Annabelle Chih

Thesis

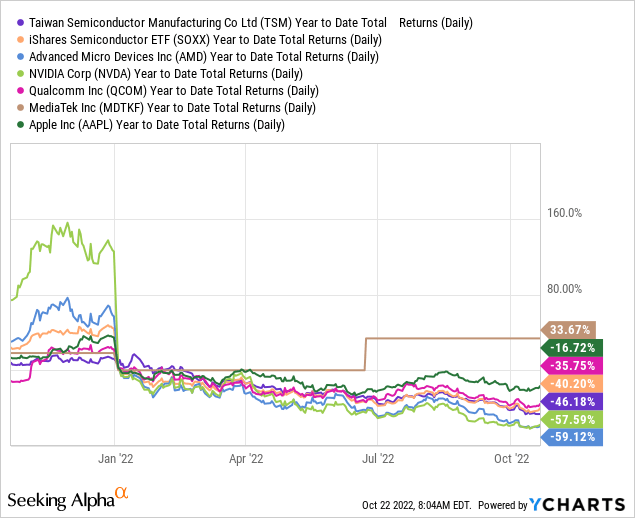

TSMC’s (NYSE:TSM) Q3 launch did not elevate shopping for sentiments, although TSM had been battered in 2022. It posted a YTD whole return of -46.18%, under the Semiconductor ETF’s (SOXX) -40.2% efficiency.

As we defined in our pre-earnings article, we anticipated near-term draw back volatility to proceed. Subsequently, it appears the market stays tentative over a cloth re-rating on TSMC, given the stock digestion in its finish clients. Moreover, we imagine weak export knowledge launched lately by South Korea and Taiwan pointed to a worsening world financial system as buyers parsed the impression on TSMC’s ahead efficiency.

Our evaluation means that TSMC final traded at a big low cost towards its historic averages and in addition its friends. Given its large CapEx enlargement over the previous two years, we imagine the de-rating is justified, because the market must consider additional execution dangers.

Administration highlighted it is assured that it might put up income progress in 2023, whereas the semi trade is anticipated to put up unfavourable progress. Moreover, it burdened that the stock digestion ought to attain its nadir in H1’23 earlier than staging a second-half restoration.

However, TSMC’s visibility is derived from what its clients predict. And its clients’ monitor file of their forecasts for 2022 has been fairly disappointing. Furthermore, apart from Apple (AAPL), which has executed comparatively effectively, AMD (AMD) and NVIDIA (NVDA) have misplaced vital credibility with buyers, given their markedly decrease revisions to steering.

Qualcomm (QCOM) and MediaTek (OTCPK:MDTKF) have additionally confronted challenges of their smartphone phase as progress in China slows additional.

Subsequently, we imagine the market must replicate the dangers of TSMC’s working deleverage given its excessive CapEx necessities, which might markedly impression its working revenue efficiency in 2023.

Nonetheless, our evaluation signifies that the battering in TSMC has created engaging entry ranges for buyers with a long-term focus. We count on the market to proceed demonstrating volatility over the following few months because it attracts in bearish buyers/merchants whereas forcing extra weak TSMC holders to capitulate.

Therefore, buyers are urged to proceed utilizing a dollar-cost averaging method to scale back their allocation/timing dangers.

Accordingly, we reiterate our Purchase score on TSM.

TSMC’s Huge Progress In 2022 Is Set To Finish

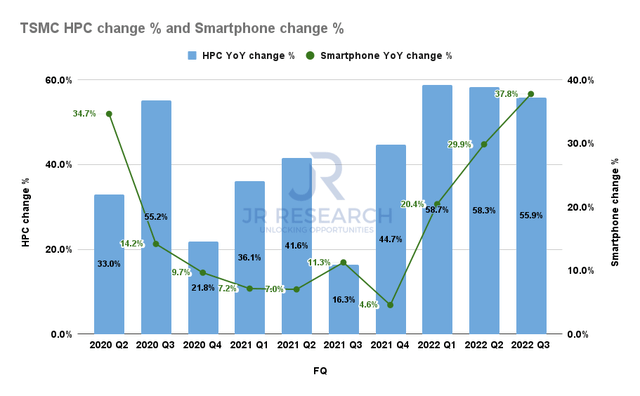

TSMC HPC income change % and Smartphone income change % (Firm filings)

TSMC posted one other strong quarter, as income elevated by 47.9% YoY in Q3. The expansion was broad-based, with its two vital segments, Excessive-performance Computing (HPC) and Smartphone demonstrating strong progress.

