Vertigo3d

Manole Capital Administration

4th Quarter Publication

December 2022

Manole Capital’s 4th Quarter Publication:

We’re utilizing our 4th quarter publication as a means of summing up a difficult 2022 and (extra importantly) wanting ahead to 2023. We’ll present some tidbits on the macro surroundings (i.e., rates of interest, inflation, Fed commentary, and many others.), and we’ll try and weave in some insights into our distinctive funding course of and philosophy.

Introduction:

As we all the time say, for those who’re searching for political ideas, you might be completely within the fallacious place. We by no means touch upon politics and depart that to others. Our feedback are solely targeted on the markets, particularly our model of FINTECH. We outline FINTECH reasonably uniquely, as “something using expertise to enhance a longtime course of.” If in case you have any free time or for those who’re having a tough time sleeping, you possibly can higher perceive our model of FINTECH by studying our proprietary analysis. Simply search on Looking for Alpha for our prior newsletters, inventory particular pitches, thematic notes, or Gen-Z surveys.

We all know that volatility is the short-term value that fairness buyers should pay for long-term enticing returns. All buyers finally really feel the nervousness and ache of a unstable market. Nonetheless, we select to plan for and mannequin in this kind of volatility, so we aren’t stunned when it will definitely arrives. We now have stayed true to our bottoms up, research-intensive course of and proceed to spend all of our time doing FINTECH and company-specific evaluation.

2022:

This 12 months and final 12 months seem to be polar opposites. In 2021, the S&P 500 rose +29% and all people was having success choosing shares. This 12 months, the S&P 500 is down roughly (20%) and discovering winners is far more difficult.

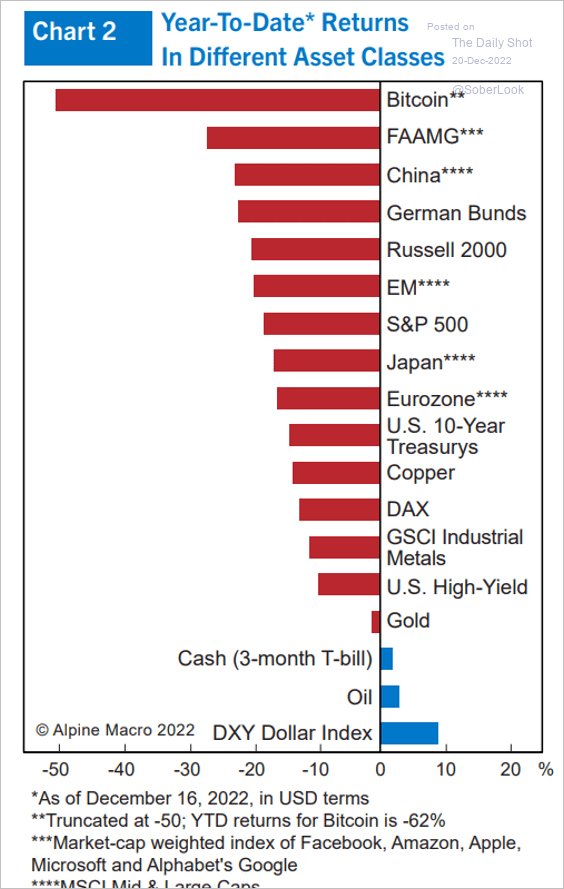

In a 12 months like 2022, when the whole lot from crypto to equities to fastened revenue is down, it was exhausting to discover a “place to cover.” As you possibly can see on this chart, aside from good ol’ money and vitality, just about each asset class and geography went down this 12 months.

The Every day Shot (The Every day Shot)

Warren Buffett as soon as mentioned “Rule #1 isn’t lose cash. Rule #2 is always remember rule #1.” Whereas we try to all the time make cash, the unlucky fact is we typically get a inventory fallacious – shocker! We’d share a primary identify with Mr. Buffett, however we completely aren’t excellent. For us, we outline success as “producing glorious long-term returns and limiting a fabric lack of capital.”

