DragonImages

The fifth bear market rally could also be underway.

CNBC

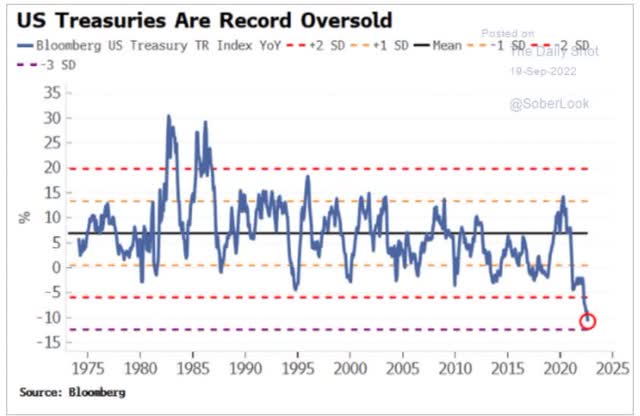

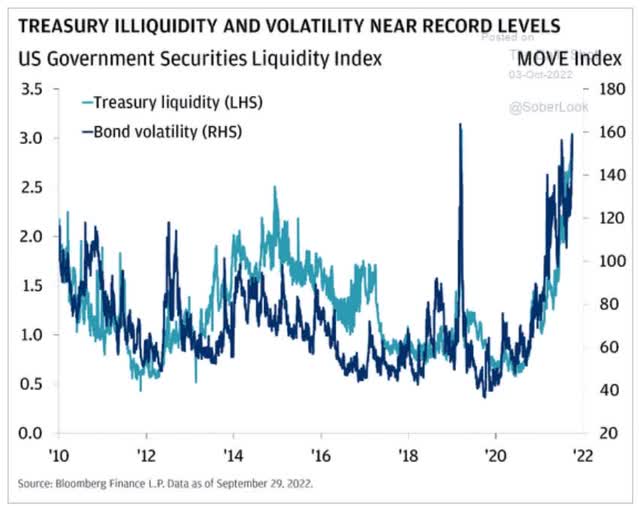

The inventory market is up about 4% within the final two days, more than likely a short-term aid rally brought on by bonds being essentially the most oversold in latest historical past.

Day by day Shot

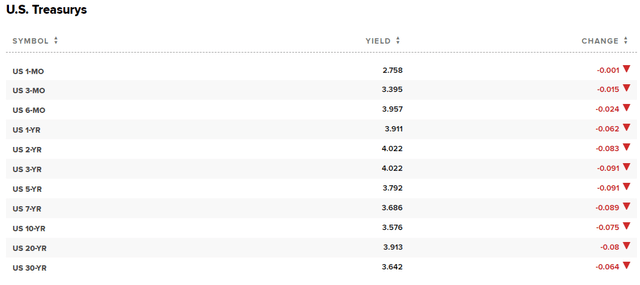

Quick-term US treasuries have a tendency to trace the Fed, so these are more than likely to maintain rising till the Fed pauses.

CME Group

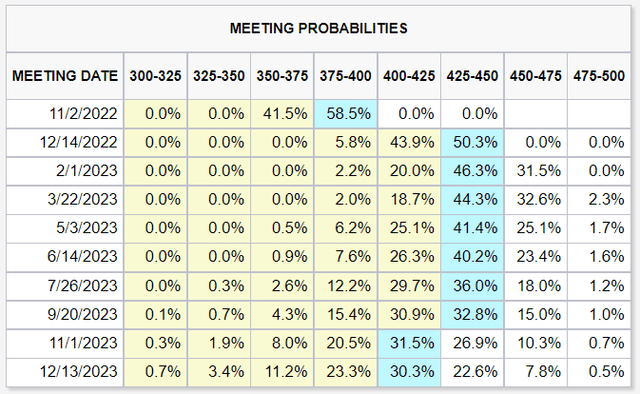

The bond market now thinks the Fed seemingly will pause at 4.25% moderately than 4.5% because the Fed’s dot plot forecast says.

That is moderately speculative, given a number of key details.

- There’s a 9 to 12 month between Fed hikes and financial affect

- thus slower progress (particularly within the jobs market) may now present up till Q1 2023

- 280K internet jobs are anticipated for Friday’s job report

- 200K to 390K vary

The NY Fed estimates 115K internet month-to-month jobs is important to maintain up with inhabitants progress. Based on Bloomberg, Toronto-Dominion, one of the crucial correct economist groups on earth, thinks the Fed will not contemplate pausing early except US jobs creation is underneath 100K per thirty days.

And TD says the Fed MIGHT pause early if the labor market weakens that a lot. Cleveland Fed President Mester stated final week that the Fed will not be deterred by recession alone.

Vice Chairman Brainard stated that the one factor that may trigger an early pause is monetary instability.

