevailed for the subsequent 4 a long time.

Investor success during the last forty years might have largely been resulting from this multi-decade tailwind of decrease rates of interest, a pattern that fueled an age of entry to low cost capital. This favorable surroundings has now ended, and buyers are confronting an rate of interest headwind. Rates of interest hit an all-time low in 2008 after the Federal Reserve minimize the federal funds fee to zero to rescue the economic system from the Nice Monetary Disaster. From 2009 to 2020, when the pandemic started, america loved its longest financial increase in historical past. This period doubtless ended this 12 months, with resurgent inflation and better rates of interest. Because it’s doubtless inflation and rates of interest will dominate the funding surroundings for the rest of the last decade, funding methods that labored exceedingly nicely may battle within the years to return.

Having promised to emulate the anti-inflationary footsteps of Paul Volcker, Jay Powell continues to “maintain at it.” The potential drawback is that Volcker’s world was far faraway from that which exists immediately. There isn’t a worldwide push to extend fossil-fuel manufacturing to fight spiking vitality costs. Fairly the opposite, interventionist politics, inexperienced vitality transition initiatives and labor shortages characterize immediately’s vitality coverage surroundings. Coupled with the rising motion to “rearm, reshore and restock” home manufacturing capabilities, inflation might show harder to tame than anticipated. Volcker was audacious in his actions towards unimaginable political stress, however he additionally benefited from an economic system that carried far much less debt on its collective stability sheet. Whereas Wall Avenue continues to eagerly anticipate an imminent shift in Federal Reserve coverage, inflationary pressures stay excessive. After falling far behind the inflation curve following the pandemic, the Federal Reserve has raised the low cost fee by 4.25% in solely 9 months, the sharpest improve in charges within the Federal Reserve’s 108-year historical past, comparable solely to the aggressive actions below the management of Paul Volcker in 1980.

Berkshire Hathaway buyers readily acknowledge one in all Warren Buffett’s extra colourful sayings: “You solely discover out who’s swimming bare when the tide goes out.” One by no means actually is aware of or appreciates the dangers corporations take till they’re examined by antagonistic circumstances. This 12 months’s mixture of inflation and rising rates of interest have created a perverse surroundings the multi-decade tailwind of falling rates of interest managed to cover. The current collapse of the cryptocurrency trade FTX is probably a harbinger of the altering funding panorama. FTX’s debacle has uncovered simply how little due diligence takes place amongst buyers prepared to chase the shiniest new object that guarantees outsized returns.

Sam Bankman-Fried, a thirty-year outdated MIT graduate generally known as “SBF,” based after which subsequently destroyed FTX by inserting management of his shoppers’ cash within the palms of a small variety of buddies with no expertise, information, or scruples about the best way to responsibly handle funding funds. Monetary document maintaining and reporting on the firm have been chaotic at greatest. FTX misplaced round $2 billion of shopper funds, to not point out billions of {dollars} invested within the firm’s fairness that merely evaporated. Sadly, 1000’s of shoppers positioned cash within the FTX trade with some placing of their total life’s financial savings. One wonders why so many have been prepared handy over their livelihood to an operation run by a man-child in shorts who was not accountable to anybody…..however the easy reply is the fear-of-missing-out (FOMO) on potential earnings.

Whereas information headlines centered on the losses suffered by retail buyers, it’s the institutional buyers who must be taken to process. Sequoia Capital, a widely known enterprise capital agency, invested $210 million into FTX. “Due diligence” concerned a last-minute Zoom name with Bankman-Fried throughout which he performed the online game League of Legends. In the course of the Zoom name with Sequoia to safe extra funding for FTX, SBF clicked away on his recreation controller whereas telling Sequoia that he needed “FTX to be a spot the place you are able to do something you need together with your subsequent greenback. You should buy bitcoin. You may ship cash in no matter foreign money to any buddy wherever on the earth. You should buy a banana. You are able to do something you need together with your cash from inside FTX.” Listening to SBF’s imaginative and prescient for FTX, Sequoia’s aspect of the Zoom name grew more and more excited. “I LOVE THIS FOUNDER,” typed one companion. “I’m a ten out of 10,” pinged one other. “YES!!!” exclaimed a 3rd companion of Sequoia.[3]

