Bet_Noire

I’ve lined a number of inflation-hedge ETFs these previous few months, together with these centered on commodity futures, miners, fairness inflation beneficiaries, and extra. These have usually carried out moderately effectively, attributable to skyrocketing inflation, however ought to underperform as inflation is introduced again beneath management. On the flipside, most of those ETFs have constructive long-term anticipated returns, so will be held long-term with none important subject. Accurately timing inflation can be finest, if troublesome, however holding long-term is ok too. At the least that’s the case for many of those funds. Commodity future ETFs, together with the Invesco DB Commodity Index Monitoring ETF (NYSEARCA:DBC), are an exception.

DBC’s long-term anticipated returns are near zero, plausibly even detrimental, because the fund’s holdings don’t generate any earnings, cash-flows, or earnings. Buyers will obtain roughly nothing from these funds if inflation normalizes, which appears exceedingly possible: inflation is slowing down, and the Fed is dedicated to combating inflation ‘till the job is finished‘. Inflation may at all times shock to the upside, however I’ve no motive to consider that this would be the case, nor do I see any attainable catalyst. Underneath these circumstances, I might not be investing in commodity futures ETFs typically, or in DBC specifically.

DBC – Fast Overview

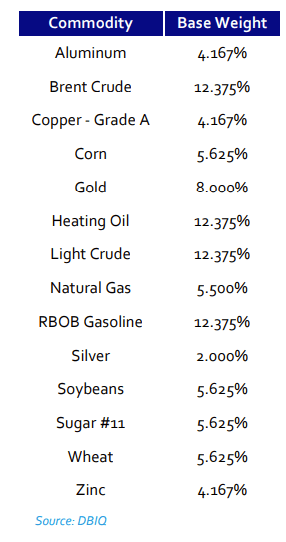

DBC is a diversified commodities index ETF, monitoring the DBIQ Optimum Yield Diversified Commodity Index Extra Return. Commodity weights are moderately well-diversified, fastened, and rebalanced yearly. Goal weights are as follows.

DBC

DBC’s precise present weights don’t considerably differ from the above.

DBC’s commodity publicity is gained by futures contracts. These are agreements to purchase or promote a specific commodity on a selected date for a selected value. Mentioned contracts are structured in such a manner that patrons, together with DBC, revenue from rising commodity costs, however undergo losses from reducing costs. Contracts are considerably pricey, however DBC take steps to attenuate mentioned prices.

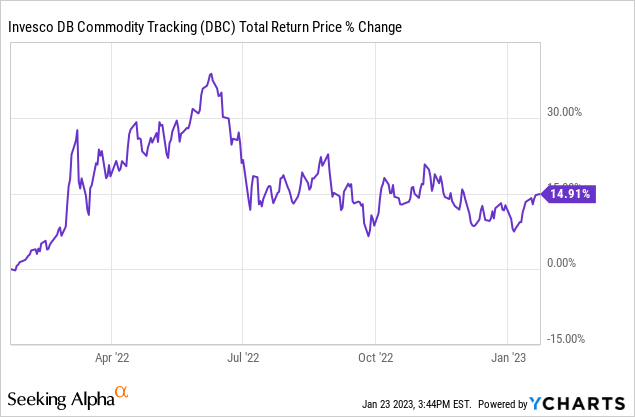

DBC ought to carry out effectively when commodity costs enhance which, virtually by definition, happens when inflation is excessive and rising. Inflation has risen these previous twelve months, throughout which DBC has carried out fairly effectively, as anticipated.

DBC is an easy diversified commodities ETF, performs fairly effectively when commodity costs enhance / inflation is excessive and rising, and is a improbable buying and selling automobile for commodity bulls. There are, nonetheless, many funds with broadly related traits, together with these centered on vitality equities, miners, and extra. DBC does have two necessary benefits relative to most of its friends. Let’s take a look at these.

DBC – Benefits

Pure Commodities Play

DBC’s commodity value publicity is direct, gained by futures contracts. Mentioned contracts are explicitly structured to ship earnings when commodity costs enhance, ignoring problems with valuation, investor sentiment, dividends, and many others. If oil costs enhance, oil futures costs enhance too, boosting DBC’s share value, with only a few exceptions.

