Drew Angerer

Introduction

As a dividend development investor, I continuously search further alternatives to amass income-producing belongings. My present portfolio generates a dependable stream of earnings. I generally add to my present positions once I discover them enticing. On different events, I begin new positions to diversify my holdings additional. I’m making an attempt to capitalize on the current volatility to get extra earnings for a beautiful value.

One among my favourite sectors is the healthcare sector. Firms on this sector earn cash by bettering folks’s lives. From a monetary perspective, folks will keep away from chopping healthcare bills for so long as potential. I personal shares in medical gadgets, prescription drugs, drug shops, and distributors. On this article, I’ll analyze one in every of my present positions: Bristol-Myers Squibb (NYSE:BMY).

I’ll analyze the corporate utilizing my methodology for analyzing dividend development shares. I’m utilizing the identical methodology to make it simpler to check researched firms. I’ll look at the corporate’s fundamentals, valuation, development alternatives, and dangers. I’ll then attempt to decide if it is a good funding.

In search of Alpha’s firm overview reveals that:

Bristol-Myers Squibb Firm discovers, develops, manufactures, and markets biopharmaceutical merchandise worldwide. It presents merchandise for hematology, oncology, cardiovascular, immunology, fibrotic, neuroscience, and Covid-19 illnesses. It sells merchandise to wholesalers, distributors, pharmacies, retailers, hospitals, clinics, and authorities businesses. The corporate was previously generally known as Bristol-Myers Firm. The corporate was based in 1887 and is headquartered in New York, New York.

Fundamentals

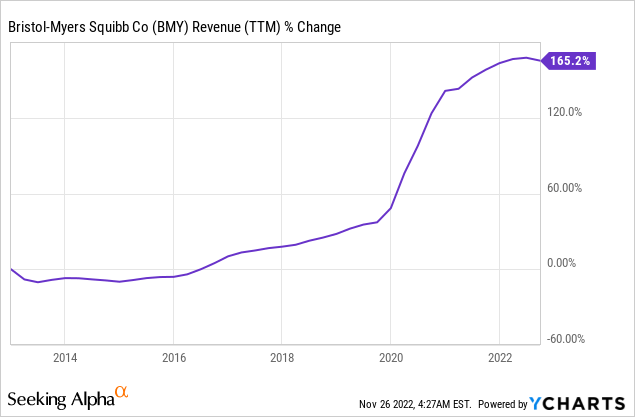

Revenues of Bristol-Myers Squibb elevated by 165% during the last decade. The rise in gross sales outcomes from the corporate’s drug pipeline and important acquisitions. The 2 predominant acquisitions have been Celgene for $90B and MyoKardia for $13B. Sooner or later, analysts’ consensus, as seen on In search of Alpha, expects Bristol-Myers Squibb to continue to grow gross sales at an annual charge of ~2.5% within the medium time period.

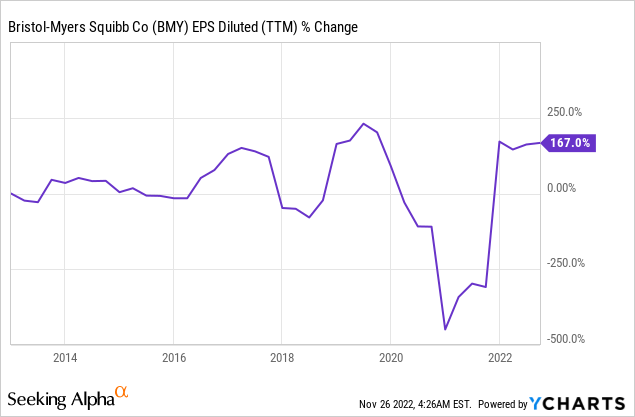

The EPS (earnings per share) has elevated equally over the previous decade. The expansion within the EPS occurred regardless of the rise within the variety of shares as the corporate managed to chop prices following acquisitions. The fee-cutting measures improved the margins of the corporate. Sooner or later, analysts’ consensus, as seen on In search of Alpha, expects Bristol-Myers Squibb to continue to grow gross sales at an annual charge of ~3% within the medium time period.

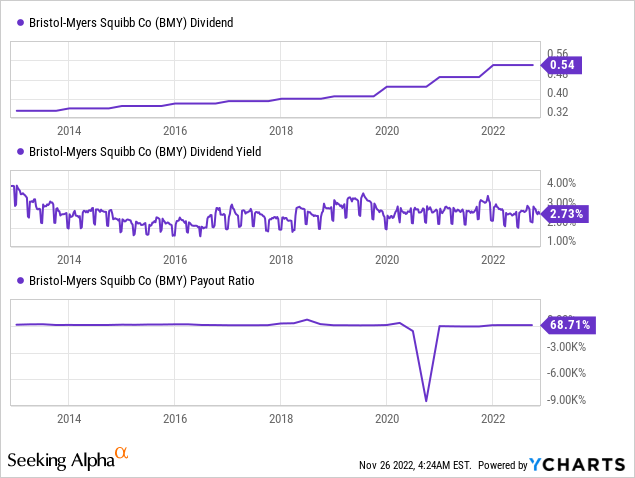

The dividend is one other distinguished prospect of Bristol-Myers Squibb. The corporate has elevated the dividend for 15 years and hasn’t decreased it for greater than 50 years. The present dividend yield stands at 2.73% and is protected as the corporate pays lower than 70% of its GAAP earnings and fewer than 30% of its non-GAAP earnings. Traders ought to anticipate one other dividend enhance in December as the corporate is prone to enhance its streak, which is able to seemingly be mid-single digits, in step with the EPS development.

