YinYang/iStock through Getty Photos

Introduction

Mainz Biomed (NASDAQ:MYNZ) presents traders a possibility to put money into an up-and-coming genetic testing firm that focuses on illness detection. Their major take a look at package is for the lethal, costly, and a tough to detect group of colorectal cancers. This might permit sufferers to have a better solution to frequently test for the early indicators of those illnesses with out the necessity for extra invasive and expensive procedures resembling colonoscopies. Together with the ColoAlert take a look at package, the corporate is a frequent collaborator and repair lab for different diagnostics firms, permitting Mainz to develop fruitful partnerships down the highway that different entry degree firms might not have.

Contemplating that the colorectal take a look at market is massive, early information means that Mainz’s present product presents accuracy benefits over different genetic checks of the identical indication, and the corporate is already engaged on different diagnostic areas, I consider that the present $100 million USD valuation is price a thought for traders which can be prepared to attend for commercialization to really scale up. Nonetheless, there are a couple of bumps within the highway transferring ahead that should be thought-about and the danger and reward is probably not attractive to some. I hope to put out the strengths and weaknesses of the thesis within the article.

For the approaching quarters, the funding is speculative, and the most effective probability for upside depends on not simply ColoAlert, however many different checks.

The ColoAlert Check

For diagnostics firms, whereas there could also be fewer hurdles to leap by way of for achievement in comparison with therapies (pricey improvement course of, strict approval requirements, and so on.), good diagnostics kits can save lives and be worthwhile merchandise for builders. Nonetheless, this additionally means that there’s normally elevated competitors as different firms are additionally capable of fund checks in the identical areas. The flexibility to focus on markets with important complete accessible market (TAM) or alternative is simply as necessary as providing probably the most correct kits.