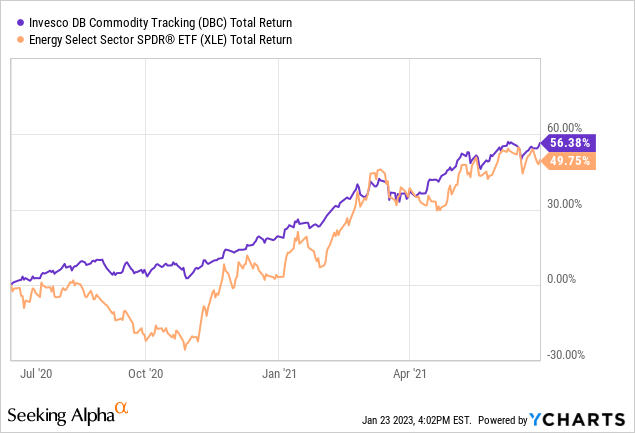

Most different funds concentrate on securities with oblique commodity value publicity. Vitality equities, as an illustration, ought to see larger share costs when oil costs enhance, boosting vitality fund share costs in flip. Importantly, vitality equities are not structured to make sure that that is the case: their precise efficiency relies on many components, together with fundamentals and investor sentiment. Vitality equities may simply underperform at the same time as oil costs enhance, for a myriad of causes.

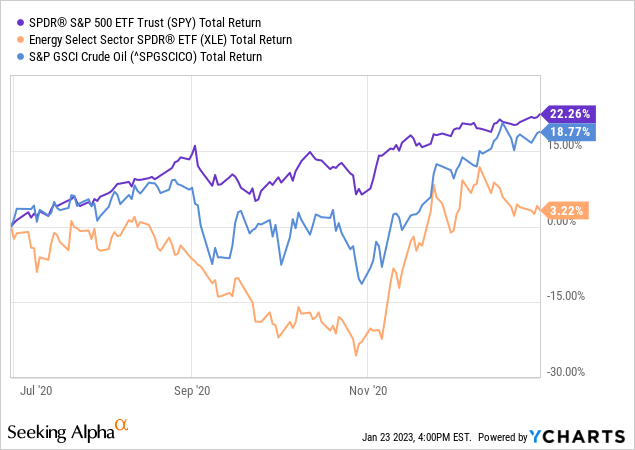

For instance, vitality indexes have been barely up throughout 2H2020, at the same time as oil costs skyrocketed. Vitality’s subpar efficiency was virtually definitely attributable to bearish investor sentiment: the coronavirus pandemic was nonetheless in full swing and vitality had carried out disastrously for over a decade on the time. Investor demand for vitality shares was extremely weak, sturdy costs and fundamentals however.

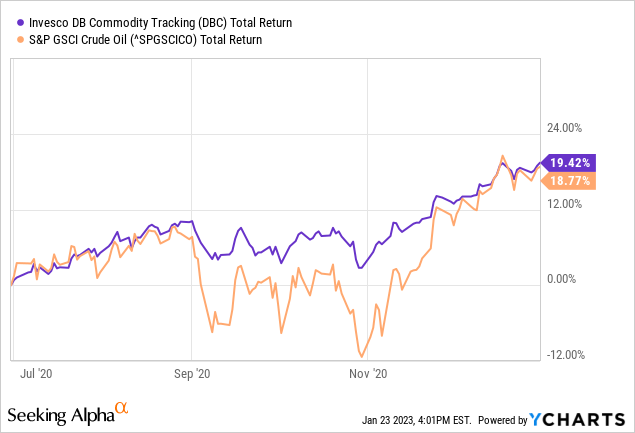

Importantly, DBC itself doesn’t undergo from these points. As talked about beforehand, the fund’s underlying holdings are structured to ship earnings when commodity costs enhance, no matter investor sentiment. DBC posted sturdy good points throughout 2H2020, as anticipated.

