Editor’s observe: In search of Alpha is proud to welcome Gytis Zizys as a brand new contributor. It is simple to change into a In search of Alpha contributor and earn cash on your finest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click on right here to seek out out extra »

Meta Platforms gamble on the Metaverse jaanalisette/iStock Editorial through Getty Pictures

After going by way of the financials of Meta Platforms (NASDAQ:META), coupled with the present adverse sentiment and the Metaverse gamble by Mark Zuckerberg and his workforce, I imagine there’s a nice alternative on this identify for long-term traders. I’ve modeled the corporate’s financials and can undergo assumptions for the long run, forecast five- and 10-year DCF valuations, and can give my opinion on how the corporate would possibly carry out. On this article, I’ll give attention to how the corporate is making an attempt to diversify its income streams away from the tried-and-true advert income and construct up a stable stream of income from the Metaverse and the peripherals that include it. I may even focus on how administration feels about additional monetization of the enterprise messaging platforms Messenger and WhatsApp Enterprise. I may even examine potential dangers and catalysts that may change my funding thesis.

Income

The principle income stream for Meta Platforms has been promoting. From the latest 10-Q report, DAU, MAU, DAP, and MAP metrics have seen little or no progress YoY at a mean of three.5%. That is not stunning, contemplating that they’ve penetrated nearly half of the world. Nobody expects these numbers to develop considerably sooner or later, except China one way or the other permits all of the platforms to function throughout the nation, however I am not holding my breath.

What’s vital to traders is advert income. In the latest quarter, advert impressions on the household of apps (FoAs) have elevated by 17%. Nevertheless, the common value per advert has decreased by 18%, which triggered an enormous meltdown of the share value (down 60% within the final yr). The corporate expects this income to be affected significantly sooner or later as entrepreneurs are spending much less due to iOS privateness adjustments from the early spring of 2021. There are additionally different components, resembling laws within the U.S. and EU that impacts how they will course of private information.

And what’s Zuckerberg going to do about all of this? Nicely, the corporate is engaged on growing its promoting system additional and evolving it so that it’ll rely much less on private info. Which means extra of the information will likely be anonymized or aggregated third-party information to ship related advertisements and measurement capabilities. Nevertheless, these efforts shouldn’t have any tangible advantages as of now, as they are going to take years to implement.

It won’t be all doom and gloom for advert income simply but. An ally has just lately emerged that may assist soften the blow of iOS updates. That ally is Shopify (SHOP). Their new software, Audiences, is designed to determine and goal high-interest consumers with digital promoting. The platform aggregates all the buyer information and uploads it onto Meta’s advert platform to focus on prospects who purchased comparable merchandise. Time will inform how a lot of an influence this new software can have on advert income for Meta, however, in my view, there’s nice potential for synergy right here.

I additionally imagine that there will likely be an influence on advert income within the brief time period. Nevertheless, an organization like Meta, with the variety of assets they’ve accessible, will have the ability to reduce the influence to the place it won’t be vital anymore two or three years from now.

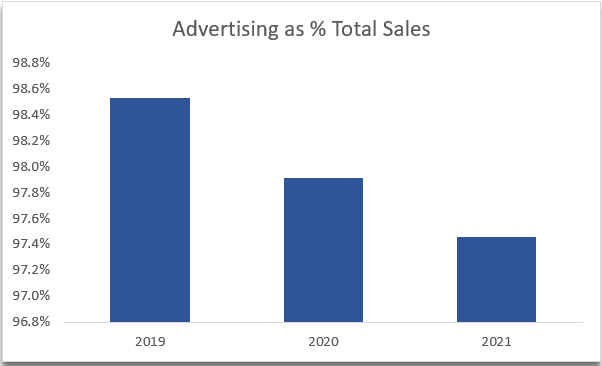

Virtually all of the income at Meta has been generated from advertisements, slowly trending down. (Personal calculations)

Metaverse Gamble

If the altering of their identify from Fb to Meta shouldn’t be an indication that the corporate is closely invested within the Metaverse going ahead, then I do not know what’s. Zuckerberg is a giant proponent of VR, and his lifelong dream was to construct one thing large on this area. With the height of the pandemic in 2020, the imaginative and prescient grew to become even clearer for Mark that digital workplace areas might be an enormous alternative.