Within the 1960’s, progress shares had a large rally, with the High 50 firms changing into the “Nifty 50”. These “positive issues” led buyers to pay extraordinary valuations (50x ahead earnings). By the top of that decade, Mr. Buffett had turn into so pissed off on the exuberance of the market that he dissolved his investing fund and easily moved to the sidelines. We weren’t that pissed off with fairness markets final 12 months, however we respect his precept.

By 1973, with an oil embargo and runaway inflation, Mr. Buffet re-emerged and commenced to place his money to work. He was quoted in Forbes saying he felt “like an oversexed man in a harem.” Whereas we aren’t about to say the 2023 is that attractive, we proceed to selectively put extra capital to work.

Santa Claus Rally:

Since 1950, the 4th quarter has generated the perfect common quarterly returns for the S&P 500 of +4.1%. In a traditional 12 months, shares usually head greater in mid-to-late December, in what is usually known as a Santa Claus Rally. During the last 70 plus years, from December twenty third by means of the final 5 buying and selling days of the 12 months, the S&P 500 averages achieve of +1.4%. Not this 12 months!

After some preliminary pleasure over the smaller rate of interest tempo (simply 50 foundation factors, as a substitute of 75 foundation factors), it did not take very lengthy for the markets to appreciate that the Fed expects to proceed to hike and go longer than most count on. As Chairman Powell said, “Whereas smaller fee hikes are a promising improvement and a welcome signal that tightening insurance policies are serving to, it doesn’t imply that we’ve got restored value stability or that inflation has been tamed. He then emphasised that “It is going to take considerably extra proof to offer consolation that inflation is definitely declining” and “by any customary, inflation stays a lot too excessive.” Then, the Fed downwardly revised its GDP progress estimate for subsequent 12 months to solely 0.5% (from +1.2%) and upped its estimate for unemployment to 4.6% subsequent 12 months (at the moment at 3.7%).

Fed policymakers now have a median federal funds goal projection 5.1% subsequent 12 months, a stage not seen since 2007. To hit that concentrate on subsequent 12 months, the Fed will doubtless increase charges by 25 foundation factors in February, March, and Might. That is what the CME FedTool is at the moment indicating. With public feedback like these, one may suppose Chairman Powell is making an attempt to be the Grinch that stole Santa’s rally.

Our 2022 Efficiency:

We aren’t in a position to assemble a catastrophe proof portfolio, however we will handle our web publicity and lean into positions that current the perfect upside. I suppose you possibly can say we’re patiently ready for our alternatives to seem. As Bruce Lee as soon as mentioned, “Endurance just isn’t passive, quite the opposite, it’s concentrated power.”

We attempt to phase our efficiency into 3 numerous camps. The primary is our long-only portfolios (publicly-traded FINTECH securities), the second is our lengthy and brief portfolios (additionally publicly traded FINTECH firms) and the final is our hedge fund – the Manole Fintech Fund (i.e., The Fund). The Fund is the one car that may personal each publicly traded, in addition to privately held FINTECH firms.

In our long-only portfolios, which will be considered right here, we proceed to personal a concentrated mixture of FINTECH securities. When the market declines and monetary danger is heightened, we can not hedge this portfolio with our brief guide. We select to extend our money, as a type of draw back safety. In an inflationary surroundings, this may be an costly proposition, however it’s not our long-term intention to run the portfolio with money ranges this elevated. It’s merely a short lived resolution to a difficult surroundings. After 13 consecutive years of optimistic efficiency, the Nasdaq 100 simply had its worse 12 months since 2014. With so many expertise names in our concentrated portfolio, we weren’t immune.

Our“Low Internet” lengthy / brief FINTECH portfolio makes an attempt to maintain our web publicity low (within the + or – 500 foundation level stage). When the market is steadily transferring greater (like 2021), the lengthy names carry out, however the shorts detract from total efficiency. When the market stumbles (like 2022), we wish to see our lengthy names “maintain their very own”, whereas the shorts materially add to efficiency. That is precisely what occurred this 12 months and the portfolio ought to finish the 12 months up within the +7% vary.