DBC’s direct commodity value publicity ameliorates the problems above, a constructive for the fund and its shareholders. Mentioned constructive is especially necessary for commodity value bulls, for apparent causes. Mentioned constructive can be significantly necessary within the short-term, throughout which investor sentiment reigns supreme, much less necessary long-term, throughout which fundamentals matter essentially the most. For instance, DBC outperformed vitality indexes throughout 2H2020, however the hole considerably narrowed within the subsequent six months, as investor sentiment improved. Investor sentiment may have remained bearish for longer, however fundamentals do matter, and have a tendency to take priority over sentiment as time goes on.

Brief-term, DBC considerably outperformed. Lengthy-term, not a lot.

Diversified Commodities Publicity

DBC supplies traders with diversified commodities publicity, with publicity to most related commodities. Diversification reduces danger, volatility, and potential losses or underperformance attributable to idiosyncrasies in anybody particular commodity.

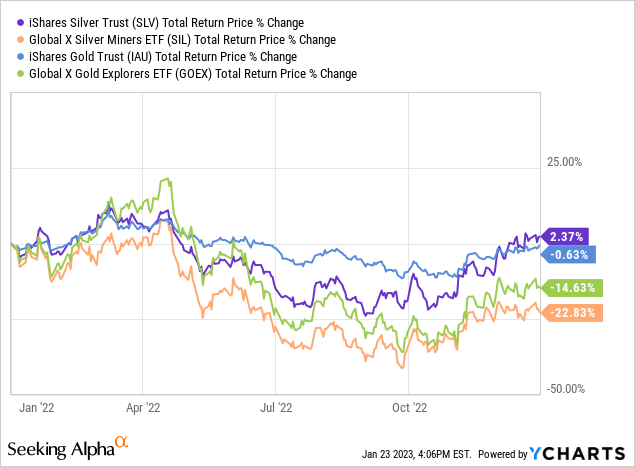

Single-commodity ETFs, then again, concentrate on one particular commodity, and so may underperform throughout a broad-based inflationary surroundings if their particular commodity does badly. For instance, silver and gold costs stagnated in 2022, at the same time as inflation and commodity costs typically skyrocketed. Silver and gold ETFs, fairness and commodity, each posted losses in the course of the 12 months, regardless that inflation has been fairly excessive.

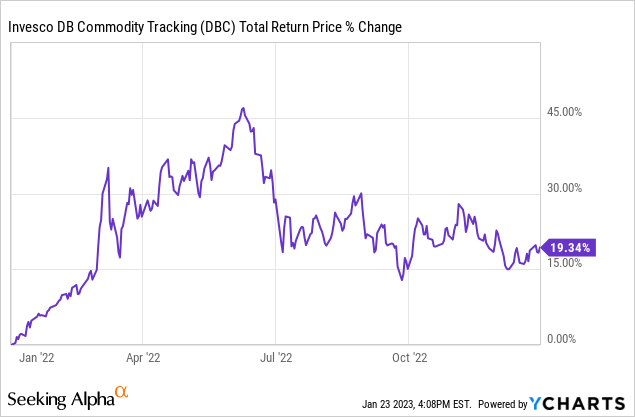

DBC, then again, is a diversified commodities ETF, and so does not likely undergo from mentioned points. So long as commodity costs are, typically, growing, fund returns ought to be constructive. Having a couple of laggards isn’t a problem, as different commodities can decide up the slack. For instance, DBC has posted very wholesome good points in 2022. Gold and silver detracted from the fund’s efficiency, however oil and vitality merchandise greater than made up for these losses.

DBC – Drawbacks

Low Lengthy-Time period Anticipated Returns

DBC’s most important disadvantage is the fund’s low long-term anticipated returns. Potential returns are low because the fund’s underlying holdings don’t generate / entitle traders to any earnings, cash-flows, or earnings, not like most different asset lessons and friends.

Equities pay dividends. Exxon (XOM) at the moment pays 3.2%, and dividends are inclined to develop.

Bonds pay curiosity. I Bonds pay 6.9%, and curiosity ought to rise if inflation will increase.