To succeed in higher client penetration of the VR/AR area, workplaces have to be investing within the Metaverse to make any actual income from this megaproject. The push into the Metaverse has begun. Deloitte is one the larger gamers that helps corporations navigate the brand new world of the Metaverse and its capabilities sooner or later, even going so far as calling the Metaverse a trillion-dollar concept.

One other main firm to start out experimenting with the Metaverse is the actual property funding firm CBRE (CBRE). They’ve created their very own digital workplace for onboarding. CBRE is a large firm worldwide they usually imagine that digital workplaces will play a giant position in lowering carbon emissions.

Firms are slowly beginning to embrace what might be the way forward for work. If Meta needs to extend income within the workplace area, they might want to have a number of partnerships with as many corporations as they will get on board. I can solely speculate if corporations will likely be keen to embrace this concept.

There are fairly a number of uncertainties in regards to the Metaverse. It comes with a number of dangers. Once more, time will inform if this expertise will likely be a novelty or if it may possibly take off and change into a good income stream for the corporate. The way in which I see it’s that Zuckerberg shouldn’t be giving up on this anytime quickly. He’ll plow billions of {dollars} into the undertaking. It’s attainable to give you one thing extraordinary when you sink billions of {dollars} into one factor.

Expenditures

Actuality Labs, the phase that works on the Metaverse, accounted for 18% of complete OPEX. Of their newest 10-Q report, administration expects this phase to function at loss for the foreseeable future. To maintain supporting this megaproject they are going to want adequate earnings from the FoAs and different enterprise segments to generate money. Meta is on observe to lose $13B on Actuality Labs in 2022, and the corporate goes to commit 20% of its funds to the Metaverse in 2023.

This stage of expenditure on RL and R&D is smart as Zuckerberg and the administration workforce are ramping up innovation on this area. It might change into very promising within the subsequent few years.

Metaverse Choices

You can’t go into the VR world with out the accompanying equipment. Again in October, the corporate launched its flagship VR headset, Meta Quest Professional. The machine shouldn’t be very accessible on the present value of $1,500. It’s a large enchancment on their earlier headset and preliminary reactions to how a lot the headset has improved are nice. The display per eye is far greater high quality now, and it will solely enhance with time as Zuckerberg continues to take a position cash into it. Nevertheless, I don’t see many individuals adopting the headset at that value. As well as, it won’t be the appropriate time to get the headset as a result of there is no killer app accessible simply but. The present digital world of “Horizon Worlds” left lots to be desired, though with future updates like full facial recreation and a decrease entry value for the headset, I might see this taking off.

The Metaverse can change into large. Have a look at Roblox (RBLX) and what they’re doing on this area, or surgeons who’re utilizing AR to assist with surgical procedures, or the military shopping for AR expertise from Microsoft (MSFT). There will likely be many new methods of adopting AR/VR expertise in actual life sooner or later. It’s exhausting to place a worth on the Metaverse, however I do imagine that sometime this undertaking will likely be creating wealth for META as a substitute of burning the money generated by different segments within the firm.

In my view, the people who find themselves engaged on the Metaverse at Actuality Labs are doing an awesome job – simply take a look at this prototype the workforce has been engaged on for some time. The brand new avatars are photorealistic and are rendered in actual time. It’s gentle years forward of what the present avatars appear to be in “Horizon Worlds.” I can already inform that this expertise is revolutionary, and I’m very excited to see what is going to come out within the subsequent few years as Zuckerberg and the workforce preserve investing in R&D.

Monetization of WhatsApp and Messenger

Now that we have gotten that a part of the story out of the way in which, let’s give attention to one thing a bit extra tangible – e.g., the potential of WhatsApp and Messenger by way of income. Zuckerberg got here out just lately after main layoffs and stated that the following large pillars of their enterprise would be the enterprise messaging apps – WhatsApp Enterprise and Messenger – as they proceed their efforts by way of monetization.