NY Fed

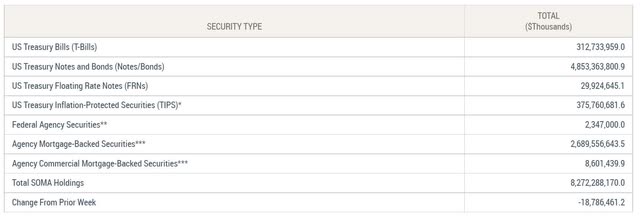

The Fed’s historic mega-QT is accelerating on schedule, now as much as $19 billion per week. By November it will likely be at its full $95 billion month-to-month energy.

Day by day Shot

QT is designed to suck liquidity out of the financial system, and it is actually doing that, particularly within the US treasury market.

However let’s not neglect what Fed Chair Powell stated at the newest press convention.

- the Fed plans to hike above core inflation (PCE).

- after which pause till core inflation falls “at the very least 1%” under the height Fed funds price

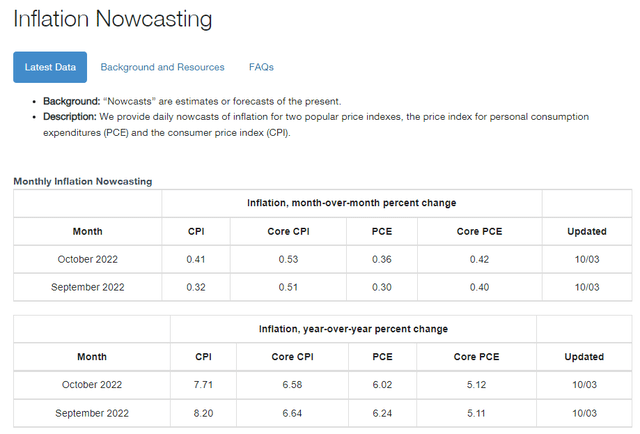

So what’s taking place with core inflation?

Cleveland Fed

The Cleveland Fed’s inflation mannequin now thinks core inflation will get caught at 5.1%, at the very least for the following two months.

With housing 40% of core inflation, and never anticipated to peak (within the month-to-month inflation stories) till January to June 2023, it is attainable that core inflation stays sticky round 5%.

This implies the Fed would seemingly hike to five.25% earlier than pausing and take short-term bond yields to round 4.75% to five% as properly.

The excellent news is that short-term bonds have such low period that in the event you personal 2-year yields (like SHY) a 1% enhance in yields = a couple of 2% lower in value.

Lengthy bonds aren’t anticipated to rise practically as a lot, particularly as soon as the financial system actually exhibits indicators of weakening, which is predicted within the 1st half of 2023.

What does all this imply for rates of interest and the inventory market within the short-term?

- the Fed is much from accomplished

- bonds are seemingly experiencing a short-term aid rally

- and so are shares

- the fifth bear market rally of this bear market

- Bloomberg thinks it could possibly be a 5% to 10% rally earlier than it fades

Or to place it one other means:

Now this isn’t the tip. It’s not even the start of the tip. However it’s, maybe, the tip of the start.” – Winston Churchill

As Morgan Stanley’s Chief Funding Officer Mike Wilson explains, this bear market seemingly has two phases.

- inflation spike/Fed price hike scare section

- recession/progress scare section

2022 to date has been all section one, with valuations coming down however earnings expectations remaining robust.

In 2023 we’re prone to see the cumulative impact of the 4.25% value of price hikes the Fed is planning, plus a bit extra in February or March.

As Mike Wilson stated not too long ago on Bloomberg, with reference to falling bond yields:

That mild on the finish of the tunnel you see is definitely an oncoming freight practice”.

I do not imply to scare you or anybody out of proudly owning shares. My objective is to tell you of what is more than likely to occur subsequent with rates of interest and the financial system, so you possibly can keep away from being shocked by what’s coming subsequent.

No person can predict rates of interest, the long run path of the financial system or the inventory market. Dismiss all such forecasts and focus on what’s really taking place to the businesses during which you’ve invested.”— Peter Lynch

I like finding out what’s taking place with the financial system, however not for market timing functions. In case you perceive what’s LIKELY to occur, you might be higher ready to experience out inevitable market storms and even revenue from bear market blue-chip bargains.

Why not simply promote all the things now if shares might fall decrease over the following six to 12 months?

