RiverNorthPhotography

Introduction

Tyson Meals (NYSE:TSN) is likely one of the largest meals producers and protein manufacturers on the planet. With many identified manufacturers like Tyson, Jimmy Dean, Ball Park, and Hillshire Farm, shoppers throughout the US purchase rooster breast to hotdogs in grocery shops every week. The meals trade, particularly protein manufacturing, ebbs and flows with the financial system and atmosphere, inflicting lower than linear outcomes for the enterprise. For instance, in the USA we presently have the worst avian flu ever seen, affecting rooster provide, demand, together with pricing and volumes. That’s the reason you will need to have a look at the long-term developments and averages when investing in Tyson. If that’s finished, we are able to see the enterprise has trended upward during the last decade and trades at a 12x P/E ratio.

Lengthy-Time period View & Monetary Historical past

Firm As A Complete

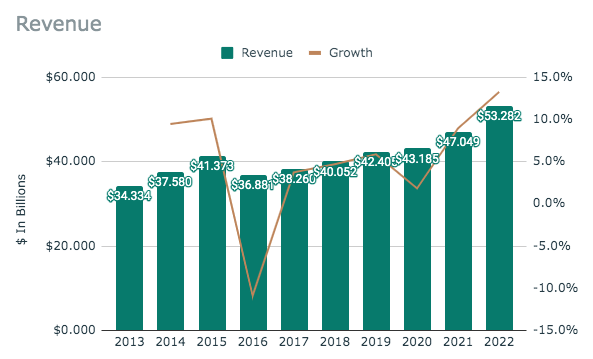

Tyson Meals Income (SEC.gov)

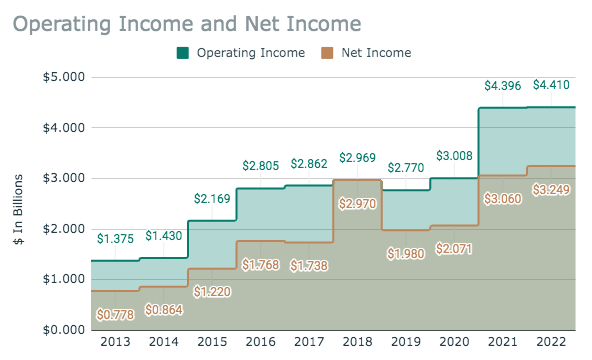

Tyson Meals Working & Web Revenue (SEC.gov)

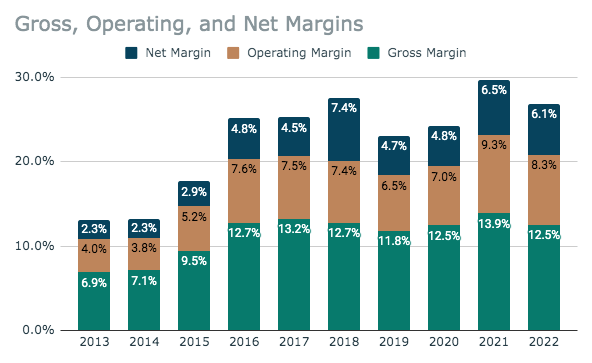

Tyson Meals Margins (SEC.gov)

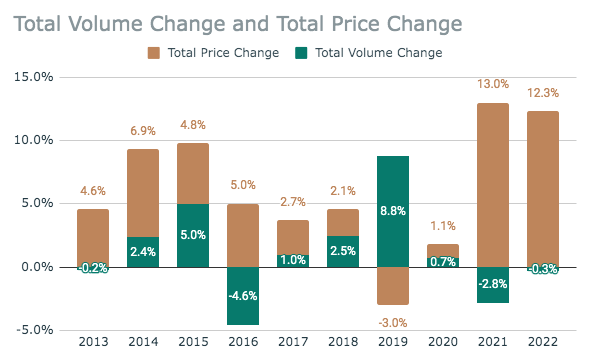

Tyson Meals Quantity & Worth Change Per Yr (SEC.gov)

Tyson has at all times been an organization on the whims of provide and demand. Many components, environmental and financial, have a direct impact on the corporate’s enterprise. Due to this, I consider you will need to have a look at a protracted interval of the enterprise’s outcomes to get a transparent image. As might be seen above, Tyson has a historical past of an upward trajectory in income, however it isn’t constant yr to yr. During the last ten years, Tyson has seen income develop at a CAGR of 4.49%. The identical development follows alongside within the working and internet earnings too. Each have a basic progress development, however such progress will not be constant. Working and internet earnings have grown at charges of 12.36% and 15.37% every over the previous decade.

