Yield compression is usually a ache level for gear lessors and financing companies, particularly in a rising fee surroundings.

Rising rates of interest can negatively affect returns in a typical warehouse-to-securitization financing construction. Let’s discover these dangers and how one can mitigate them.

Background

The US entered a rising rate of interest surroundings in March 2022 after two years of short-term charges close to 0% and historic lows for long-term charges.

The Fed has overseen 6 fee hikes in as many conferences this 12 months. The questions relating to future hikes stay: how excessive, how briskly, and the way lengthy?

The latest minutes point out continued hikes into 2023 however there stays a excessive diploma of uncertainty and volatility within the markets.

The yield curve turns into downward sloping (inverted) within the second half of 2023, and this inversion has been current within the curve for a lot of the final 6 months. There may be broad-based market consensus that this a powerful recession indicator. Traditionally, the quick finish of the yield curve tends to be much less risky than the lengthy finish however at present we’re in a singular second. Since June, each the 2-year and 10-year USD swap charges have moved by 20+bps, intraday. This determine was considerably much less risky over the identical interval final 12 months. Given comparatively massive every day actions, it’s very laborious to choose the “proper” second to repair your fee.

Your Warehouse Facility

For a lot of companies, a warehouse is designed to supply versatile liquidity to construct origination quantity – although typically at the next all-in fee than a securitization offers. This has develop into dearer in 2022 as charges have risen.

How do you deal with quick time period rate of interest threat in a risky market? How do you protect flexibility to implement different financing selections? How do you purchase your self time to seek out the suitable second for a securitization?

Choices-based hedging is especially properly suited to a warehouse facility. One of the widely-used choices, an rate of interest cap, features like a bespoke insurance coverage coverage towards an increase in charges. Basically, caps are very liquid, and these merchandise can simply be tailor-made and modified to the chance profile of a given origination pool. The thought is to purchase the correct quantity of protection for the correct quantity of time.

Instance:

You anticipate originations to amass over a 6-month interval with an general WAL of 40 months. Whereas your goal is to pool and securitize semi-annually, spreads within the ABS market have widened. This has made you rethink i) whenever you need to re-enter the market and ii) should you ought to consider different financing options. You establish that your window is now 6-10 months and {that a} 100bps enhance in charges from present ranges would compromise your goal NIM (internet curiosity margin) given your current ebook.

You buy an rate of interest cap in your forecasted warehouse balances for a 10-month interval (the present exterior date). Your strike fee of 4.75% is ~100bps over your present index (1M Time period SOFR). Over the following 10months, if 1M Time period SOFR is beneath 4.75% you proceed to pay your mortgage curiosity as at all times. Nevertheless, if 1M Time period SOFR is 5.00% (for instance) you’ll obtain a cost from the cap supplier equal to: 0.25% x hedged quantity x one month. Netting the cost you obtain towards your curiosity invoice for that month serves to synthetically scale back your rate of interest from 5.00% to the 4.75% cap fee that you simply bought.

Advantages: you may solely obtain ongoing funds so you may take pleasure in charges beneath the cap; you may at all times terminate the cap early and obtain any residual worth (termination doesn’t price you something).

Prices: Your solely obligation with an rate of interest cap is the upfront premium cost, although within the case of an extension or modification sooner or later, you could then be topic to extra premiums.

Utilizing an rate of interest swap to synthetically repair a warehouse facility is difficult within the present market due to the steepness of the yield curve within the quick time period, the inversion of the yield curve in the long term, and everpresent uncertainty round facility balances and securitization timing. A swap fee at any given time is basically comprised of the typical of the yield curve all through the swap, plus a credit score unfold added by the lender. In a rising fee surroundings, swapping usually means paying the next fee instantly vs. floating on the prevailing index fee (e.g. SOFR, LIBOR), as a result of ahead charges on common might be increased. Moreover, there’s an ongoing obligation with a swap, which may result in materials breakage price ought to exit be sooner than deliberate. Choices (reminiscent of caps or corridors) can present flexibility and important general price financial savings in contrast with swapping to a hard and fast fee.

Hedging incrementally, over time with an options-based technique can protect a desired internet rate of interest margin and suppleness—enhancing the advantages of a warehouse facility. Swaps are nice instruments, nevertheless, and will be useful within the context of hedging an upcoming securitization.

Your Securitization

Tools leasing and financing companies usually use the securitizations to entry competitively priced debt that’s matched to the underlying leases or loans. As you construct originations, how do you make sure that a future securitization achieves your required NIM? How do you purchase your self time to seek out the suitable time for a securitization?

Two hedge methods will be acceptable on this context: ahead beginning swaps and swaptions. Each work to hedge your future securitization fee in an effort to protect NIM. Nevertheless ahead beginning swaps have restricted flexibility whereas swaptions include an upfront price (like a cap).

