Boarding1Now/iStock Editorial by way of Getty Photos

Funding Thesis: Whereas income progress has been encouraging, traders will wish to see additional proof that the corporate can return to profitability and sustainably scale back its long-term debt.

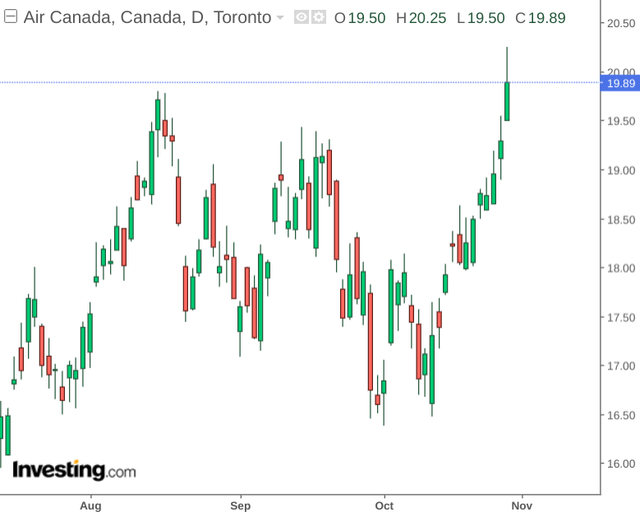

In a earlier article again in August, I made the argument that Air Canada (OTCQX:ACDVF) (TSX:AC:CA) holds potential for longer-term progress, however progress within the short-term might be modest.

The market disagreed, with the replenish by practically 10% since my final article:

investing.com

The aim of this text is to evaluate whether or not Air Canada might have scope to see additional upside from right here, taking current earnings efficiency under consideration.

Efficiency

The latest earnings quarter noticed Air Canada obtain an working margin of 12.1 % – which marked the primary constructive quarterly working margin for the reason that begin of the pandemic.

Working revenues got here in at $5.322 billion, which is over double that of the third quarter of 2021, together with an EBITDA margin of 19.9 %. Whereas the corporate nonetheless noticed a web lack of $508 million this quarter, this was down from a web lack of $640 million within the third quarter of 2021.

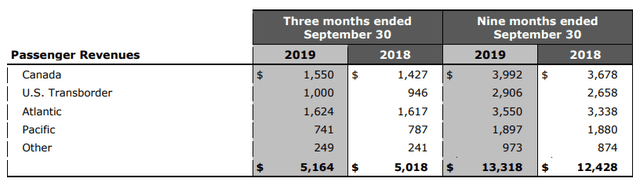

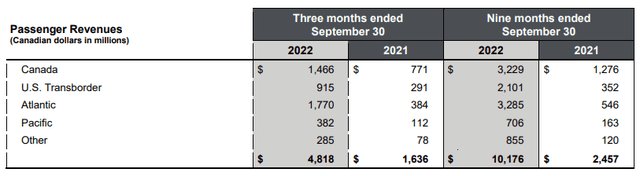

Furthermore, when evaluating passenger revenues throughout geographies – we are able to see that the corporate is beginning to see income ranges method that of Q3 2019 as soon as once more:

Q3 2019 Passenger Revenues

Air Canada Condensed Consolidated Monetary Statements and Notes Quarter 3 2019

Q3 2022 Passenger Revenues

Air Canada Condensed Consolidated Monetary Statements and Notes Quarter 3 2022

Moreover, income passenger miles and out there seat miles are up sharply on that of final 12 months. For Q3 2019, income passenger miles and out there seat miles got here in at CAD 27.954 billion and 32.457 billion respectively.

Information Launch: Air Canada Studies Third Quarter 2022 Monetary Outcomes

As such, we are able to additionally see that these metrics are making their means again in the direction of 2019 ranges.

From a steadiness sheet standpoint, we are able to see that the short ratio (calculated as present belongings much less inventories throughout present liabilities) has risen to above 1 – indicating that Air Canada has enough liquid belongings to cowl its present liabilities:

| September 2019 | September 2022 | |

| Whole present belongings | 7415 | 10195 |

| Plane gasoline stock | 104 | 238 |

| Spare elements and provides stock | 107 | 108 |

| Whole present liabilities | 7838 | 9005 |

| Fast Ratio | 0.92 | 1.09 |

Supply: Figures sourced from Air Canada Q3 2019 and Q3 2022 Condensed Consolidated Monetary Statements and Notes. Figures supplied in Canadian {dollars} in hundreds of thousands (besides fast ratio). Fast ratio calculated by creator.

With that being mentioned, whereas Air Canada’s fast ratio has seen an enchancment, the corporate has additionally seen a rise in its long-term debt to whole belongings:

| September 2019 | September 2022 | |

| Lengthy-term debt and lease liabilities | 8116 | 15799 |

| Whole belongings | 27497 | 29754 |

| Lengthy-term debt and lease liabilities to whole belongings ratio | 0.30 | 0.53 |

Supply: Figures sourced from Air Canada Q3 2019 and Q3 2022 Condensed Consolidated Monetary Statements and Notes. Figures supplied in Canadian {dollars} in hundreds of thousands (besides long-term debt and lease liabilities to whole belongings ratio). Lengthy-term debt and lease liabilities to whole belongings ratio calculated by creator.

On this regard, whereas the expansion in income and short-term liquidity is encouraging, I take the view that traders will begin to focus extra on long-term debt metrics going ahead, and search for proof that the corporate will pay down long-term debt masses that have been incurred throughout the pandemic.

Wanting Ahead

Up to now, Air Canada has clearly proven indicators of restoration after journey has began to method pre-pandemic ranges as soon as once more.

Whereas there have been considerations that inflationary pressures might maintain demand decrease – there has not been any explicit proof of this thus far. Whereas there might be a seasonal slowdown in income progress as we method the winter months – I take the view that income progress nonetheless has room to run over the medium and longer-term.

As talked about, there’ll come a degree whereby income progress is now not enough to appease traders, who’re more likely to pay extra consideration as to if the corporate can scale back its long-term debt load, which nonetheless stays elevated in comparison with 2019. As well as, as the corporate nonetheless is working at a web loss – income progress might want to proceed to rise considerably to return the corporate to profitability.

Going ahead, one wish to see a discount in long-term debt, or no less than a discount in long-term debt relative to whole belongings. Ought to we see proof of this going ahead, then I take the view that this might function a catalyst for upside.

Conclusion

To conclude, Air Canada has seen robust income progress as in comparison with final 12 months. With that being mentioned, traders will wish to see additional proof that the corporate can return to profitability and sustainably scale back its long-term debt. As such, I take a “wait and see” method on Air Canada at this time limit.