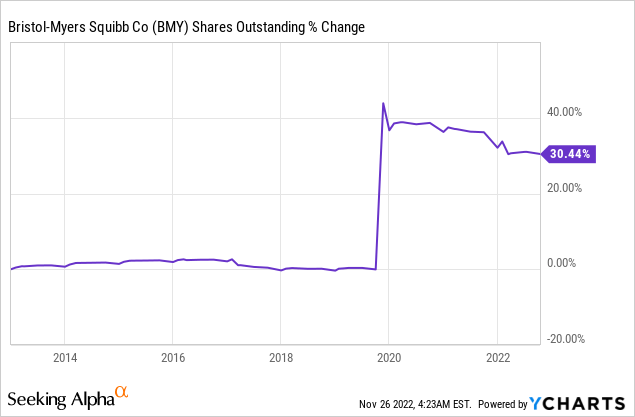

One other type of returning capital to shareholders apart from dividend funds is share repurchases. Over the past decade, the variety of shares elevated by 30% as a result of firm’s acquisitions which have been paid partially utilizing firm inventory. Since then, the corporate has been shopping for again its shares, and during the last three years, it has decreased the variety of shares by greater than 3%. Buybacks are efficient primarily when the valuation is low, as the corporate buys extra shares for much less.

Valuation

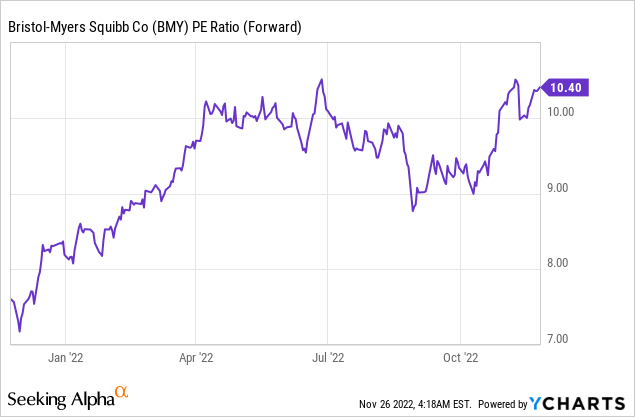

The P/E (value to earnings) ratio of Bristol-Myers Squibb, when making an allowance for the corporate’s 2022 EPS forecast, stands at 10.4. For my part, this can be a low valuation for an organization with strong fundamentals. The graph beneath reveals how the P/E ratio elevated from lower than 7 to 10.4 within the final twelve months. The present valuation continues to be a good entry level for a top quality firm like Bristol-Myers Squibb.

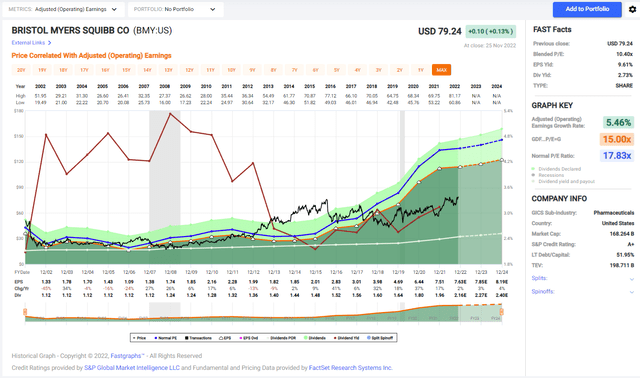

The graph beneath from Fastgraphs emphasizes how regardless of the rise in EPS, the share value of Bristol-Myers Squibb remained depressed. You possibly can see how in 2016, there was a disconnection between the blue line and the worth line. The present P/E ratio of 10 is considerably decrease than the common P/E during the last 20 years, which stands at virtually 18. Due to this fact, I consider that the shares are enticing from a valuation perspective.

Fastgraphs

To conclude, Bristol-Myers Squibb combines nice fundamentals with a good valuation. The corporate grows its high and backside line and fuels dividend development and buybacks. On the identical time, it trades far beneath its common valuation, making it an thrilling prospect for dividend development traders. It will likely be enticing if the corporate has future alternatives and restricted dangers.

Alternatives

The drug Repotrectinib is a particularly promising drug for lung most cancers. The FDA has granted a breakthrough remedy designation to Repotrectinib. When Bristol-Myers Squibb acquired Turning Level Therapeutics in 2022, it turned the proprietor of that promising drug. The corporate depends on the quick approval of this breakthrough remedy.