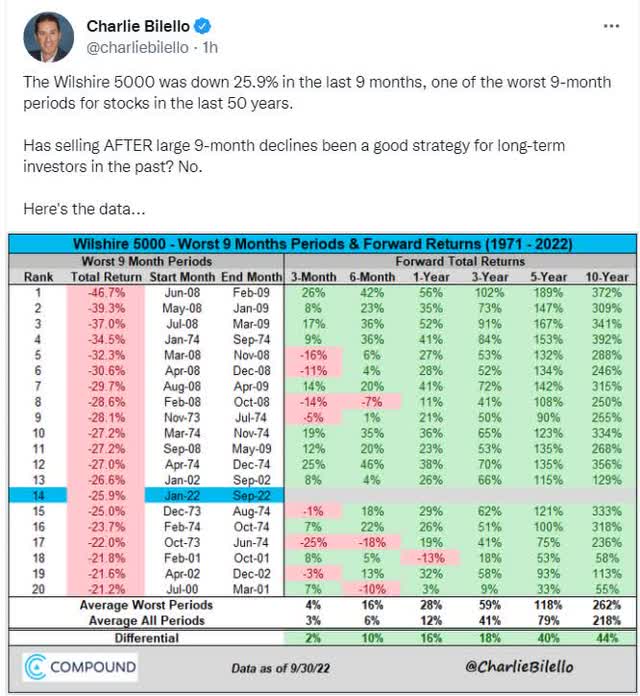

Charlie Bilello

As a result of we have simply been via the 14th worst bear market in historical past, promoting now has at all times been a mistake for anybody with a 3+ 12 months time horizon, together with the stagflation hell of the Nineteen Seventies.

Until you suppose we’re within the literal apocalypse, then this time is prone to show no totally different.

So what do you have to do for the following six to 12 months, which is how lengthy Morgan Stanley thinks it can take for the market to actually backside?

- give attention to security and high quality first, and prudent valuation and sound danger administration at all times

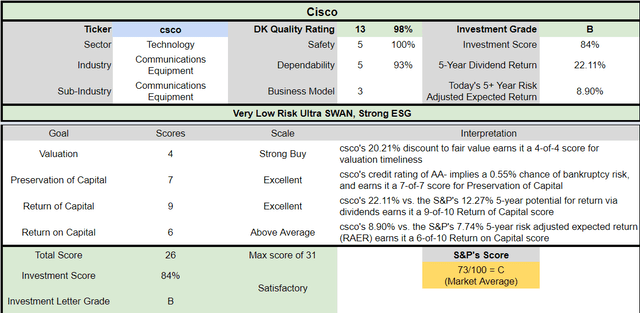

That is why right now I might like to offer an replace that Dividend Kings members have requested about Cisco (NASDAQ:CSCO), certainly one of our favourite tech utility Extremely SWANs (sleep properly at evening).

Let me present you why Cisco is a doubtlessly robust purchase right now, even with that potential “recession freight practice” barreling in the direction of us.

However simply as importantly, I need to present you why T. Rowe Value (TROW) and British American Tobacco (BTI) are two higher-yielding and faster-growing dividend aristocrat alternate options to CSCO.

Ones which may provide help to generate extra very secure earnings and superior long-term returns, whereas serving to you sleep properly at evening throughout the ultimate section of this bear market.

And as soon as the following bull market begins, might provide help to earn outsized income on the highway to retiring in security and splendor within the coming many years.

Why Cisco Is A Probably Robust Purchase Right this moment

Additional Studying

- Cisco: One Of The World’s Biggest Dividend Shares Is On Sale

- a full deep dive on Cisco’s funding thesis, progress outlook, danger profile, valuation, and complete return potential

Funding Thesis On Cisco

We view Cisco Methods because the dominant drive in enterprise networking and count on it to retain its energy in each legacy and future networks. Cisco holds main market shares throughout switching, routing, and wi-fi entry, with robust complementary positions in safety and collaboration. We consider Cisco’s portfolio is positioned appropriately to profit from traits towards hybrid work and cloud environments. It presents essentially the most complete suite of capabilities throughout converging networking and safety markets, and we deem its intertwined merchandise as sticky and worthy of a large financial moat.” – Morningstar

Cisco is a tech utility with a comparatively recession-resistant enterprise mannequin.

- throughout the pandemic, earnings grew by 2%

- throughout the Nice Recession, earnings grew by 9%

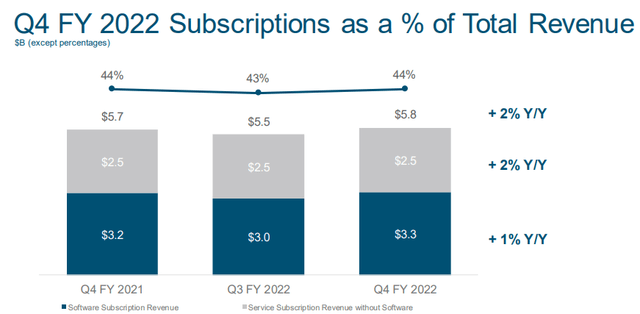

What makes Cisco so particular? Merely put, its clients are a few of the world’s largest and richest corporations. Cisco can be transitioning to a subscription-based enterprise mannequin.

earnings presentation

44% of gross sales at the moment are recurring income, based mostly on contracts starting from three to seven years.

Cisco has loads of rivals in fact, together with white field choices however its vast moat and wealthy margins are a testomony to its “one-stop-shop” suite of enterprise choices.