As seen above, HPC posted income progress of 55.9%, whereas Smartphone delivered a income enhance of 37.9%. Nonetheless, buyers are reminded that the market is forward-looking. Administration was additionally reticent in issuing 2023 steering, because it’s normally completed in This autumn. Nonetheless, administration highlighted that it expects 2023 to be a “progress 12 months.” TSMC CEO C.C. Wei accentuated:

The continuing stock correction can even have an effect on TSMC. [But,] we count on our enterprise to be much less unstable and extra resilient than the general semiconductor trade throughout this era. Looking forward to 2023, with the profitable ramp-up of N5, N4P, N4X, and the upcoming ramp of N3E, we’ll proceed to broaden our buyer product portfolio and enhance our addressable market. Thus, whereas the continuing semiconductor stock correction will have an effect on our first half 2023 utilization charge, we count on our enterprise to be supported by stronger demand for our differentiated and main superior and specialty applied sciences, and for 2023 to be a progress 12 months for TSMC. (TSMC FQ3’22 earnings name)

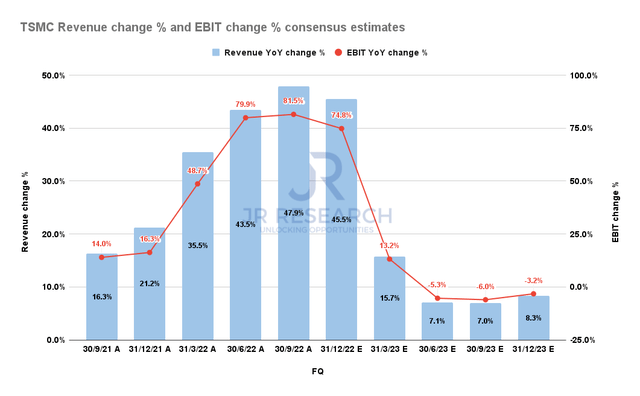

TSMC Income change % and EBIT change % consensus estimates (S&P Cap IQ)

So, it is fairly clear that administration expects its income progress to gradual markedly in 2023. Nonetheless, the consensus estimates (bullish) counsel TSMC remains to be anticipated to put up excessive single-digit income progress by FY23.

Accordingly, TSMC is projected to ship income progress of 8.1% for FY23, although the semi trade is anticipated to put up 0% progress (based on the revised Refinitiv knowledge). Therefore, semi trade analysts might nonetheless be overly optimistic of their forecasts, as TSMC highlighted that “in 2023, nonetheless a progress 12 months for TSMC [but] the general trade in all probability will decline.”

Subsequently, we imagine the market’s present positioning signifies that it thinks the Road analysts may must revise their ahead estimates downward for TSMC.

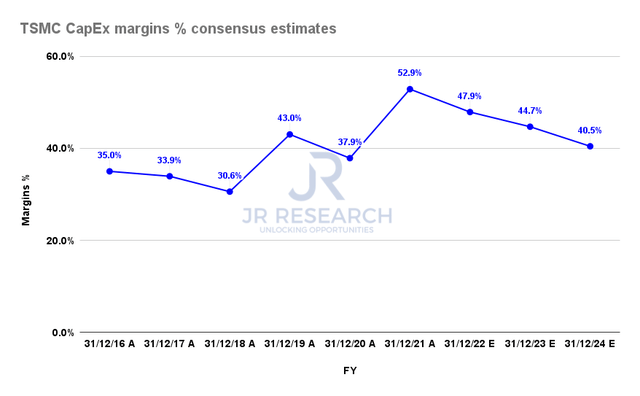

TSMC CapEx margins % consensus estimates (S&P Cap IQ)

Additionally, we gleaned that TSMC’s CapEx margins are nonetheless anticipated to be above its long-run steering of “mid-to-high 30s.” Therefore, TSMC might nonetheless bear an prolonged digestion section that the Road analysts could not have mirrored accordingly.