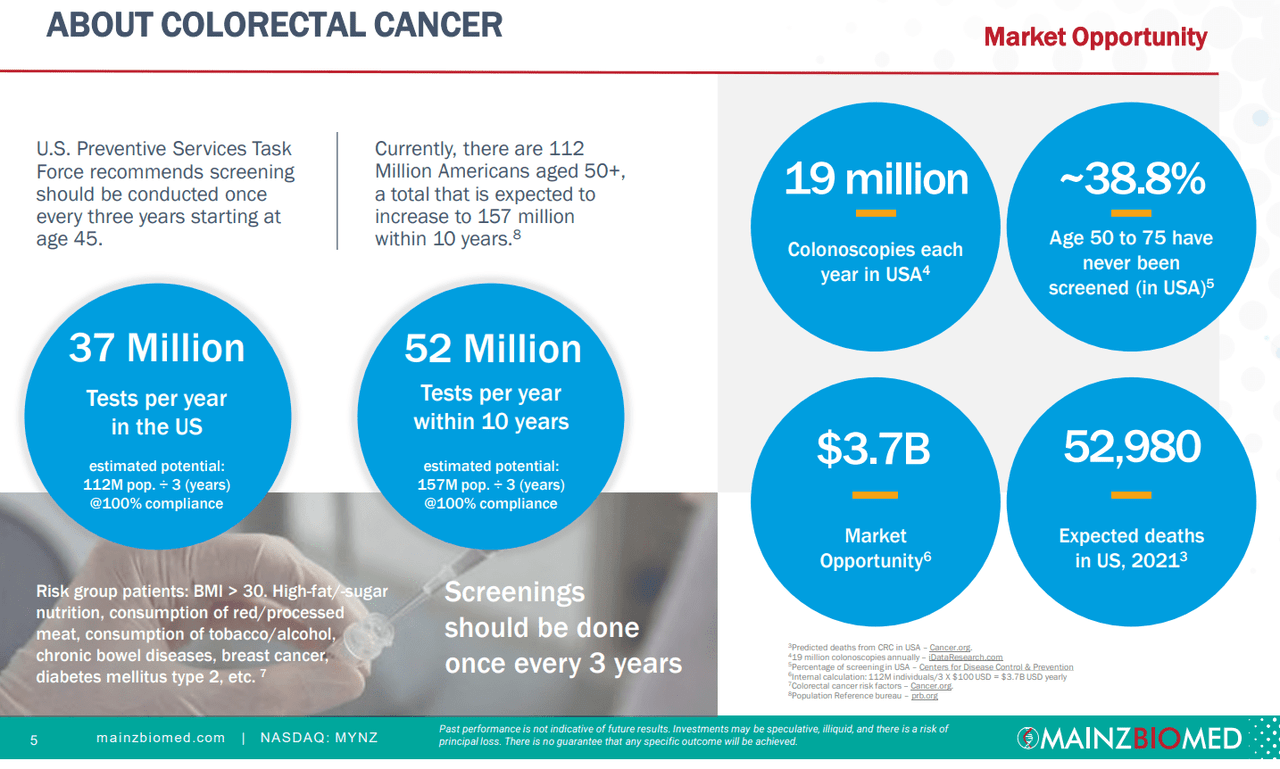

For MYNZ, they test off each packing containers. First, colorectal most cancers is sadly a typical illness that may have an effect on practically all populations. For that reason, preventive screening is widespread and so long as populations age, there will likely be extra threat for colorectal most cancers. Most necessary for diagnostics firms is the truth that healthcare professionals suggest frequent testing, about as soon as each three years beginning at age 45, and this might account for a possible issuance of over 35 million checks per 12 months within the US alone. At $100 per take a look at, that may account for $3.5 billion in revenues per 12 months.

The TAM can be assessed in different methods, whether or not taking a look at individuals over the age of 45 who select to not get screened in any respect, or ~39% of these between 50-75 within the US, or with the 20 million colonoscopies that may be changed per 12 months. Each of those teams could also be seeking to both start non-invasive detection, or substitute common colonoscopies, rising the compliance for these above 45. Nonetheless, this nonetheless lowers the $3.5 million in potential revenues by over 50% as we take away high-risk populations and non-compliance. With time and elevated accuracy of the take a look at package, it could be seemingly that the TAM will progressively enhance, particularly with our getting old societies.

3Q22 Investor Presentation

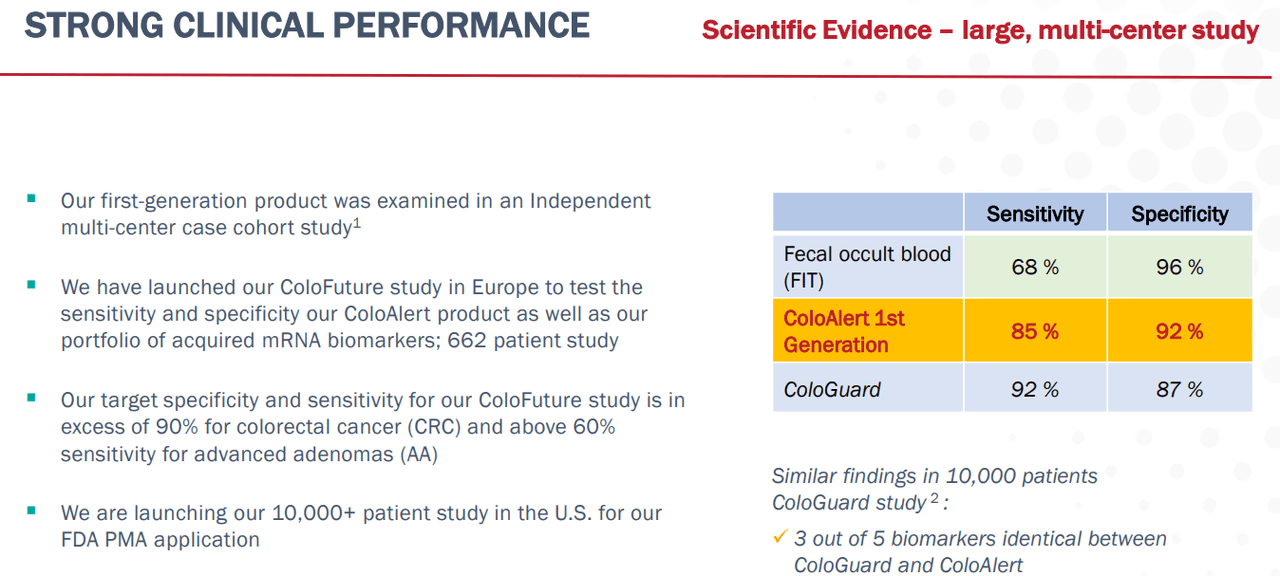

One other threat to contemplate is the truth that there may be competitors within the colorectal most cancers area, and Mainz should develop an advantageous take a look at. The legacy solution to take a look at outdoors of a colonoscopy is with a fecal occult blood take a look at (FIT model) that gives the next proportion of false negatives on account of low sensitivity, however presents few false positives. Then, there may be Actual Sciences’ (EXAS) ColoGuard, a take a look at that’s fairly correct and would be the major competitors for MYNZ. Each firms’ merchandise and information are fairly latest, and so it will likely be necessary to evaluate some great benefits of each transferring ahead. In the meanwhile, I’d say it’s too quickly to inform how competitors will affect Mainz, however at over $500, ColoGuard appears to be the dearer possibility.