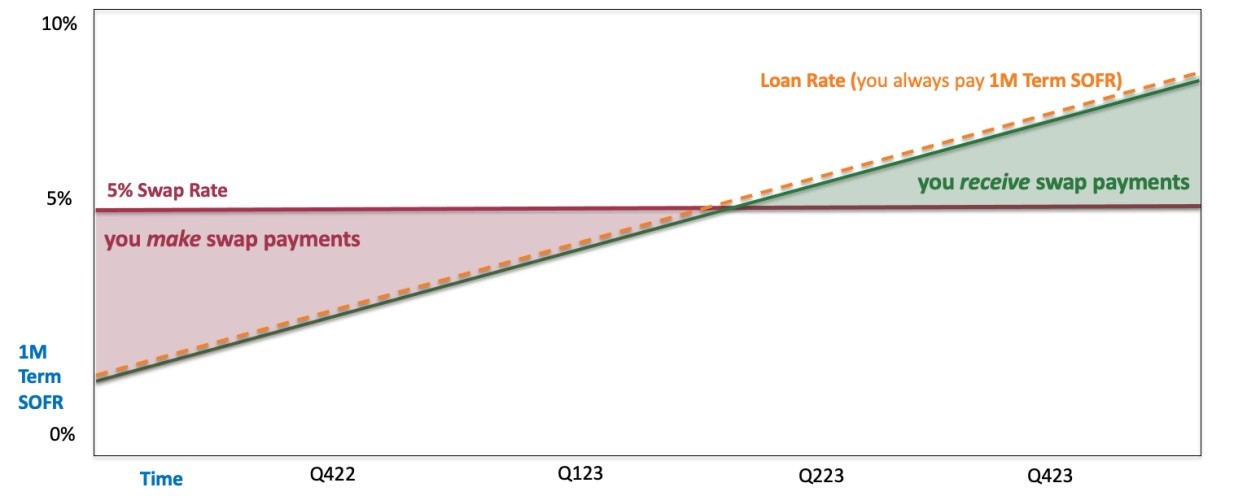

Basis: an rate of interest swap serves to synthetically repair your fee on a specified quantity of debt for a specified time frame. In a simplified instance, you enter into an rate of interest swap on 1M Time period SOFR with a fee of 5.00%. If charges are 4.50% you pay your swap supplier 0.50%, the distinction between your swap fee and the index. Nevertheless, if charges are 5.50% your swap supplier pays you 0.50%. These month-to-month calculations are primarily based on the quantity hedged that month. As a result of swaps contain a possible future obligation in your half, your swap supplier will need some type of collateral to make sure you preserve your obligations. Swaps are sometimes executed with a lender so that you simply received’t have to publish money / money equal to be able to enter right into a swap.

Instance:

You will have amassed an acceptable quantity of originations and have decided the ABS market is pricing properly. You anticipate to shut in your upcoming securitization in 3-5 months. You establish that {that a} 50bps enhance in charges from present ranges would compromise your goal NIM given your current ebook. That ebook has a WAL of 40 months.

Path A: Ahead Beginning Swap. You enter right into a ahead beginning swap along with your warehouse facility lender. The swap is structured to reflect your anticipated securitization: swap begin date = securitization time limit, swap finish date = 40 months; hedged quantity = anticipated securitization quantity, and so on. Your swap fee is 5.00%. Assuming all goes based on plan, on the date you shut on the securitization you additionally terminate the ahead beginning swap. In doing so, you both make or obtain a cost primarily based on the present market fee. That cost, netted with the precise securitization fee would synthetically give you a 5.00% index on the securitization. Let’s break down the funds.

- The swap fee on the time limit = 5.50%. Your swap supplier pays you 0.50% x the hedged quantity x 40 months. Your efficient securitization index fee is 5.00%.

- The swap fee on the time limit = 4.50%. You pay your swap supplier 0.50% x the hedged quantity x 40 months. Your efficient securitization index fee is 5.00%.

Advantages: you may obtain a identified future fee with out an upfront money cost.

Prices: you can not make the most of falling charges; you could pay to terminate the swap; you could incur an extra charge to increase or modify the swap.

Path B: Swaption. A swaption is used to hedge a future fastened fee. It features like a ceiling or a restrict and offers you with a identified, future, worst-case fee. Identical to a cap, you’ll pay for this selection upfront. In a simplified instance, you enter right into a swaption on the long run, 40-month swap fee with a strike fee of 5.00%. If the long run swap fee is 4.50% you merely profit from a decrease fee. Nevertheless, if the long run swap fee is 5.50% your swaption supplier pays you 0.50%. This calculation is predicated on the quantity hedged and the period. Let’s break down the funds.

- The swap fee on the time limit = 5.50%. Your swap supplier pays you 0.50% x the hedged quantity x 40 months. Your efficient securitization index fee is 5.00%.

- The swap fee on the time limit = 4.50%. Your efficient securitization index fee is 4.50%.

Advantages: you may solely obtain funds, so you may take pleasure in charges beneath the swaption fee; you may at all times terminate the swaption early and obtain any residual worth (termination doesn’t price you something).

Prices: upfront cost for the choice; you could incur an extra charge to increase or modify the swaption.

The important thing to successfully managing your agency’s rate of interest threat is to seek out the steadiness between your threat tolerance and your hedge finances. The objective is to focus in your funding objectives whereas making certain your financing selections improve (quite than hinder) these returns.

ABOUT THE AUTHOR: Christina Ochs, President of The Company for Curiosity Price Administration, has labored in rate of interest threat administration for the previous 18 years, gaining expertise in nearly each operational position on the CIRM. Having first earned her bachelor’s diploma from New York College she then gained an MBA from St. John’s College of Rome. A passionate chief, Christina is a member of the Girls’s Presidents Group. She additionally sits on varied boards together with the Girls’s Board of The Museum of Modern Artwork (Chicago), The Chicago Chamber Music Society, the Energetic Transport Alliance, and CASA (Court docket Appointed Particular Advocates) of Cook dinner County.