TSMC’s Valuations Have Been Battered

With this in thoughts, we aren’t stunned that TSMC has underperformed most of its most vital clients and the SOXX YTD in 2022. Apart from the 2 predominant “culprits,” AMD and NVIDIA, which revised their steering markedly, TSMC’s underperformance is kind of gorgeous.

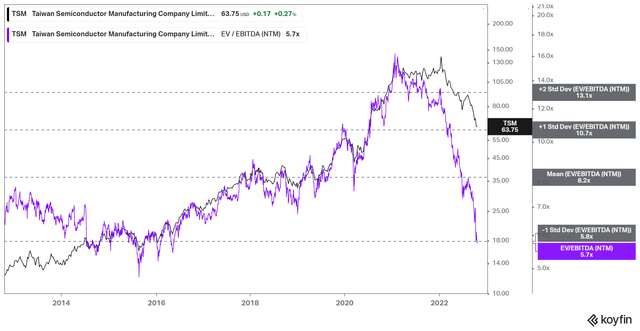

TSM NTM EBITDA multiples valuation pattern (koyfin)

Nonetheless, it is onerous to not get excited figuring out TSM’s EBITDA multiples have collapsed to the 2 customary deviation zone beneath its 10Y imply. Therefore, we postulate that the market has inflicted vital harm in its valuations, presumably anticipating extra draw back dangers to the present consensus estimates.

As such, TSM’s NTM EBITDA a number of of 5.7x can also be effectively under its semi friends’ median a number of of seven.8x (based on S&P Cap IQ knowledge). As well as, its NTM normalized P/E of 10.7x is markedly under the semi trade ahead P/E of 14x and under its SOXX friends’ ahead P/E of 12.9x.

Subsequently, we view TSM’s valuation constructively at these ranges and imagine the reward-to-risk profile has improved tremendously.

Is TSM Inventory A Purchase, Promote, Or Maintain?

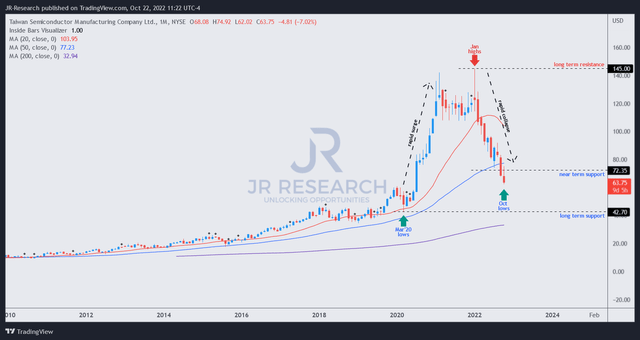

TSM worth chart (weekly) (TradingView)

Regardless of its practically 60% collapse from its January 2022 highs, TSM stays in a long-term uptrend.

However, the market was ruthless within the digestion of its fast surge from its March 2020 COVID lows, because it digested its positive factors all the best way again to ranges final seen in July 2020.

Subsequently, the fast selloff from its January bull lure highs has probably impacted the conviction of weak palms who purchased close to these ranges, chucking up the sponge on the best way down.

The draw back break of its June lows was additionally vital, as patrons who utilized cease losses near its 50-month shifting common have probably been taken out. Nonetheless, the extent of its selldown is emblematic of a transfer to drive weak holders to surrender. Regardless of that, we nonetheless want a validated bullish reversal to type on its long-term chart over the following two to 3 months, which is vital to sustaining its long-term bullish bias.

Given its engaging valuation and extremely pessimistic sentiments, we’re assured of the reward-to-risk profile of its present ranges. As such, we reiterate our Purchase score on TSM.