3Q22 Investor Presentation

Present Valuation

Mainz Biomed at the moment trades at a $100.1 billion USD market cap and I discover that the valuation is kind of low. A few of that is as a result of 20%+ appreciation of the USD over the previous 12 months in comparison with the Euro, and a few of it’s the greater low cost charges that should be utilized due to the fed. Nonetheless, contemplating that the market is at the moment implying that the $3.5 billion TAM has between a ten and 15% likelihood of success (or proportion of TAM met), the present is kind of favorable for these prepared to ascertain a long-term place. The desk beneath highlights the present valuation on a 15% low cost price foundation over 10 years, together with potential annualized inventory worth efficiency at a 2.5x P/S (EXAS trades at 3.15x however is extra diversified).

|

PoS or Proportion of TAM Met (%) |

Potential Revenues (thousands and thousands USD) |

Current Worth (million USD) |

Low cost or (Premium) (%) |

10 12 months CAGR (%, at 2.5x P/S @ Potential Revenues) |

|

10 |

$350 |

$86 |

(14%) |

24.2 |

|

15 |

$525 |

$130 |

30 |

29.4 |

|

20 |

$700 |

$173 |

73 |

33.1 |

3Q22 Investor Presentation

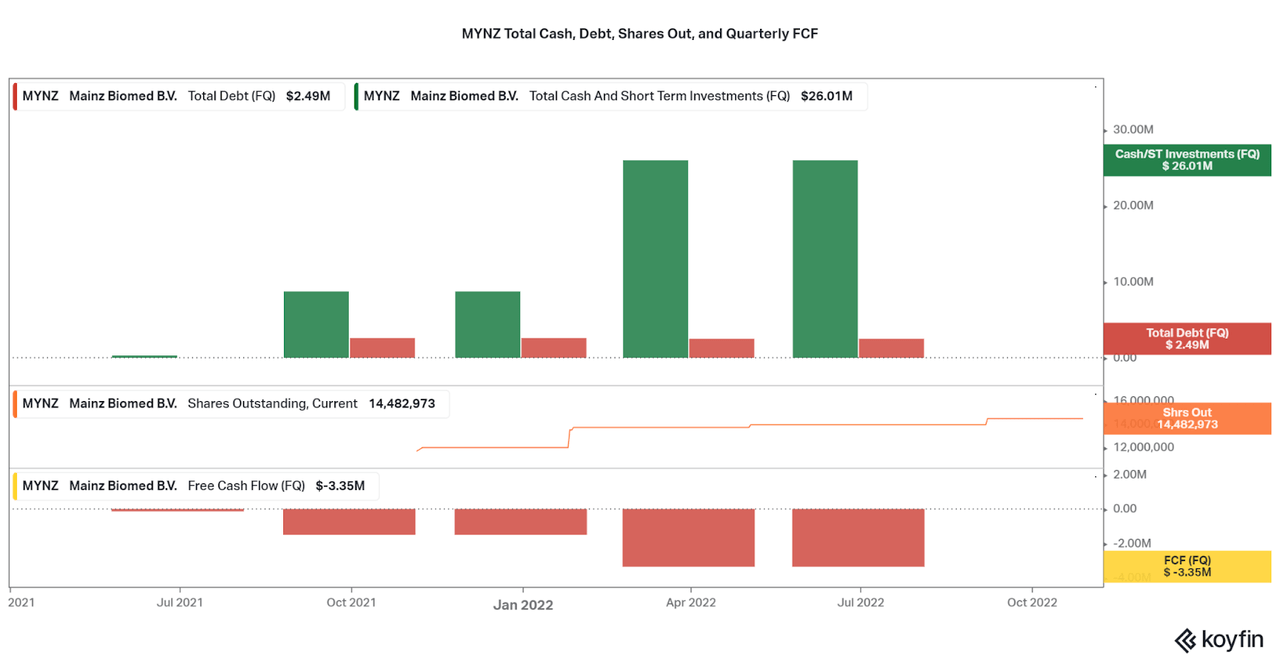

Burn Charge Issues

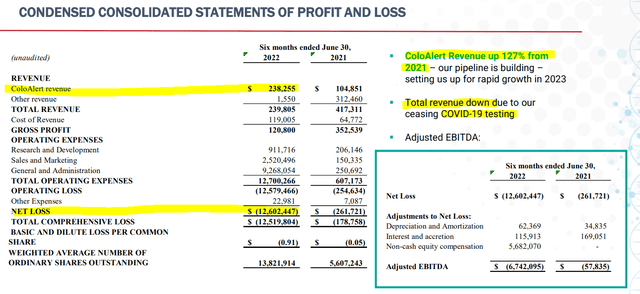

To additional spotlight the long-term capabilities of the funding, Mainz presents a powerful stability sheet with a number of years of operations accessible with present money readily available. At $23 million in internet money as of the primary half of 2022 in comparison with quarterly FCF losses averaging round $3 million, Mainz can help operations for about 2 years. With the present valuation extraordinarily low, I don’t anticipate that MYNZ will dilute to a excessive diploma over the subsequent few years, however issuances of debt are unsure. We might hear administration focus on rising the money stability with the subsequent few earnings reviews.

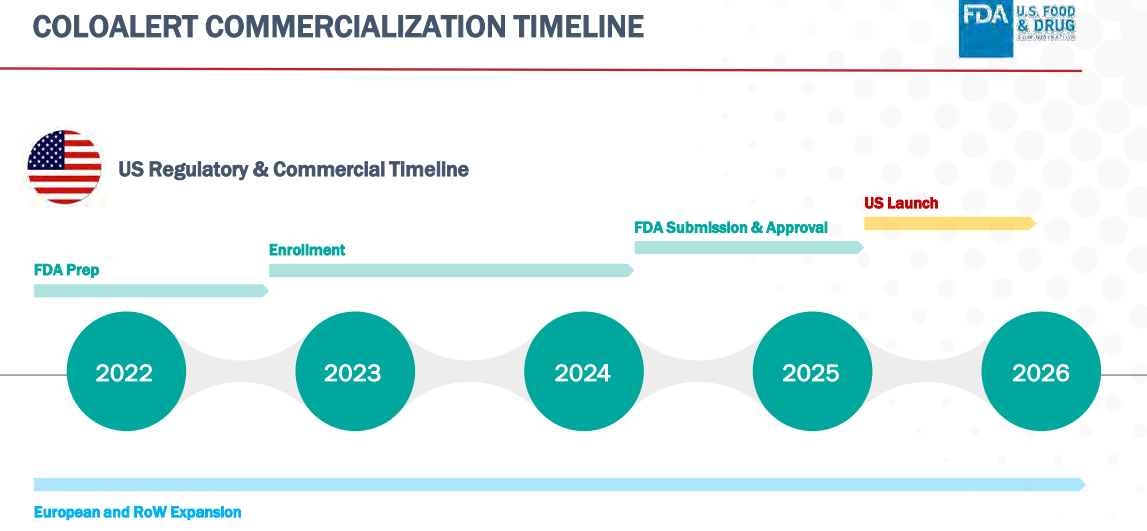