WhatsApp for Enterprise

This app is freed from cost for corporations and customers if the corporate solutions the question inside 24 hours. If not, they are going to be charged $0.0085 per message for the primary 250,000 and happening to $0.0058 per message above 10 million messages – which means the extra the corporate responds, the cheaper it will get. The newest statistics I discovered for a way a lot income this app is producing is just below $300m in 2021, which is a really small fraction of the entire income. I might see this ramping up much more because the firm will likely be specializing in these platforms. This initiative exhibits me that administration isn’t just specializing in the Metaverse play, however moderately maximizing revenues in all the segments of the corporate.

WhatsApp Pay

This app is a more moderen service that’s solely accessible in Brazil and India thus far, and works similar to PayPal (PYPL). You’ll be able to ship cash to mates, household, or a enterprise, and the receiver is charged round 4% of the cash. There aren’t many particulars on how a lot income Pay is producing as a result of it is nonetheless within the testing section. Nevertheless, these areas will likely be a superb gauge of how the app will do contemplating they’re the most important areas the place WhatsApp is used worldwide.

As soon as the corporate works out all of the kinks in these areas and opens the service up worldwide, we’ll lastly see correct monetization of the platforms and additional diversification from advert income.

Partnership-Pushed Success

The current partnership of WhatsApp and Salesforce (CRM) is an efficient instance of additional monetize these two messaging platforms. The combination creates instruments so that companies can contact prospects immediately by way of the messaging apps, run advert campaigns, and promote straight by way of the chat. One other main partnership was with Jio and WhatsApp in India. It’s the first end-to-end purchasing expertise, which permits prospects to browse items by way of WhatsApp for supply by merely sending a message.

Enterprise messaging apps are presently within the early levels of monetization. Nevertheless, partnerships with main corporations and world availability have the potential to drive vital income progress by way of focused promoting and commerce alternatives on apps like Messenger and WhatsApp.

Financials

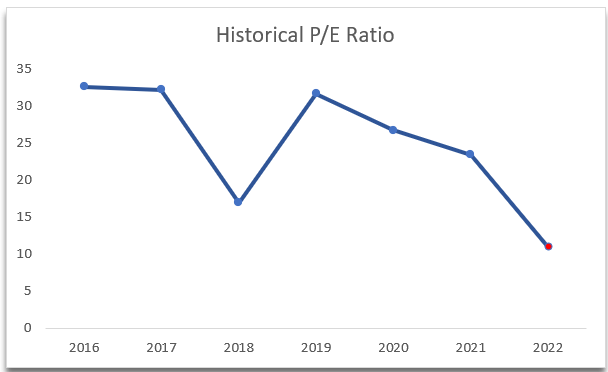

Earlier than we delve deeper into the corporate’s financials, we will see that the pummeling the share value took during the last yr might current an awesome shopping for alternative. First, the P/E ratio of Meta has by no means been decrease, sitting at 11x on the time this text was written. This alone would possibly entice some individuals’s consideration to it. The very first time I invested within the inventory was round 2018 when the P/E ratio was at round 27, and even then I believed it was a superb funding.

Historic P/E Ratio (Personal Calculations)

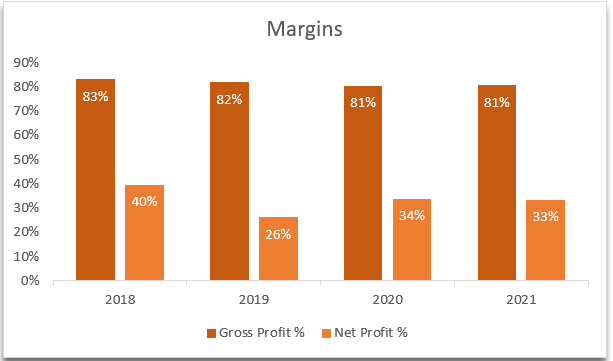

Trying on the financials of the corporate during the last 5 years I can see that the corporate is doing effectively. Gross and internet revenue margins have been regular and in actually good condition. These figures could be impacted a bit extra as soon as we see full-year 2022 accounted for within the subsequent 10-Okay report, due in February. I’d count on internet margins to go all the way down to round 20%, however it’s nonetheless a wholesome firm that is aware of handle its accessible assets very effectively.

