Lycopodium (ASX:LYL) has had an ideal run on the share market with its top off by a big 13% over the past three months. We surprise if and what function the corporate’s financials play in that worth change as an organization’s long-term fundamentals often dictate market outcomes. Notably, we will probably be being attentive to Lycopodium’s ROE at present.

ROE or return on fairness is a great tool to evaluate how successfully an organization can generate returns on the funding it acquired from its shareholders. In less complicated phrases, it measures the profitability of an organization in relation to shareholder’s fairness.

Try our newest evaluation for Lycopodium

How Do You Calculate Return On Fairness?

ROE might be calculated through the use of the method:

Return on Fairness = Internet Revenue (from persevering with operations) ÷ Shareholders’ Fairness

So, primarily based on the above method, the ROE for Lycopodium is:

27% = AU$27m ÷ AU$100m (Based mostly on the trailing twelve months to June 2022).

The ‘return’ is the revenue the enterprise earned over the past 12 months. So, because of this for each A$1 of its shareholder’s investments, the corporate generates a revenue of A$0.27.

What Is The Relationship Between ROE And Earnings Progress?

Thus far, we have discovered that ROE is a measure of an organization’s profitability. Relying on how a lot of those earnings the corporate reinvests or “retains”, and the way successfully it does so, we’re then in a position to assess an organization’s earnings development potential. Usually talking, different issues being equal, corporations with a excessive return on fairness and revenue retention, have a better development charge than corporations that don’t share these attributes.

A Aspect By Aspect comparability of Lycopodium’s Earnings Progress And 27% ROE

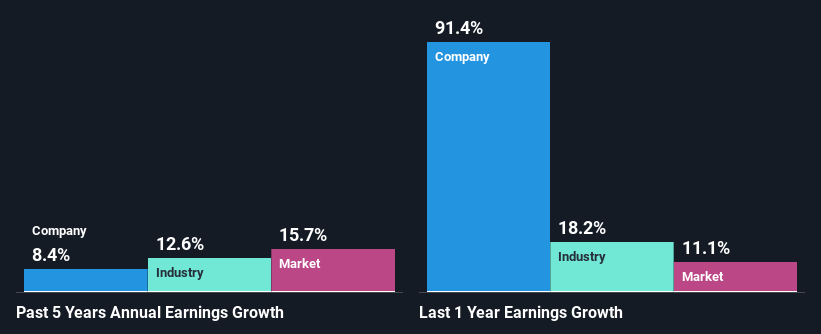

Firstly, we acknowledge that Lycopodium has a considerably excessive ROE. Second, a comparability with the typical ROE reported by the business of 14% additionally does not go unnoticed by us. This probably paved the best way for the modest 8.4% web revenue development seen by Lycopodium over the previous 5 years. development

As a subsequent step, we in contrast Lycopodium’s web revenue development with the business and had been upset to see that the corporate’s development is decrease than the business common development of 13% in the identical interval.

Earnings development is a large think about inventory valuation. What traders want to find out subsequent is that if the anticipated earnings development, or the dearth of it, is already constructed into the share worth. Doing so will assist them set up if the inventory’s future seems promising or ominous. One good indicator of anticipated earnings development is the P/E ratio which determines the worth the market is prepared to pay for a inventory primarily based on its earnings prospects. So, chances are you’ll need to verify if Lycopodium is buying and selling on a excessive P/E or a low P/E, relative to its business.

Is Lycopodium Effectively Re-investing Its Earnings?

Whereas Lycopodium has a three-year median payout ratio of 69% (which suggests it retains 31% of earnings), the corporate has nonetheless seen a good bit of earnings development up to now, that means that its excessive payout ratio hasn’t hampered its capability to develop.

In addition to, Lycopodium has been paying dividends for at the very least ten years or extra. This exhibits that the corporate is dedicated to sharing earnings with its shareholders.

Abstract

In complete, it does seem like Lycopodium has some optimistic features to its enterprise. The corporate has grown its earnings reasonably as beforehand mentioned. Nonetheless, the excessive ROE may have been much more useful to traders had the corporate been reinvesting extra of its earnings. As highlighted earlier, the present reinvestment charge seems to be fairly low. Up until now, we have solely made a brief examine of the corporate’s development knowledge. So it could be value checking this free detailed graph of Lycopodium’s previous earnings, in addition to income and money flows to get a deeper perception into the corporate’s efficiency.

Have suggestions on this text? Involved concerning the content material? Get in contact with us straight. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles will not be supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We purpose to convey you long-term targeted evaluation pushed by elementary knowledge. Word that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

Be part of A Paid Consumer Analysis Session

You’ll obtain a US$30 Amazon Reward card for 1 hour of your time whereas serving to us construct higher investing instruments for the person traders like your self. Join right here