Since its inception, The Fund has generated stable efficiency from its personal investments, however that modified in 2022. In the summertime, Klarna raised cash and it equated to a down spherical of over (85%). We’re removed from excellent, and this is only one instance of the hazards of investing in personal firms (much less transparency and restricted liquidity). In The Fund, we anticipate 2022 efficiency being barely optimistic. This 12 months, the brief guide materially assisted total efficiency, which primarily is the other story from 2021. Whereas that is the worst absolute annual lead to its 4 years of existence, one may argue it’s the greatest relative return too (in comparison with a market down roughly 20%).

Horny and modern shares have been in vogue in 2021, because the market climbed greater and better. A few of our “boring” and free money circulate firms have been higher performers this 12 months. As we glance to 2023, we’re excited that the majority of our secularly rising FINTECH firms will generated significant annual EPS progress. The general market EPS outlook will likely be fortunate to be flat subsequent 12 months, however our free money flowing FINTECH firms ought to have the ability to produce high-single-digits earnings progress.

2023:

Final 12 months, the S&P 500 topped out at a ahead P/E of over 21x. At the moment, taking a look at 2023 (which continues to be too excessive) earnings, the market’s P/E is roughly 17x to 18x. If we return to the late 1970’s, the P/E was within the single-digit vary. We aren’t saying valuations are “grime low-cost”, however we’re discovering attention-grabbing “bargains” in a few of our favourite names.

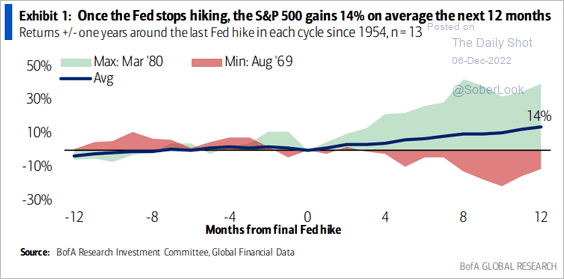

If we have been to summarize the consensus outlook for 2023, we might say that the majority market pundits are predicting 6 months of continued powerful circumstances, adopted by 6 months of a optimistic rebound in sentiment. This forecast corresponds with continued rate of interest will increase on the subsequent 3 Fed conferences, adopted by a pivot and loosening of circumstances. We perceive why the market is hoping for this pivot, because the S&P 500 sometimes performs properly as soon as the Fed stops elevating charges. As this Financial institution of America Analysis chart reveals, the S&P 500 delivers a mean of +14%, over the next 12-months as soon as the Fed is completed tightening.

Financial institution of America Analysis (Financial institution of America Analysis)

Whereas the velocity at which the Fed has raised charges is critical, we’re extra eager about how lengthy the Fed decides to carry charges at these ranges. The slower the Fed acts, the possibilities that it overdoes this tightening and causes a serious slowdown theoretically will get lowered. Possibly it comes all the way down to how a pivot is perceived. In our opinion, a discount within the tempo of fee hikes just isn’t a pivot. We proceed to suppose that the Fed’s quantitative tightening program will proceed, particularly since little has been achieved with its huge $8.6 trillion steadiness sheet. Because the Fed continues to tighten (right into a deeply inverted treasury yield curve), we imagine it’s best to stay conservative and count on elevated volatility.

At the moment’s market appears solely targeted on macro commentary emanating from the Fed. We perceive this however aren’t going to alter our course of as a result of the market is fixated on Chairman Powell’s feedback. Fairly merely, we do not imagine that issues will miraculously get higher as soon as the Fed stops elevating rates of interest and pauses. We’re modeling in a continued sluggish surroundings, the place firms with money circulate and dominant franchises will carry out, whereas much less capitalized (i.e., weaker) opponents fail. If the Fed have been to reverse course and out of the blue get accommodative, it could doubtless imply the economic system has carried out remarkably nicely. If that is the case, our market main firms ought to submit glorious returns and outcomes.

Inflation, Curiosity Charges, and the Fed:

The Fed continues to focus on 2% inflation, which it struggled to realize for a few many years. Lastly, inflation rises to 7% to eight% and the worldwide economic system goes haywire. Why ought to we count on that the Fed will shortly reverse course and minimize rates of interest? As Chairman Powell said, “it’s doubtless that restoring value stability would require holding coverage at a restrictive stage for a while. Historical past cautions strongly in opposition to prematurely loosening coverage.”