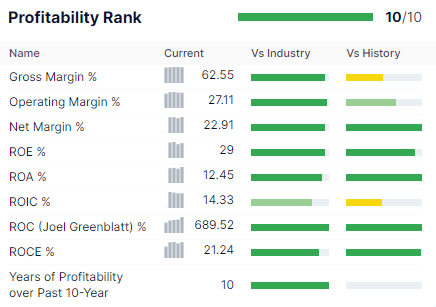

Gurufocus Premium

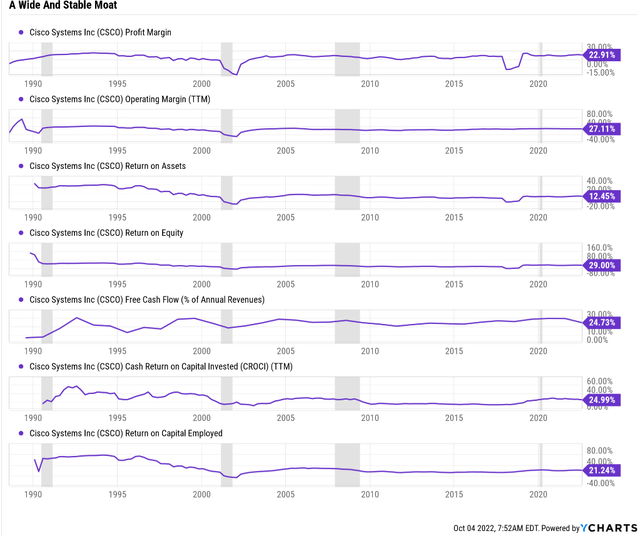

CSCO’s profitability is traditionally within the prime 5% of friends. That is not only a vast moat; that is a really vast moat. One which’s comparatively secure over time.

YCharts

Cisco’s free money movement margins are 25%, larger than Apple’s (AAPL). Its internet margins are 23%, and its money return on invested capital is a Buffett-like 25%.

Gurufocus Premium

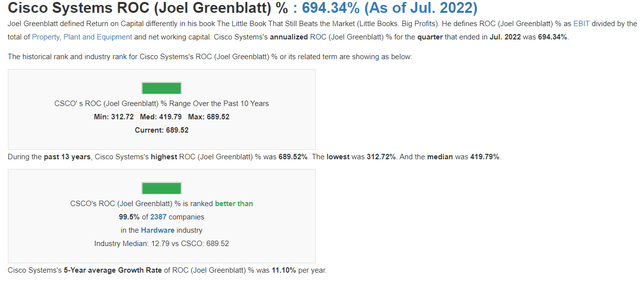

Cisco is producing nearly 700% returns on capital, or ROC.

- annual pre-tax revenue/the price of operating the enterprise

- Joel Greenblatt’s gold normal of high quality and moatiness

For context, the S&P 500’s ROC is 14.6%, the dividend aristocrats 105%, and the median for this trade is 12.8%.

CSCO’s ROC has been trending larger for nearly 30 years, confirming its moat’s secure. Its 13-year median ROC of 420% is unbelievable; over the past 5 years, ROC has been rising by 11% yearly.

Principally, Cisco is a gloriously worthwhile enterprise that mints money and has confirmed very dividend pleasant with its 11-year dividend progress streak, together with throughout the Pandemic.

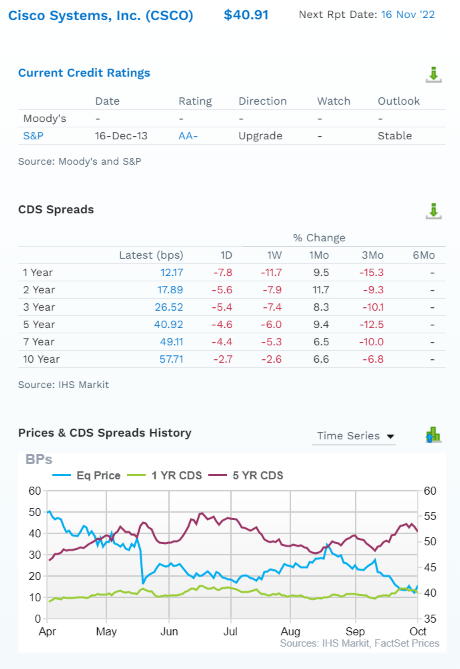

(Supply: FactSet Analysis Terminal)

