JHVEPhoto/iStock Editorial through Getty Photographs

We had been beforehand bearish on Intel (NASDAQ:INTC), however we imagine after a tough 12 months, it is time to transfer the corporate to a purchase. Our bullish sentiment relies on our perception that INTC’s outlook for 4Q22 and 2023 takes under consideration the weak PC demand and comfortable cloud spending. We count on INTC’s monetary efficiency to stabilize and even enhance throughout 2023. Our purchase thesis is pushed by our perception that the market has lastly priced within the weak point within the PC and cloud spending for probably the most half – one thing we hadn’t seen in earlier quarters. We imagine INTC is headed in the appropriate course to outperform expectations in 2H23.

Close to macroeconomic headwinds present no signal of washing out quickly; we imagine the near-term market stays risky. Nevertheless, we imagine INTC’s inventory pullback over the previous couple of quarters creates a horny entry level for long-term traders, particularly as INTC expands and invests extra critically in its foundry enterprise.

Pricing within the macroeconomic headwinds within the 4Q22 and FY23 outlook

We don’t imagine weak PC demand and comfortable cloud spending have washed out; as an alternative, our bullish sentiment on INTC is as a result of we imagine the weak point is now priced in. Therefore, we’re extra constructive on the corporate outperforming monetary expectations for 2H23. INTC’s 4Q22 outlook expects its three core segments (Shopper Computing (together with Shopper PC), Information Heart, and Edge) to see a sequential decline. INTC is forecasting weaker gross sales primarily based on weaker TAM and as clients undertake stock corrections to stability the supply-demand dynamics.

- Shopper Computing Group (Shopper PC):

We imagine the market has lastly priced within the weak point in INTC’s core enterprise, its PC enterprise. Gartner forecasts worldwide PC shipments to say no 19.5% within the third quarter of 2022. INTC’s largest clients are feeling the churn of the weakening demand, and we count on INTC to really feel the decline as PC Shopper Group makes up greater than 50% of the corporate’s complete income. INTC provides main PC distributors together with Lenovo (OTCPK:LNVGY), Dell (DELL), and HP (HPQ) all of which have reported damaging Y/Y development. We imagine INTC’s declined shipments to clients will enable HPQ, DELL, and Lenovo to undertake stock corrections for 2023. The next desk outlines INTC’s vendor’s unit cargo estimates for 3Q22.

Gartner

Whereas we’re extra assured about INTC’s outlook post-earnings, we nonetheless imagine the corporate’s PC TAMs are too excessive for the present macroeconomic atmosphere. INTC forecasts PC TAM of 270-295M models for 2023. INTC’s Shopper Computing Group’s gross sales in 3Q22 had been up 6% sequentially however down nearly 17% Y/Y.

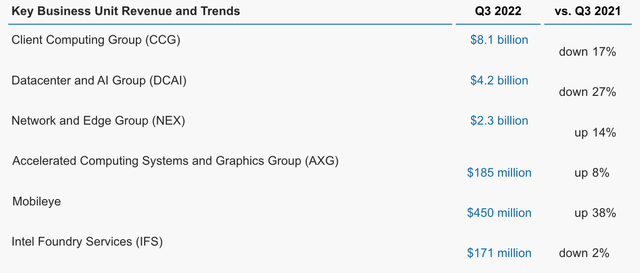

We imagine INTC is headed in the appropriate course on the subject of Information Heart Group as effectively. The corporate’s Information Heart and AI Group suffered a 9% drop in sequential gross sales in 3Q22 and a 27% decline Y/Y. We count on the corporate will proceed to see a comfortable cloud spending atmosphere because the weakening shopper demand spills into cloud spending. We additionally imagine the corporate could also be pressured by competitors within the information heart market. Nonetheless, we expect INTC’s market share loss will reasonable considerably in 2023 because the market has priced in many of the weak point within the PC and cloud spending, in addition to the market share loss to Superior Micro Units (AMD) and ARM-based CPUs. We’re extra optimistic about INTC as we imagine the corporate’s outlook encapsulates the macroeconomic headwinds for 4Q22 and 2023.