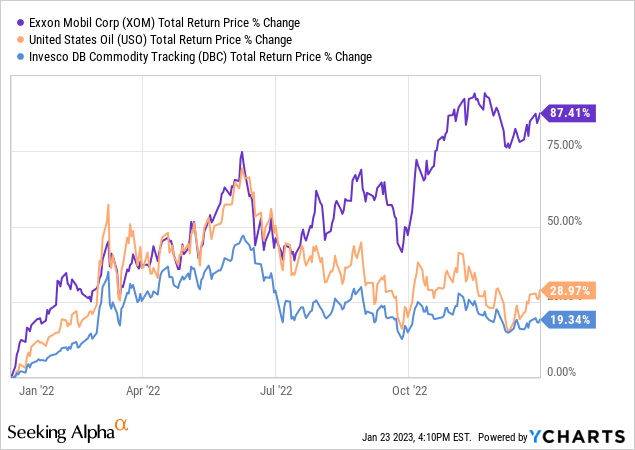

Oil futures pay nothing. Spend money on oil futures, get 0.0% in dividends or curiosity, pay 0.86% to DBC for the privilege.

Oil futures would enhance in value if oil costs enhance, however the identical is sort of definitely true for Exxon and I Bonds too. Exxon noticed skyrocketing returns in 2022, as anticipated.

I Bonds have seen excellent returns too, with yields skyrocketing to six.0% – 9.0% these previous few months (at the moment 6.9%).

DBC’s lack of earnings, cash-flows, or earnings, is the fund’s most important disadvantage, and one which is especially impactful long-term. Exxon’s dividends quantity to lower than 1.0% in 1 / 4, a rounding error. Brief-term merchants may choose DBC’s extra direct commodity value publicity over Exxon’s paltry quarterly dividends. Exxon’s dividends quantity to a extra respectable 3.3% in a 12 months. In a decade, the corporate’s dividends would quantity to greater than 33%, and that is earlier than contemplating dividend progress, dividend re-investment, and share buyback plans. These are extremely necessary, and helpful, for Exxon’s long-term traders, and virtually definitely outweigh DBC’s extra direct commodity value publicity.

On the similar time, DBC pays nothing in dividends, curiosity and the like, not like Exxon, different equities, bonds, and most different asset lessons. This makes it extraordinarily troublesome for DBC to outperform relative to its friends long-term, as has been the case since inception.

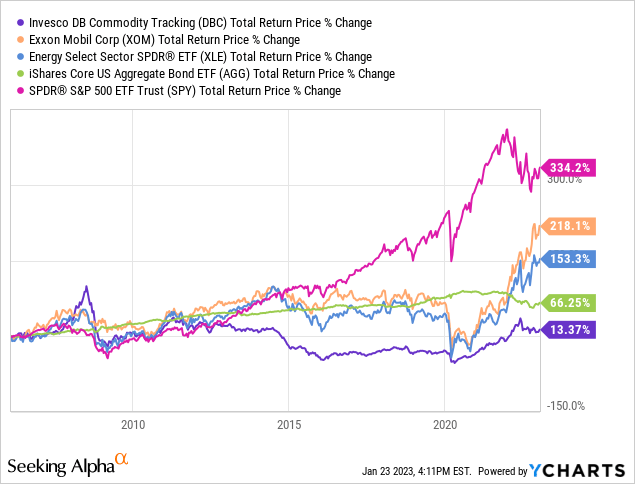

As will be seen above, DBC has posted whole cumulative returns of 13.2% since inception, greater than 20 years in the past. Most main asset lessons have seen a lot stronger returns throughout the identical, together with equities, treasuries, and vitality equities. Exxon is up too. DBC was unable to compete with these asset lessons, because of the fund’s lack of underlying earnings, cash-flows, and earnings.

For my part, and contemplating the above, DBC will virtually definitely be unable to compete long-term with these similar asset lessons shifting ahead. For my part, that is an extremely important detrimental, and greater than outweigh the fund’s different advantages.

Conclusion

DBC’s anticipated long-term returns are extraordinarily low, a major detrimental for the fund and its shareholders. As such, I might not be investing within the fund these days.