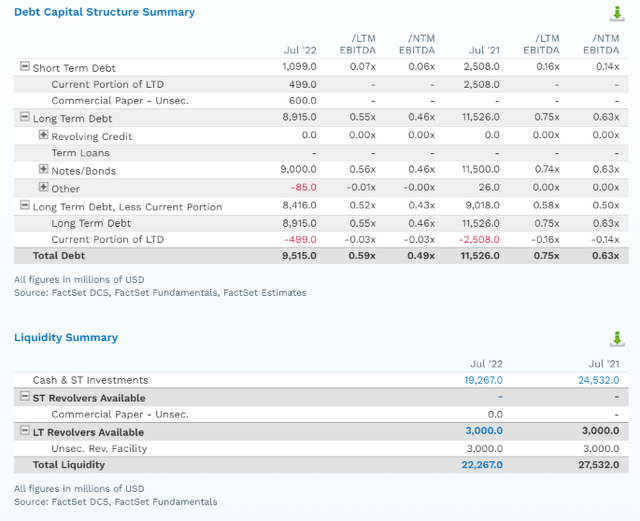

That is an AA-rated firm with a 0.55% 30-year chapter danger, in line with S&P. The bond market believes CSCO’s basic danger has been falling modestly in the previous couple of months.

(Supply: FactSet Analysis Terminal)

CSCO has $10 billion additional cash than debt, and its debt/EBITDA is 0.6X on its approach to 0.5X within the subsequent 12 months.

- 3.0X or much less internet debt/EBITDA is secure for this trade in line with ranking businesses

CSCO’s working income cowl its curiosity prices nearly 40X over, 5X greater than the curiosity protection ratio of 8 ranking businesses contemplate secure.

Its common borrowing prices are 3.9%, or simply 1.6% adjusted for long-term inflation, nearly 16X lower than its money return on invested capital.

(Supply: FactSet Analysis Terminal)

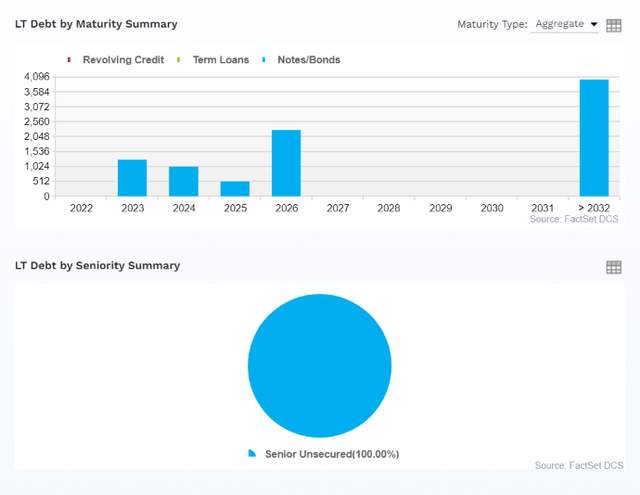

CSCO’s debt is properly staggered and 100% unsecured for optimum monetary flexibility.

This can be a fortress steadiness sheet which signifies that Cisco’s dividend could be very secure.

- excellent 100% security rating

- 0.5% common recession dividend minimize danger

- 1% extreme recession dividend minimize danger

(Supply: FactSet Analysis Terminal)

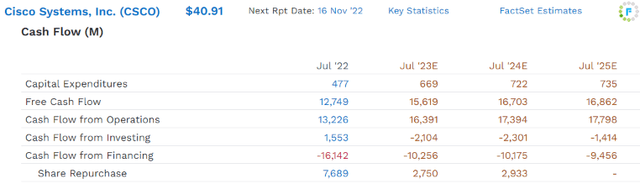

CSCO is producing slowly however steadily rising free money movement annually to pay its $6.25 billion in dividends.

- 41% FCF payout ratio consensus for 2023

- Vs. 60% secure in line with ranking businesses

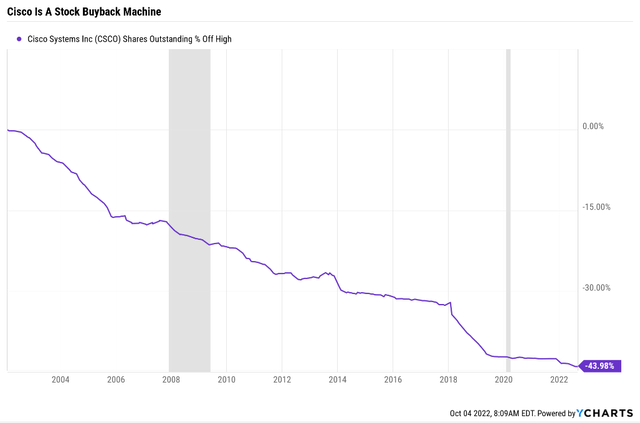

Cisco is not shopping for again that a lot inventory proper now, nevertheless it has the fortress steadiness sheet to purchase again inventory at a price of about 2% per 12 months.

Charts

Since 2003 Cisco has repurchased 44% of its internet shares, often at cheap to very engaging valuations.