Regardless of institutional enthusiasm for FTX, there have been warnings. CME Chairman and Chief Govt Officer Terry Duffy recalled his first assembly with Sam Bankman-Fried again in March 2022. Duffy’s instincts from years of buying and selling within the pits stay sharp and he immediately pegged FTX as a fraud earlier than the corporate blew up. Duffy recalled how SBF approached him at a convention and advised him that he needed to compete with CME in crypto buying and selling. As a substitute, Duffy supplied CME’s crypto franchises in trade for working collectively, however SBF instantly turned him down. Later that spring, Duffy went to Congress and particularly made claims that FTX had put aside inadequate monetary assets to again its proposed direct clearing mannequin for crypto derivatives. As a substitute of appearing on Duffy’s evaluation, Congressman Ro Khanna berated Duffy for making false statements.[4]

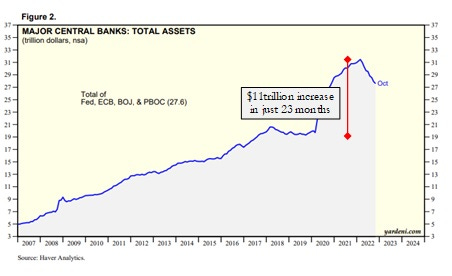

FTX is barely the latest instance of troubled crypto exchanges, however FTX might have saved its issues hidden longer if the U.S. Federal Reserve didn’t improve the price of short-term lending charges. Many buyers neglect that when the straightforward cash spigot is flowing, even outright frauds will be made to look legit—it typically requires solely the smallest quantity of financial tightening to reveal the con. Whereas extreme use of leverage turbocharged the cryptocurrency bull market that began in 2020, the tidal wave of liquidity unleashed by central banks within the face of the Covid pandemic additionally performed a significant half on this disastrous episode. Between March 2020 and February 2022, the G4 central banks (US, Europe, Japan, UK) added $11 trillion to their collective stability sheet. This liquidity wave swamped not simply cryptocurrencies however bond, inventory, and commodity costs too.

Fourteen years in the past the Federal Reserve launched its quantitative easing initiative in response to the unfolding international monetary disaster. That preliminary announcement, which detailed plans to buy $100 billion in company debt and $500 billion of mortgage-backed securities by the tip of 2008, preceded comparable undertakings that culminated within the pandemic-era, $4.4 trillion splurge spanning March 2020 by early 2022. Curiosity-bearing property on the Federal Reserve’s stability sheet at present stand at $8.6 trillion, up from lower than $1 trillion shortly earlier than Lehman Brothers collapsed in 2008. The Federal Reserve now holds $5.6 trillion in U.S. Treasurys, equal to 22.7% of the $24.4 trillion in federal debt held by the general public, in comparison with $476 billion and a 7.4% share, respectively, in November 2008.

How the Federal Reserve will take away such an unimaginable sum of cash from their stability sheet is anybody’s guess, however in accordance with then-Federal Reserve Chairman Ben Bernanke, there is no such thing as a want to fret. In a February 2011 testimony in entrance of the Home Price range Committee, Bernanke dismissed any issues and argued that the then-$2.5 trillion stability might simply be decreased as soon as monetary circumstances improved: “Federal debt monetization would contain a everlasting improve within the cash provide to pay the federal government’s payments by cash creation. What we’re doing here’s a short-term measure which will probably be reversed, in order that on the finish of this course of, the cash provide will probably be normalized, the Fed’s stability sheet will probably be normalized and there will probably be no everlasting improve, both in cash excellent or within the Fed’s stability sheet.”

When Wall Avenue mixes speculative manias with a long time of questionable central financial institution insurance policies, the result’s an funding panorama during which FOMO and a determined seek for yield can result in catastrophe. The FTX implosion is what one ought to anticipate following a multidecade financial dependancy to low cost credit score that now confronts rising rates of interest. An financial reckoning is inevitable however has been repeatedly delayed as a result of many issues and inefficiencies have been papered over by borrowing more cash to retire earlier obligations with newer and cheaper debt. This tactic works nicely when rates of interest are frequently falling. Now that corporations can now not rely upon entry to cheaper capital, working losses grow to be an issue. When borrowing prices go up, inefficient and fraudulent corporations can now not masks working losses. This turns into particularly problematic for extremely leveraged corporations which have huge debt-service prices.