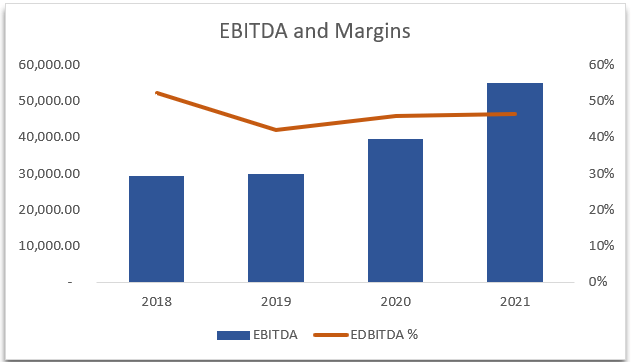

Gross and Web revenue Margins from 2018-2021 (Personal calculations) EBITDA numbers and EBITDA Margin from 2018- 2021 (Personal calculations)

EBITDA and EBITDA margins have been glorious all through the years and comparatively secure. I do count on EBITDA to go down barely on the finish of 2022 to across the 35%-40% vary, as the corporate has spent much more cash on R&D, and additional influence advert revenues. However that is solely within the brief time period; I am extra centered on an extended timeframe.

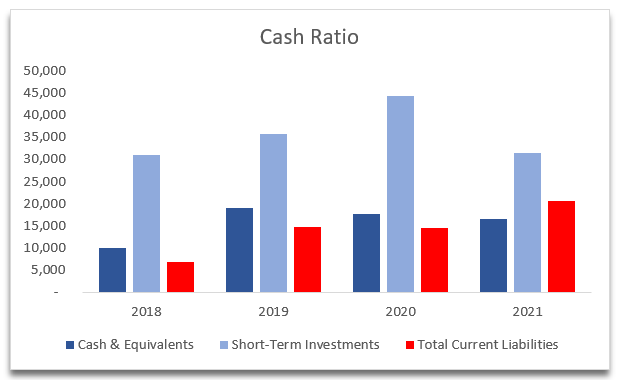

Money Ratio Chart of Money & Equivalents to Complete Present Liabilities 2018-2021 (Personal calculations)

Meta Platforms has been a money machine for the longest time, and has sufficient money and equivalents to cowl all its short-term obligations and even its complete liabilities. I like investing in corporations which have little or no or no debt in any respect. Meta has little or no debt, round $9 billion, which is well lined by money and marketable securities as proven above. The corporate is basically unleveraged and that could be a excellent place to be in, in my view.

DCF Valuation

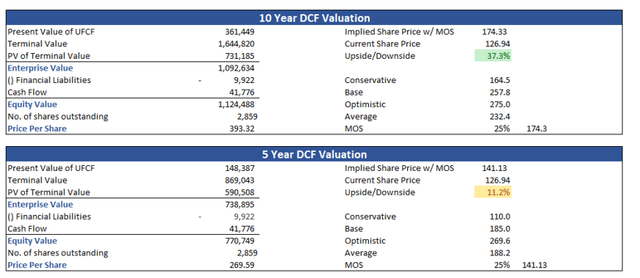

I created a DCF mannequin for the corporate, making an allowance for present financials and future developments, and generated three situations to guage the corporate’s attractiveness. Case one is conservative, case two is base, and case three is optimistic.

Various assumptions have been applied within the mannequin, offering additional element on advert revenues, RL revenues, and R&D prices. For the conservative case, I took out all the RL income however left its prices to make it look as if the corporate is basically burning money with no profit. That is as a result of I needed to see if that will have an effect on the valuation by lots. It didn’t, as a result of many of the income is coming from advertisements. I’ve modeled each revenue assertion merchandise; nevertheless, I solely talked about those that will take advantage of influence on the valuation.