(Supply: FactSet Analysis Terminal)

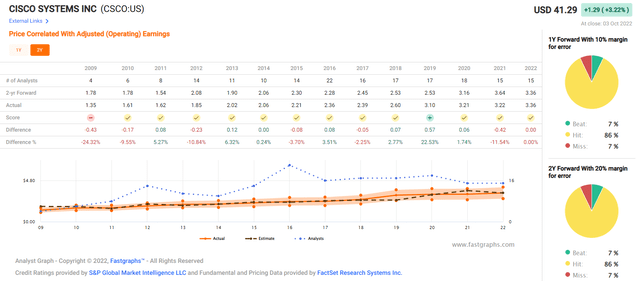

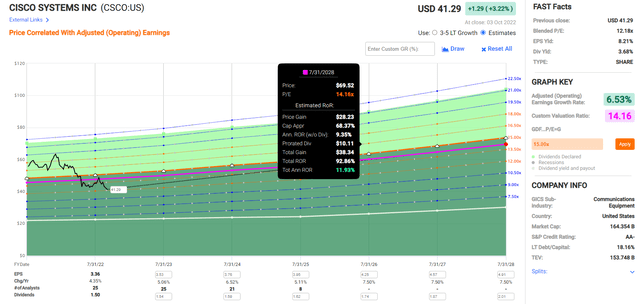

Analysts count on 7.5% CAGR long-term progress from Cisco, and this enterprise is so secure that margins of error are usually small.

FAST Graphs, FactSet

What do a really secure 3.7% yield and seven.5% CAGR progress imply for long-term traders?

| Funding Technique | Yield | LT Consensus Development | LT Consensus Whole Return Potential | Lengthy-Time period Danger-Adjusted Anticipated Return | Lengthy-Time period Inflation And Danger-Adjusted Anticipated Returns | Years To Double Your Inflation & Danger-Adjusted Wealth |

10-Yr Inflation And Danger-Adjusted Anticipated Return |

| REITs | 3.9% | 6.1% | 10.0% | 7.0% | 4.7% | 15.3 | 1.58 |

| Cisco | 3.7% | 7.5% | 11.2% | 7.8% | 5.6% | 13.0 | 1.72 |

| Schwab US Dividend Fairness ETF | 3.6% | 8.80% | 12.4% | 8.7% | 6.4% | 11.3 | 1.86 |

| Dividend Aristocrats | 2.8% | 8.7% | 11.5% | 8.1% | 5.8% | 12.5 | 1.75 |

| S&P 500 | 1.9% | 8.5% | 10.4% | 7.3% | 5.0% | 14.4 | 1.63 |

(Sources: DK Analysis Terminal, FactSet, Morningstar, YCharts)

That evaluation expects CSCO to ship about 11.2% CAGR long-term returns, which is barely higher than the S&P 500 and on par with the dividend aristocrats.

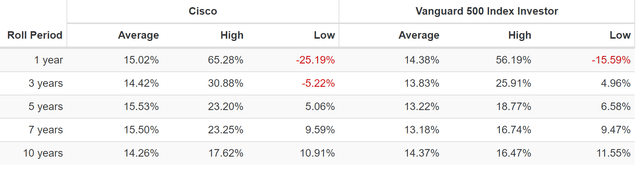

Cisco Rolling Returns Since 2011 (When It Started Paying Dividends)

Portfolio Visualizer Premium

Cisco has confirmed itself a really reliable supply of market matching returns however far superior earnings over time.

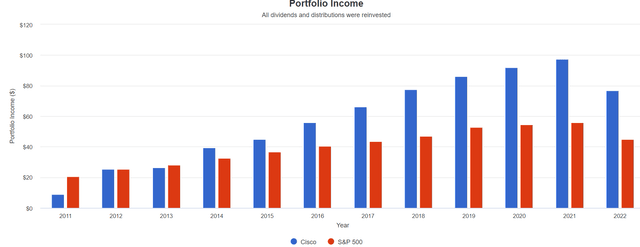

Portfolio Visualizer Premium

Cisco’s earnings progress over the past 11 years has been double that of the S&P 500, a really spectacular 22%.

| Portfolio | 2011 Earnings Per $1000 Funding | 2022 Earnings Per $1000 Funding | Annual Earnings Development | Beginning Yield |

2022 Yield On Value |

| S&P 500 | $21 | $60 | 10.01% | 2.1% | 6.0% |

| Cisco | $12 | $103 | 21.58% | 1.2% | 10.3% |

(Supply: Portfolio Visualizer Premium)

Sooner or later, 7% to eight% dividend progress is probably going, now that the payout ratio has normalized at very secure 40% to 50% ranges.

Cisco 2024 Consensus Whole Return Potential

(Supply: FAST Graphs, FactSet Analysis)

If CSCO grows as anticipated and returns to historic honest worth by 2024, it might ship 46% complete returns, or 14% yearly.