Whereas the burn price appears brief on the floor, preliminary gross sales of the CE/IVD permitted ColoAlert in Europe will enhance money flows over the subsequent two years whereas Mainz works on FDA approval. Gross sales are at the moment rising at over 100% per 12 months, and so I anticipate that Mainz might even grow to be money circulate constructive with simply European revenues by the point of the US approval. Nonetheless, it will likely be necessary to control progress frequently.

Koyfin 3Q22 Investor Presentation

Conclusion

As proven, the present valuation seems to be fairly pessimistic no matter what quantity of the market they meet. Whereas the very fact of the matter is that Mainz must first broaden approvals within the US and Europe, the present information counsel that the approvals ought to happen. As such, I anticipate the share worth to leap considerably. Upon maturation, additional consideration of profitability, expanded indications, and competitors will likely be essential to bolster the trigger, however for a minimum of the subsequent decade plainly upside seems to be fairly favorable for traders. Maybe revenues from areas outdoors of the US will present shock upside, particularly with distribution partnerships already underway.

For the second, I will likely be patiently accumulating shares and can see how improvement performs out. If there may be any spike on account of constructive information, I’ll most probably promote the bounce and attempt to get again in at a cheaper price. Buyers also needs to remember that this can be a risky, low-volume microcap firm, and this funding isn’t suited for many who need a decrease threat funding. Nonetheless, I’ll maintain the long-term alternative in thoughts and consider that Mainz might mature right into a multi-billion genetic take a look at firm in some unspecified time in the future down the highway. Till then, I will likely be keeping track of the developments and can present an replace as essential. Thanks for studying.