We’re happy that inflation has fallen from +8.6% in September all the way down to +7.1% in November, however we stay very removed from that Fed 2% goal. We would not name 10 to twenty bps of a decline (versus Road expectations) equal to a deflationary surroundings. In our opinion, inflation working within the high-single-digits is not worthy of a celebration.

Do not get us fallacious. Decrease inflation readings are a web optimistic, however the absolute stage is sadly nonetheless troublesome. We hate to make a sophisticated topic so easy, however inflation working over 7% continues to be a Fed drawback.

Fed Governor Christopher Waller latest feedback resonated with us, when he mentioned “we’re not softening…stop taking note of the tempo and begin taking note of the place the endpoint goes to be. Till we get inflation down, that endpoint continues to be a methods on the market.” Governor Waller believes the Fed is “on the proper path” as a result of all the fee will increase this 12 months have completed little to interrupt inflation. He mentioned, “For all of the discuss of crashing the economic system and breaking the monetary markets…it hasn’t completed that.”

Does this sound like anyone that can shortly pivot and alter course in 2023 (and minimize charges)? Decrease rates of interest would clearly assist hyper progress firms that are not terribly sustainable on this greater fee surroundings, however we simply do not imagine that forecast is possible. We’ll proceed to imagine inflationary pressures in our proprietary fashions, and if that finally disappears, we’ll be pleasantly stunned to the upside.

Investing Kinds:

Understanding a supervisor’s course of, technique and philosophy can typically be a problem for buyers to understand. Our investing type was developed underneath the umbrella of Herb Ehlers and Goldman Sachs Asset Administration’s Development Fairness group. Most of the important investing themes we focus on, have been discovered from years of expertise on that profitable group.

There are macro or top-down managers, that make choices primarily based on financial fundamentals. There are quantitative managers, utilizing algorithms, machine studying and typically synthetic intelligence to make buying and selling choices. There are arbitrage outlets that search for alternatives with M&A disparities and technical managers making intra-day buying and selling calls. Frankly, there are dozens and dozens of various kinds of asset managers.

As our loyal readers know, we do not make grand proclamations or forecasts on macro subjects, as that is not our space of experience. We’re not going to guess the what number of foundation factors the Fed will improve at their subsequent assembly in February. We aren’t going to supply an inflation goal, a market guestimate for foreign currency echange or make any daring commodity predictions. As a substitute of guessing the place costs will go, we choose to personal the exchanges the place all of those merchandise commerce. We might reasonably personal a transaction processor benefitting from greater volatility, versus speculating on the following leg up or leg down in numerous commodities.

As a substitute of macro forecasting, we are going to proceed to focus solely on doing bottoms up, elementary analysis. We like to do situation evaluation to know how our firms will carry out in numerous environments and financial circumstances. Possibly we want a passion?

Totally different Strokes for Totally different Of us:

Let’s begin our dialogue on funding types with a Resort.com’s Captain Apparent kind of assertion. Whereas Tampa has completed a incredible job increase its downtown, it is not mid-town Manhattan. In New York Metropolis, one may see a dozen hedge funds all positioned in a single workplace constructing. That is not Tampa, as our metropolis is far more of a health care provider / lawyer kind of city.

Over a 12 months in the past, Cathie Wooden relocated her Ark Funding Administration agency from New York Metropolis to St. Petersburg, FL. We have been thrilled to have extra monetary professionals and cash managers in our “neck of the woods”. With over $14 billion in belongings underneath administration, Ark’s ETFs stay fairly standard.

Ms. Wooden has turn into one thing of an “funding rock star” along with her skill to articulate and clarify monetary ideas to retail buyers. Ms. Wooden is an amazing speaker and eloquently goes from macro commentary to deeper, inventory particular points. Again in August 2021, the New York Instances profiled Ms. Wooden and her “uncommon method to investing.” We now have seen her on CNBC and Bloomberg TV, and he or she all the time appears to splendidly focus on the markets and Ark’s funding type.