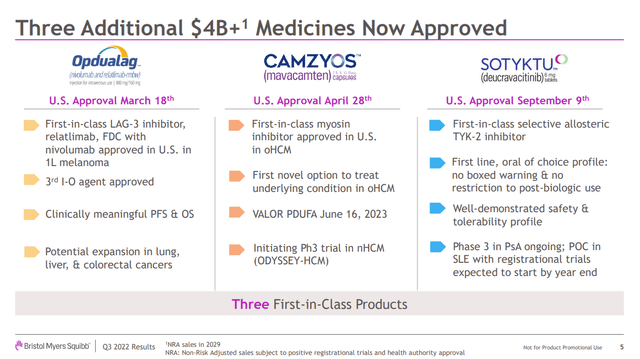

Portfolio renewal can also be a major development catalyst for Bristol-Myers Squibb. The corporate is consistently creating new medication to switch the gross sales of older medication. Essentially the most promising merchandise that can attain the market within the quick time period are Opdualag, Camzyos, and Sotyktu. These three merchandise have been authorized and are anticipated to convey $4B in annual gross sales, which equates to virtually 10% of the present gross sales.

Bristol-Myers Squibb Q3 Outcomes

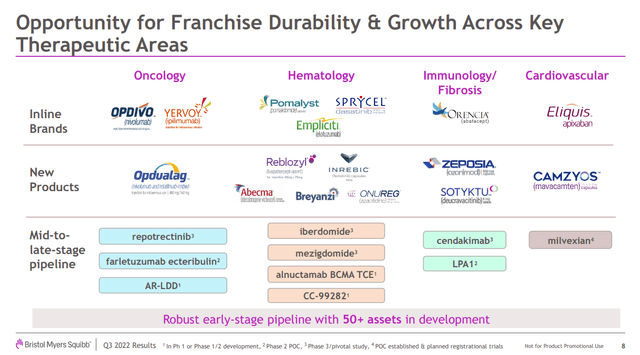

One other alternative for the corporate is its diversification. It sells its merchandise throughout the globe and would not need to rely solely on one or a number of markets. As well as, it sells medication for various essential therapeutic areas: oncology. Hematology, immunology, and cardiovascular. It additionally enjoys a diversified, balanced pipeline that features merchandise virtually able to market and early-stage prospects. Diversification makes the corporate extraordinarily versatile because it invests in numerous areas and markets.

Bristol-Myers Squibb Q3 Outcomes

Dangers

A brief-term threat for Bristol-Myers Squibb is the forecasted gradual development within the coming three years. The corporate and the analysts protecting it are nicely conscious of the present merchandise and those being launched within the very quick time period. They’re inadequate to propel significant development in order that the corporate could depend on M&A and its long-term early-stage prospects. The chance degree is greater when the expansion prospects are additional away on the timeline.

One other threat for Bristol-Myers Squibb is the competitors. The pharmaceutical world is extremely aggressive with large firms like Merck (MRK) and Novartis (NVS), in addition to many startups. Each failure to launch a product in its pipeline could put the corporate’s skill to develop in a path in danger. Due to this fact, it’s a high-risk reward play.

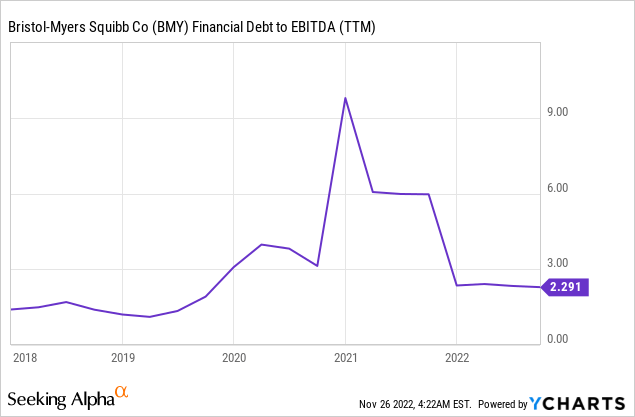

The debt burden is one other threat for Bristol-Myers Squibb. The debt degree elevated by greater than 60%, and in the mean time, the debt-to-equity ratio stands at 2.3. Whereas the debt degree itself shouldn’t be dangerous for the corporate, along with the upper charges, it will likely be tougher for the corporate to finance further acquisitions if it strives to develop extra via M&A.

Conclusions

Bristol-Myers Squibb is a superb firm from each perspective. The corporate presents traders strong fundamentals with secure gross sales and EPS development even throughout unstable occasions. It additionally returns capital to shareholders by buybacks and dividends making it straightforward to share the success. The present valuation can also be promising as it’s decrease than common.

Furthermore, the corporate has a number of development alternatives within the medium and long run, and it will possibly gas future development with its pipeline. The dangers appear restricted and never very distinctive to Bristol-Myers Squibb. I consider the shares are a BUY for long-term dividend development traders on the present value. Shares generally is a STRONG BUY if the share value reaches $65-$70 once more, as there will probably be a excessive dividend yield and much more margin of security.