- about 33% greater than the S&P 500

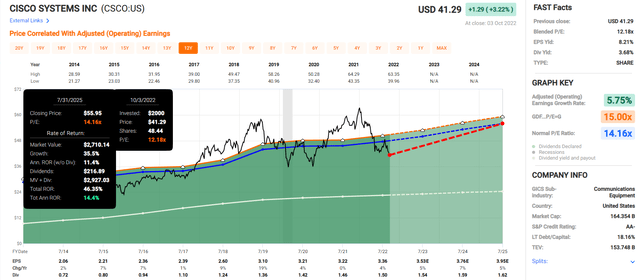

Cisco 2027 Consensus Whole Return Potential

(Supply: FAST Graphs, FactSet Analysis)

If CSCO grows as anticipated over the following 5 years (it nearly at all times does) and returns to historic honest worth, then it might practically double, delivering 12% annual returns.

- about 50% larger complete returns potential than the S&P 500

| Metric | Historic Honest Worth Multiples (12 years) | 2021 | 2022 | 2023 | 2024 |

12-Month Ahead Honest Worth |

| 5-Yr Common Yield | 2.97% | $49.83 | $51.18 | $51.18 | $52.53 | |

| Earnings | 14.10 | $46.25 | $48.36 | $51.18 | $55.84 | |

| Common | $47.97 | $49.73 | $51.18 | $54.13 | $50.59 | |

| Present Value | $41.29 | |||||

|

Low cost To Honest Worth |

13.93% | 16.97% | 19.33% | 23.72% | 18.38% | |

| Upside To Honest Worth | 16.19% | 20.44% | 23.95% | 31.10% | 26.20% | |

| 2022 EPS | 2023 EPS | 2022 Weighted EPS | 2023 Weighted EPS | 12-Month Ahead EPS | 12-Month Common Honest Worth Ahead PE |

Present Ahead PE |

| $3.43 | $3.63 | $0.73 | $2.86 | $3.59 | 14.1 | 11.5 |

(Supply: Dividend Kings Zen Analysis Terminal)

Cisco is about 18% traditionally undervalued and presents as much as 26% essentially justified upside potential over the following 12 months.

It is buying and selling at 11.5X ahead earnings however simply 8.2X cash-adjusted earnings.

- an anti-bubble non-public fairness valuation pricing in -0.6% CAGR progress

Cisco Funding Resolution Rating

DK

(Supply: Dividend Kings Automated Funding Resolution Instrument)

CSCO is a doubtlessly cheap high-yield Extremely SWAN alternative for anybody comfy with its danger profile.

- 3.7% secure yield vs. 1.9% S&P (2X larger and far safer yield)

- 10% larger annual long-term return potential

- comparable risk-adjusted anticipated returns

- 2X the consensus 5-year earnings

However whereas Cisco is a doubtlessly robust purchase right now, there are even higher choices out there, with larger yields, and quicker progress charges, like TROW and BTI.

British American Tobacco: Each The Finest Valuation AND Development Outlook In 20 Years

Additional Studying

- 7% Yielding British American Tobacco Is The Good Bear Market Purchase

- a full deep dive on BTI’s funding thesis, progress outlook, danger profile, valuation, and complete return potential

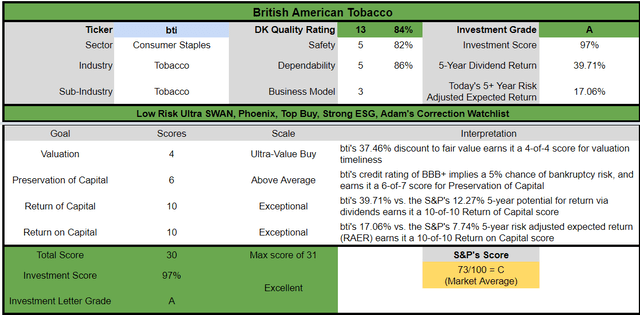

Causes To Probably Purchase British American Right this moment

| Metric | British American Tobacco |

| High quality | 84% 13/13 Extremely SWAN (Sleep Properly At Evening) World Aristocrat |

| Danger Score | Low Danger |

| DK Grasp Record High quality Rating (Out Of 500 Firms) | 166 |

| High quality Percentile | 67% |

| Dividend Development Streak (Years) | 22+ |

| Dividend Yield | 6.8% |

| Payout Security Rating | 82% |

| Common Recession Dividend Lower Danger | 0.5% |

| Extreme Recession Dividend Lower Danger | 1.95% |

| S&P Credit score Score |

BBB+ Detrimental Outlook |

| 30-Yr Chapter Danger | 5.00% |

| Consensus LT Danger-Administration Business Percentile | 72% Good |

| Honest Worth | $60.28 |

| Present Value | $36.59 |

| Low cost To Honest Worth | 39% |

| DK Score |

Probably Extremely Worth, Buffett-style table-pounding robust purchase |

| PE | 7.8 |

| Money-Adjusted PE | 8.2 |

| Development Priced In | -0.6% |

| Historic PE | 13 to 14 |

| LT Development Consensus/Administration Steering | 10.4% |

| PEG Ratio | 0.78 |

| 5-year consensus complete return potential |

23% to twenty-eight% CAGR |

| Base Case 5-year consensus return potential |

24% CAGR (5X higher than the S&P 500) |

| Consensus 12-month complete return forecast | 43% |

| Basically Justified 12-Month Return Potential | 72% |

| LT Consensus Whole Return Potential | 17.2% |

| Inflation-Adjusted Consensus LT Return Potential | 14.9% |

| Consensus 10-Yr Inflation-Adjusted Whole Return Potential (Ignoring Valuation) | 4.01 |