A month in the past, we went to one in every of Ms. Wooden’s discussions, to listen to how she invests. We weren’t making an attempt to get any new inventory particular concepts, however we wished to know her course of and investing philosophy. There was standing room solely in Ms. Wooden’s presentation and the attendees have been gripped to her feedback. We appeared on the viewers and puzzled…if we have been to offer a market replace to potential purchasers, we might be fortunate to get our dad and mom to indicate up (and possibly provided that there have been handed appetizers and an open bar).

Getting again to Ms. Wooden and the presentation we heard a month in the past. As soon as once more, we’re a fan of hers and are impressed along with her skill to articulate her funding philosophy and elegance. The place we differ is on Ark’s technique of deploying capital and perhaps on portfolio development too. Additionally, we are likely to disagree with a few of her latest market feedback; listed below are just a few of the quotes we jotted down that made us “scratch our head.”

“Disruptive Innovation”:

Ms. Wooden typically mentions “disruptive innovation” when she discusses her portfolios. She defines it as ” the introduction of a technologically enabled new services or products that probably adjustments the best way the world works.”

Ms. Wooden invests with a mindset that“sacrifices short-term earnings to capitalize on the exponential progress and extremely worthwhile alternatives that a variety of innovation platforms are creating.” On this, we completely agree and we additionally search for firms with open-ended and enticing secular progress alternatives.

We are able to respect this longer-term perspective, however not all market circumstances permit a supervisor the latitude to sacrifice right now’s ache for tomorrow’s good points. We aren’t searching for our firms to change their capital allocation plans for the near-term, however we predict glorious administration groups can use free money circulate for re-investing again of their enterprise, plus present regular dividends and probably even inventory buybacks. Simply because an organization generates additional cash circulate that it must develop doesn’t imply it is not modern.

At her Ark presentation, Ms. Wooden spent a little bit of time discussing how she considered the long run, particularly discussing air and robo-taxis. She claims that this trade has a ahead addressable market alternative of $10 trillion. Whereas that may really occur, we are typically far more grounded in right now and tomorrow kind of points. We aren’t short-term targeted, however we are likely to choose to mannequin how our companies will do in 2023 and 2024, reasonably than 2035.

Considered one of our favourite cartoon reveals (rising up) was The Jetson’s and we beloved how forward-thinking it appeared. The present got here out in 1962 and the futuristic household cartoon predicted what life can be like in 2062. The writers for The Jetsons have been means forward of their time, accurately predicting flat display TV’s, sensible watches, drones, video calls, digital newspapers, holograms, and even robotic vacuums.

Whereas we mannequin what occurs to our cost firms as you employ extra playing cards (and fewer money), Ms. Wooden appears to mannequin which firms will succeed with the arrival of flying taxi’s. I suppose we aren’t visionaries or perhaps we aren’t that good at making lengthy, lengthy, long-term forecasts.

Deflation or Inflation:

Ms. Wooden expressed a “higher danger of deflation, than inflation” after which defined how former Treasury Secretary Larry Summers is “very fallacious” together with his inflationary worries. Ms. Wooden believes that inflation is non permanent and that “it’s a 15-month drawback, not a 15-year drawback”, whereas Summers argues that the Fed will proceed to boost rates of interest (probably to five.5% to six.0%), so long as inflation is working at a close to 40-year excessive. As a substitute of discussing this deflationary menace intimately, we’ve got hooked up Ms. Wooden’s open letter to the Fed right here. If we have been to select sides on this inflationary debate, we might in all probability lean in the direction of Mr. Summers, reasonably than deflation changing into an issue subsequent 12 months.

What did the unbiased Fed should say about this actual matter? Effectively, Chairman Powell mentioned, “We should be trustworthy with ourselves that there is inflation. 12-month core inflation is 6% CPI. That is thrice our 2% goal. Now it is good to see progress, however let’s simply perceive we’ve got an extended methods to go to get again to cost stability.” As a substitute of hoping the Fed pivots and begins to chop rates of interest, which many expect in mid-2023, we envision inflation remaining stubbornly excessive. How lengthy? We do not know, however we aren’t within the camp that the Fed will start to decrease rates of interest in the course of subsequent 12 months.