The rationale the outcomes are so variant is as a result of altering in costs and volumes annually. Anyone yr may produce a variant of various pricing and quantity progress or decline. This, due to this fact, impacts income, margins, working, and internet earnings. Total although, Tyson is nice at ensuring the enterprise publish mixed progress it doesn’t matter what, even when it varies by double digits per yr.

By Section

Wanting deeper into every phase exhibits this development, and the way one phase can see massive swings year-to-year from environmental and financial challenges.

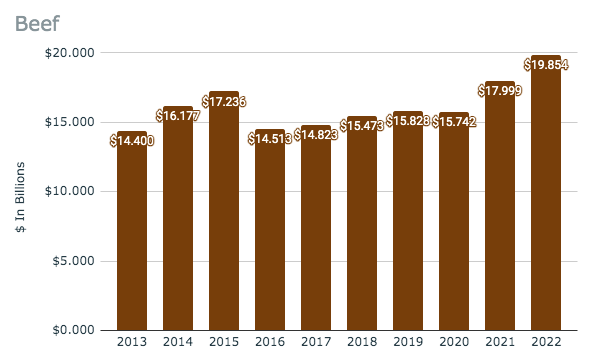

Tyson Beef Income (SEC.gov)

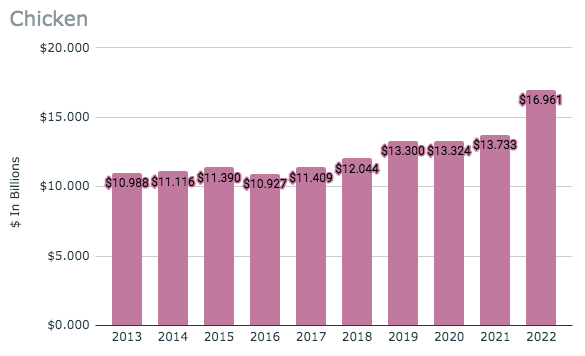

Tyson Hen Income (SEC.gov)

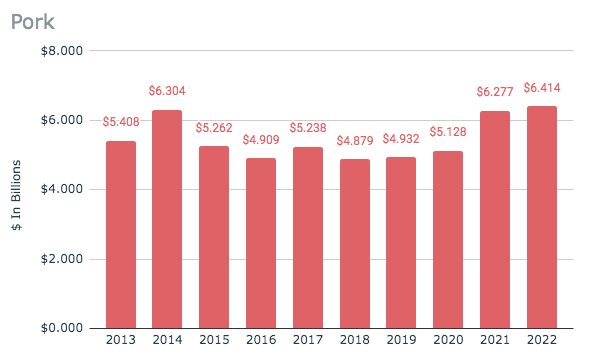

Tyson Pork Income (SEC.gov)

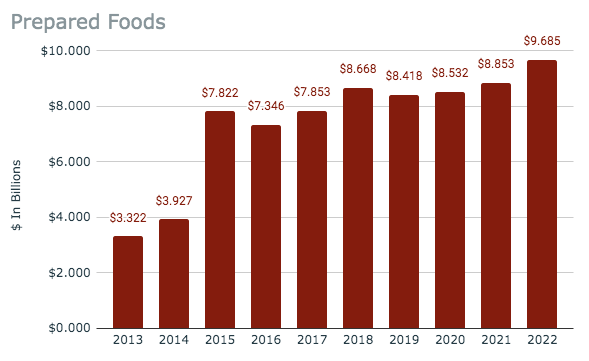

Tyson Ready Meals Income (SEC.gov)

every phase’s revenues exhibits a few of these swings. The Beef, Pork, and Ready Meals segments appear to see way more variability in income over the previous decade, whereas the Hen phase exhibits way more consistency.