I calculated the WACC to be 8.86% on the time of modeling (late December 2022) and I selected a terminal progress charge of two.5%. Making use of a margin of security of 25% to all situations and taking a mean, my mannequin means that Meta, underneath a 10-year DCF valuation, has an upside of 37.3% and 11.2% underneath the five-year DCF valuation (as proven beneath).

10- and 5-year DCF valuations of Meta Platforms with MoS of 25% (Personal calculations)

Future Dangers

There are a selection of dangers to think about right here. The Metaverse won’t work out. The corporate won’t have sufficient expertise in client {hardware} and VR/AR expertise, which could lead on different corporations to compete extra successfully than META. R&D expenditure might be for nothing if they’re unable to make key partnerships and develop belief within the Metaverse.

Continued strain from regulators within the U.S. and EU would possibly hinder the expansion and success of Meta. The EU just lately opened a brand new case towards them for breaching antitrust guidelines concerning their built-in market on Fb, through which they are saying different market corporations aren’t capable of compete with the benefit that Fb has amassed over time. That is an $11B lawsuit. However I don’t imagine it should get far in any respect, as to me it is senseless that Meta is being primarily penalized for having a superb product just like the Market built-in into their social media platform.

Strain from TikTok will take away display time from the household of apps, after all, however the good storm for Meta in 2023 could be the persevering with chaos of Twitter (TWTR) and Elon Musk within the social media area, and tighter rules of TikTok that might profit Meta significantly.

The one factor that will change my bullish thesis on the corporate is that if Meta weren’t capable of regulate their algorithms and machine studying to fight the iOS privateness adjustments, and we begin to see advert income getting hammered. If revenues are hit exhausting by the adjustments, as an instance 10%-20%, that’s primarily 10%-20% of all the income. That might lead to a big loss for the corporate, and it would battle to take care of its present operations and progress. It could be vital for the corporate to discover different income streams or diversify its income sources in an effort to mitigate the influence of such a loss.

Macroeconomic components are a giant threat for all tech corporations, not simply Meta. The latest Fed assembly noticed Fed Chair Jerome Powell point out that he’ll do every part in his energy to decrease inflation to the two% mark, so we’ll proceed to see rates of interest going up for the following whereas. The terminal charge now stands at round 5.25% for 2023.

The above-mentioned dangers might drive revenues down if all of them come true. If Meta shouldn’t be capable of overcome these obstacles, that might carry much more negativity to the corporate and depress its share value additional.

Catalyst

The share value has been on a downward trajectory since its excessive in September 2021. It’s making an attempt to interrupt out from this development because it hit a low of $88 in November of final yr. What might change this year-long downward trajectory could be an excellent end-of-year earnings report. This could shift the adverse sentiment surrounding the corporate. If we see good progress in consumer numbers and advertisers begin to pay extra for the advertisements, this might probably put the inventory into rally mode.

Then again, if consumer progress has plateaued and advert costs proceed to fall – coupled with the will increase in rates of interest – the downward development of the inventory value will proceed, and can most certainly take a look at the lows once more.

Conclusion

In my view, Meta is in nice form total financially, regardless of the Metaverse gamble hanging over the corporate’s head for the following few years and advert income uncertainty. The financials are excellent, and I imagine that traders have oversold the inventory. The corporate now appears very engaging for long-term traders.

I’m excited in regards to the potentialities of the Metaverse. The worst that may occur is it fails, and the corporate can have $10 billion yearly again on its steadiness sheet after it stops funneling all that cash into RL. Or they may pivot the entire idea towards gaming as a substitute of utterly dropping it, since what they do have on their palms is promising. I’m bullish total on the corporate, however I’d wait a short while longer to see what occurs with the following couple of earnings experiences and the way this macroeconomic surroundings goes to vary over the following few months.