Diving deeper into this matter, we will respect why Ms. Wooden desires a decrease rate of interest surroundings. In case your portfolio is stuffed with hyper progress firms, with damaging working leverage and money circulate issues, you want the Fed to cease elevating rates of interest. You hope and pray for one more bull market and an surroundings that rewards innovation and progress, on the expense of earnings.

Ms. Wooden mentioned she is investing like we’re “going to see an surroundings just like the ‘Roaring 20’s’.” These kind of circumstances are potential, but it surely is not what we’re anticipating. One other distinction in our cash administration type comes all the way down to what occurs to an organization’s fundamentals – if the “climate will get tough” and financial circumstances worsen (like 2022). All of our firms generate free money circulate and may “climate the storm”, whereas sure Ark Funding positions seem like constructed for “calmer seas.”

Portfolio Development:

Ms. Wooden closed her presentation along with her ideas concerning the upside of her portfolio. She mentioned, “our firms are going to go up 100x, and Microsoft will not”. We agree that Microsoft, with its $1.8 trillion market capitalization, has completely no likelihood to go up 10x, not to mention 100x. We do not personal Microsoft, so we aren’t taking offense to that remark. For us, it led to a query about portfolio development.

Our funding course of strives to steadiness danger and reward. We’re pleased with a few of our positions producing 10% to twenty% good points. Utilizing a baseball analogy: Not each identify must be a “residence run”. We’re happy with a few of our firms delivering “singles or doubles” or just “bunting to achieve 1st base.” Our portfolios try and marry some names which have greater danger / greater reward, with these which are steadier and have extra predictable returns. We do not have a ton of holdings which are going to finish up being value 100x their present valuation, however we additionally haven’t got positions that may find yourself nugatory (knock on wooden).

Not one of the prior few pages are supposed to be disparaging in the direction of Ms. Wooden or Ark’s funding philosophy. She needs to be applauded for constructing Ark into a big, well-known, and worthwhile asset supervisor (considerably bigger than Manole Capital). All we try to do is differentiate between funding types, and to supply extra perception into our distinctive technique and philosophy.

We discover it attention-grabbing that Ark’s FINTECH ETF owns 30 totally different firms and but there are solely 4 names that overlap with our flagship FINTECH portfolio. Clearly, we’ve got a really totally different definition and model of FINTECH.

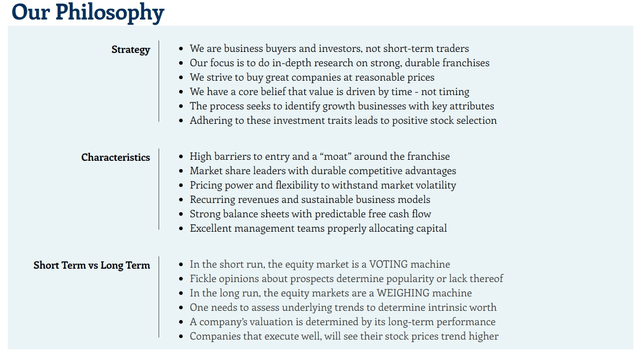

In our opinion, it comes again to our course of, technique, and funding philosophy, which will be summarized on this 1-page from our web site. We’re assured that the businesses we personal possess these essential traits and observe our long-term funding technique.

Manole Capital Philosophy (Manole web site)

Conclusion:

The early days of a brand new bull market are extraordinarily tough to decipher and there will likely be loads of pundits calling it a bear market rally. From 1942 to right now, the typical bear market lasted roughly 11.1 months with a mean decline of (32%). Counter these bearish stats with that of the typical bull market, which lasted for 4.4 years, produced a mean return of +156%. When pessimists attempt to destroy your holidays, merely inform them that “bull markets are longer and stronger than bear markets.”

We’re extra targeted on wanting ahead, than wanting backwards. We try to be anticipatory, not reactive. There have been few buyers that correctly known as the underside in March of 2009 and even fewer that completely timed it in March of 2020. We’re by no means going to be market timers, however we’re going to observe our disciplined funding philosophy and be ready for when a market rebound emerges.