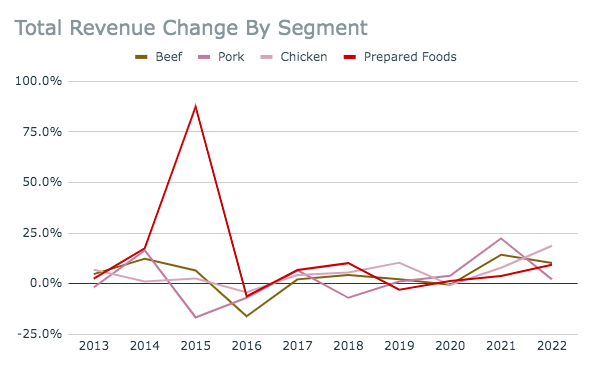

Tyson Meals Income Change Per Yr By Section (SEC.gov)

The graph above does an important job of exhibiting the final development but additionally the variance in every phase’s income progress or decline annually. What is clear is that enormous features or losses are quite common, however over time low progress is the tendency.

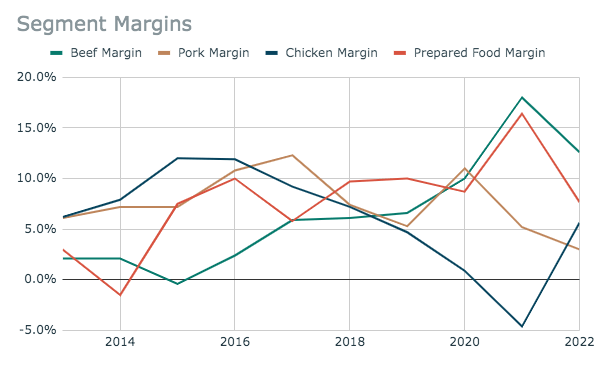

Tyson Meals Margin By Section (SEC.gov)

The environmental and financial components in any given yr have an effect on provide and demand and due to this fact, quantity, pricing, and prices. The above graph exhibits the working margins for every phase over time, and they aren’t constant in any respect. That is as a result of reactionary nature of the enterprise. Tyson first must know if the product will value extra to supply after which regulate pricing, which can have an effect on the volumes bought. This reactionary cycle is why margins, income, and progress charges fluctuate a lot from yr to yr.

Total, what I take for that is that Tyson cannot be analyzed primarily based on one yr alone. The corporate needs to be checked out from a long-term viewpoint. If one appears to be like at it this fashion, one can see the final development is low single-digit progress over time.

Valuation

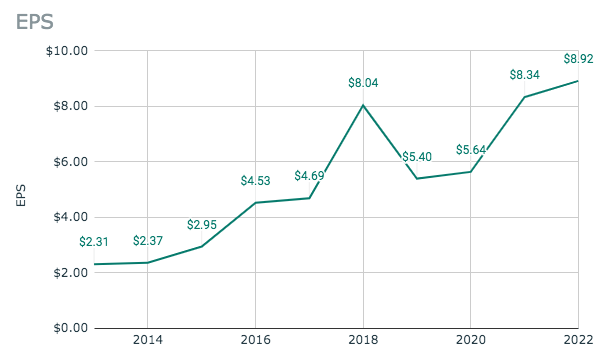

Tyson Meals EPS (SEC.gov)

Due to the variability in earnings on a year-to-year foundation, the valuation of Tyson additionally needs to be checked out on a long-term scale. A easy method to do that is common it out. The typical EPS for the corporate over the previous decade comes out to be $5.20. Now doing tends to skew the typical downward by not considering any acquisitions revamped the last decade (which is commonplace for Tyson). However to me, this simply bakes in a margin of security. With the value of the inventory presently round $67 per share, the corporate trades at a P/E of 12.88x utilizing the ten-year common EPS. At this value stage and with an already baked-in margin of security, the corporate is buying and selling at a discount.

Conclusion

Tyson has seen many ups and downs during the last decade, which is in true trade kind. As occasions just like the avian flu, mad cow illness, drought, inflation, and so on. have an effect on the protein market, Tyson sees changes in pricing, volumes, and margins affecting any given yr to the draw back or upside. However the long run, the enterprise has a transparent upward trajectory and trades at 12x common ten-year earnings. As a present holder of the inventory, I’ve been including extra to my place throughout these occasions.