The next graph outlines the 3Q22 earnings for every of INTC’s segments.

INTC 3Q22 earnings

What’s occurring on the foundry entrance?

INTC’s working critically to develop into the long run face of the foundry enterprise – America’s subsequent chip-maker at residence. We had been beforehand skeptical about INTC’s capability to develop into a significant foundry participant because the Taiwan Semiconductor Manufacturing Firm (TSM) dominates the market and is best positioned to outspend INTC. Nevertheless, after the CHIPS Act approval and because the “Tech Wars” between the U.S. and China escalate, we’re extra constructive about INTC’s capability to execute its foundry plans. We imagine it’ll take time and plenty of capital for INTC to develop into a significant foundry participant, however we imagine the corporate is laying down a stable basis. We count on it is going to be one other 3 to 4 years earlier than INTC turns into a significant foundry participant. Our bullish sentiment is primarily for long-term traders who’re interested by investing within the firm’s future foundry enterprise and PC market when macroeconomic headwinds ease.

Valuation

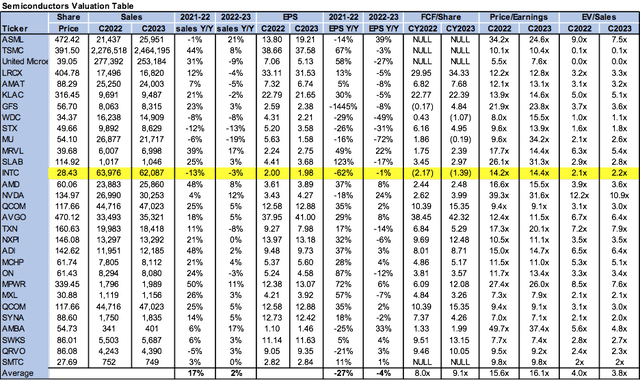

INTC inventory is comparatively low-cost, buying and selling at 14.4x on a P/E foundation C2024 EPS $1.98 in comparison with the peer group common of 16.1x. The corporate is buying and selling at 2.2x EV/C2024 Gross sales vs. the peer group common of three.8x. We imagine INTC inventory gives a horny entry level for the long-term investor at present ranges.

The next chart illustrates INTC’s peer group valuation.

TechStockPros

Phrase on Wall Road

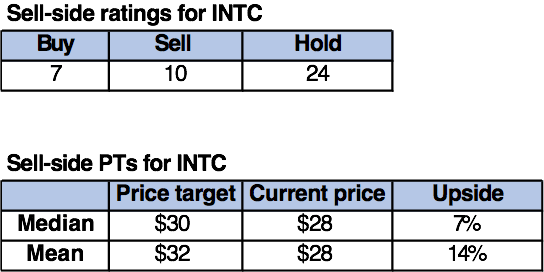

Wall Road is extra bearish on the inventory. Of the 41 analysts, 7 are buy-rated, 24 are hold-rated, and the remaining are sell-rated. We disagree with Wall Road’s bearish sentiment as we imagine INTC is well-positioned to outperform in 2023 for the reason that weak point has been priced into the inventory and outlook for probably the most half. We count on to see INTC’s monetary efficiency enhance over the approaching 12 months. The inventory is buying and selling at $28. The median and imply worth targets are set at $30 and $32, with a possible 7-14%.

The next chart illustrates INTC’s sell-side rankings and worth targets.

TechStockPros

What to do with the inventory

Now that INTC’s outlook for 4Q22 and FY2023 costs within the macroeconomic headwinds, we’re shifting the inventory to a purchase. We’re optimistic in regards to the firm’s monetary efficiency for 2023. We count on INTC to be well-positioned to outperform in 2H23. We additionally imagine INTC is constructing a stable foundry enterprise in the long term. We predict INTC inventory might stay a little bit risky within the close to time period as shopper demand stays weak, however we imagine INTC inventory gives a horny entry level for long-term traders.