Many have been warning of a coming US and world recession. On JP Morgan’s third quarter convention name, CEO Jamie Dimon mentioned storm clouds will arrive within the subsequent 6 to 9 months and “very critical” headwinds have been looming. The IMF simply said that “the worst is but to return,” and the US economic system will “stall” in 2023. As a substitute of grand proclamations, we choose to know how our firms will carry out in numerous situations. Will they have the ability to go alongside greater costs? Will they regulate their expense base for a brand new surroundings? Are administration groups correctly allocating capital?

Managing cash is tough to do. Possibly it wasn’t too difficult in 2021, when the whole lot appeared to easily head greater. 2022 has been our model of “regular”, the place winners and losers are getting differentiated. This John F. Kennedy quote appears apropos for right now’s market surroundings. He mentioned that “The Chinese language use two brush strokes to write down the phrase ‘disaster.’ One brush stroke stands for hazard: the opposite for alternative. In a disaster, pay attention to the hazard – however acknowledge the chance.” We really feel like right now’s market circumstances are ripe with juicy alternatives.

In conclusion, we perceive that the short-term is impacted by damaging sentiment and market timers. Nonetheless, we won’t stray from our disciplined investing philosophy and technique. We stay true to our investing course of and are profiting from this volatility and uncertainty. Manole Capital stays a long-term investor, in a short-term buying and selling surroundings.

We stay up for talking with you quickly.

Warren Fisher, CFA

Founder and CEO

Manole Capital Administration

|

DISCLAIMER: Agency: Manole Capital Administration LLC is a registered funding adviser. The agency is outlined to incorporate all accounts managed by Manole Capital Administration LLC. Generally: This disclaimer applies to this doc and the verbal or written feedback of any individual representing it. The data offered is accessible for shopper or potential shopper use solely. This abstract, which has been furnished on a confidential foundation to the recipient, doesn’t represent a proposal of any securities or funding advisory companies, which can be made solely by the use of a personal placement memorandum or comparable supplies which comprise an outline of fabric phrases and dangers. This abstract is meant completely for using the individual it has been delivered to by Warren Fisher and it’s not to be reproduced or redistributed to every other individual with out the prior consent of Warren Fisher. Previous Efficiency: Previous efficiency typically just isn’t, and shouldn’t be construed as, a sign of future outcomes. The data supplied shouldn’t be relied upon as the premise for making any funding choices or for choosing The Agency. Previous portfolio traits usually are not essentially indicative of future portfolio traits and will be modified. Previous technique allocations usually are not essentially indicative of future allocations. Technique allocations are primarily based on the capital used for the technique talked about. This doc could comprise forward-looking statements and projections which are primarily based on present beliefs and assumptions and on info at the moment obtainable. Threat of Loss: An funding entails a excessive diploma of danger, together with the potential for a complete loss thereof. Any funding or technique managed by The Agency is speculative in nature and there will be no assurance that the funding goal(s) will likely be achieved. Traders have to be ready to bear the danger of a complete lack of their funding. Distribution: Manole Capital expressly prohibits any copy, in exhausting copy, digital or every other kind, or any re-distribution of this presentation to any third celebration with out the prior written consent of Manole. This presentation just isn’t supposed for distribution to, or use by, any individual or entity in any jurisdiction or nation the place such distribution or use is opposite to native legislation or regulation. Further info: Potential buyers are urged to fastidiously learn the relevant memorandums in its entirety. All info is believed to be cheap, however contain dangers, uncertainties and assumptions and potential buyers could not put undue reliance on any of those statements. Data supplied herein is offered as of the date within the header (until in any other case famous) and is derived from sources Warren Fisher considers dependable, but it surely can not assure its full accuracy. Any info could also be modified or up to date with out discover to the recipient. Tax, authorized or accounting recommendation: This presentation just isn’t supposed to supply, and shouldn’t be relied upon for, accounting, authorized or tax recommendation or funding suggestions. Any statements of the US federal tax penalties contained on this presentation weren’t supposed for use and can’t be used to keep away from penalties underneath the US Inner Income Code or to advertise, market or suggest to a different celebration any tax associated issues addressed herein. |