Whereas many market members stay involved about rate of interest will increase, the true threat could also be lack of liquidity. The discount within the stability sheets of central banks, generally known as quantitative tightening, mixed with the refinancing of presidency deficits at larger rates of interest will drain liquidity from the capital markets. Just like the air we breathe, markets take liquidity with no consideration. After years of financial growth, coupled with the FOMO mentality, buyers have meaningfully elevated their threat profile. In durations of financial extra, Wall Avenue considers a number of growth and rising valuations as regular. As a result of central financial institution liquidity grew to become the norm, each time asset costs corrected over the previous twenty years, the most effective plan of action was to “purchase the dip”. Central banks saved increasing their stability sheets, including liquidity, and saving market members from nearly any dangerous funding choice.

Market members accustomed to financial growth with out inflation should now navigate a backdrop the place central banks will search to scale back their stability sheets by probably trillions of {dollars}. The consequences of this contraction are troublesome to forecast as a result of merchants for no less than two generations have solely skilled an expansionary surroundings. Diminishing liquidity is already impacting the riskiest sectors of the economic system, from excessive yield bonds to crypto property. Finally, when quantitative tightening really begins, the crunch will attain the supposedly safer property. Poor investing habits developed and strengthened over a long time will probably be onerous to interrupt.

As Jim Bianco of Bianco Analysis just lately postulated, “From 2010 to 2021, how did one get rich within the inventory market? Purchase SPY after which consistently complain that the Fed was not doing sufficient to make them wealthy.” That means, the bullish narrative to investing was to complain about how dangerous the economic system was doing to pressure the Federal Reserve to repeatedly decrease rates of interest and improve the dimensions of its stability sheet. Jim Bianco summarizes immediately’s funding dilemma: “The market is a liquidity junkie, it wants low cost cash greater than good earnings and progress. Everybody expects a recession, and due to that, everybody expects the Fed to pivot, they’re going to be chopping charges within the second half of the 12 months, everybody expects that will probably be falling inflation and can drive shares larger… transitory by no means actually went away.” If shares rally, then monetary circumstances ease, however the Federal Reserve can then stay hawkish and the “liquidity junkie” inventory market doesn’t get its repair of cheaper cash. Cartoonist Bob Mankoff captured this timeless catch-22 dilemma forty-one years in the past in The New Yorker journal.

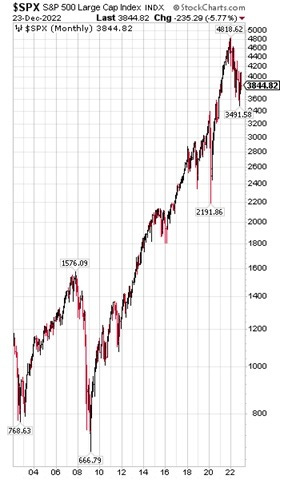

Hope springs everlasting and regardless of 2022’s bruising inventory selloff, the market has not but skilled a wholesale migration out of shares. On the contrary, buyers have bought a internet $86 billion value of home fairness mutual and exchange-traded funds within the ten months by October, in accordance with information from Morningstar. This inflow marks the second strongest annual influx going again to 2013, trailing solely the $156 billion fairness funds obtained final 12 months. Muscle reminiscence of excellent instances previous might clarify this resilient urge to buy-the-dip, because the S&P 500 has rallied practically 500% from its 2009 monetary disaster lows. As Jim Masturzo, chief funding officer of multi-asset methods at Analysis Associates, advised The Wall Avenue Journal, “For the final decade, the U.S. market was ripping yearly. Why would individuals make investments wherever else?”

As markets battle to simply accept the truth that the price for capital has elevated, buyers will probably be sluggish to simply accept the brand new funding paradigm. As a result of valuations have mattered little over the previous fourteen years, the present debate between inventory market bulls and bears hinges on one’s outlook for inflation, rates of interest and market liquidity. This battle is a part of the rationale markets all of a sudden hole larger after which bleed decrease – market members worry lacking the subsequent inventory transfer larger ought to the Federal Reserve “pivot” and decrease rates of interest. This habits was readily obvious throughout the sharp albeit very transient market drops in 2016, 2018 and 2020. Nevertheless, persistent inflation modifications the sport, and rates of interest at 5% will ultimately constrict the life out of untested enterprise fashions developed over the previous decade, depending on straightforward cash to finance profitless enterprises.

Constructed up over a decade plus of low or zero rates of interest and a easy purchase the dip technique that has left many with no creativeness for another funding aside from an index fund, there exists an unfailing optimism within the fairness markets. From the second the inventory market peaked in January, Wall Avenue pundits have downplayed the rising dangers throughout the markets. The day after the market peaked on January 4, 2022, a Bloomberg headline learn: “JPMorgan Strategists Say International Inventory Market Occasion Removed from Over.” Each step of the way in which down, month by month, headlines have bombarded buyers with new encouragement that the inventory market has reached its lows. Each single purchaser of Cathie Wooden’s ARK Innovation ETF, a one-stop store for hypothesis since August 27, 2017, is now within the crimson – a traditional instance of an asset bubble that went wild and subsequently imploded.

Fourteen years of central financial institution actions shifted threat investor appetites to such a level that fantastical narratives like ARKK managed to exist. Like all earlier bubbles, buyers now understand that they have been speculating moderately than investing and are actually going through the results. Understandably, all long-term buyers want a sure stage of optimism to attain their most elementary aim—to protect and develop the actual worth of their property. Inflation can at instances make this a excessive hurdle to clear, however the try have to be made as the choice of shunning long-term funding altogether is nearly actually the poorer selection. Historical past has by and enormous been type to the optimists and for these intrepid sufficient to embrace an fairness funding strategy, however one should even be sensible of their assumptions whereas sustaining the right temperament.

Walter Schloss was arguably one of many nice worth buyers of the final century. He pursued a deep-value technique all through his profession and even supplied to purchase Warren Buffett’s portfolio of shares when Buffett determined to exit the cash administration enterprise within the Sixties. In a 1996 speech, Schloss outlined the advantages of worth investing in comparison with another funding technique: “We’re discount hunters within the inventory market as an alternative of the retail commerce or comparable areas. As Ben Graham stated, we purchase shares like groceries not like fragrance, or as they are saying, ‘a inventory nicely purchased is half offered.’” Schloss’ main aim was to keep away from dropping cash, and the easiest way of doing that was to be contrarian: “After we purchase depressed shares, we appear to scale back our stress. Some individuals appear to thrive on stress, however we really feel in the long term it’s dangerous for them.” Schloss advised the story of Wall Avenue legend Peter Lynch, who earned billions for his buyers by investing in progress shares. His strategy, nonetheless, was terribly time-consuming and required the funding supervisor to run all around the nation discovering the most popular corporations. After ten years, Peter Lynch stop the enterprise. “I have been managing our fund for 40 years,” Schloss famous. “We aren’t stressed but, and we hope we by no means will probably be.”

Schloss understood {that a} worth funding philosophy matched his character. Following the despair within the Nineteen Thirties, Schloss needed to make sure that he might all the time become profitable and supply for his household. One of the simplest ways to do that was to restrict threat and shield the draw back: “Edwin [Walter Schloss’ son] and I search for methods to guard us on the draw back and, if we’re fortunate, one thing good might occur.” Schloss’ funding technique was not complicated; a significant cause why he was in a position to compound his funding capital at 15.3% per 12 months for nearly fifty years. To speculate efficiently, Schloss employed a technique that allowed him to make clever selections whereas maintaining his feelings in verify. He understood that how one’s funding portfolio carried out within the quick time period was a lot much less necessary than how one behaved over the long run. With this psychological framework, the investor can have the self-discipline and braveness to behave moderately than succumbing to the temper swings of different market members.

Nobody is aware of what lies forward within the capital markets for the approaching 12 months. Inflation, rates of interest, Federal Reserve coverage, earnings, recessions are all past the investor’s management. All that one can assume is markets will expertise a point of value volatility. Happily, value fluctuations solely have one important that means for the true investor—they supply the chance to purchase prudently when costs fall sharply and promote properly when a inventory value far exceeds one’s estimate of honest worth. As long run optimists, worth buyers ought to stand able to make the most of funding alternatives after they current themselves, or as Benjamin Graham stated, “The clever investor ought to acknowledge that market panics can create nice costs for good corporations and good costs for nice corporations.”

With type regards,

St. James Funding Firm

Authentic Put up

Editor’s Observe: The abstract bullets for this text have been chosen by Searching for Alpha editors.