| LT Danger-Adjusted Anticipated Return | 11.44% |

| LT Danger-And Inflation-Adjusted Return Potential | 9.15% |

| Conservative Years To Double | 7.87 Vs. 15.2 S&P 500 |

(Supply: Dividend Kings Zen Analysis Terminal)

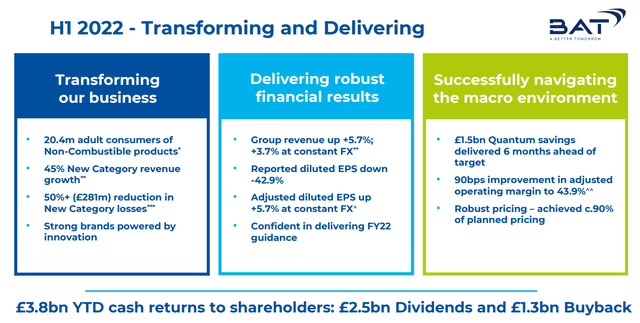

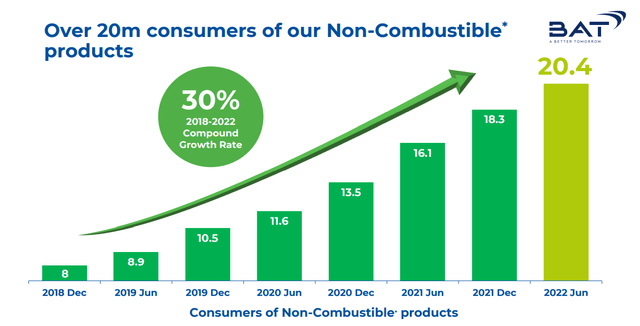

British American Tobacco is properly on its approach to its objective of promoting zero tobacco.

- simply lowered danger nicotine

- and Hashish

(Supply: earnings presentation)

BTI is crushing it with reduced-risk merchandise, posting 45% progress within the first half of 2022, over 50% when adjusting for Ukraine and Russia.

It has over 20 million RRP customers, barely greater than PM has iQOS customers.

(Supply: earnings presentation)

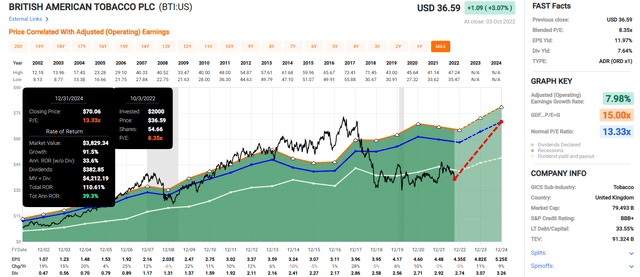

De-leveraging will proceed at a extra gradual tempo as BTI is now shopping for again modest however accelerating quantities of inventory at a few of the finest valuations in 20 years.

FactSet Analysis Terminal

Are you aware what else is at 20-year highs? BTI’s progress outlook which has been rising for the previous 12 months and simply hit 10.4% CAGR.

And have you learnt what else goes up? The British Pound, which bottomed at 1.035 {dollars}/pound and has since recovered to 1.13.

- the annual dividend is 2.17 kilos

- the extra the pound recovers, the upper BTI’s USD dividend climbs

- the pound ought to get better to 1.25 and stay secure as soon as the present disaster is over

- a 7.4% yield

- as soon as the recession within the UK ends, BTI’s normalized yield ought to return to about 8.2%, in line with the FactSet consensus

- 8.9% 2024 yield on right now’s value

That is a dividend that has been raised in native forex yearly since at the very least 2000, a 22+ 12 months dividend progress streak that makes BTI a world aristocrat.

BTI’s dividend coverage is to take care of a 65% EPS payout ratio (vs. 85% secure for this trade, in line with ranking businesses). That is the lowest payout ratio amongst tobacco blue-chips and signifies that the dividend might develop at double-digits long-term.

Principally, BTI represents among the best Buffett-style ultra-value table-pounding fats pitches on Wall Road.

British American 2024 Consensus Whole Return Potential

(FAST Graphs, FactSet Analysis)

BTI’s bear market is the results of a loopy bubble popping. In 2017 BTI grew to become 50% overvalued because of the TINA (there isn’t any various) low price bubble in high-yield dividend shares.

It rapidly crashed and have become 50% undervalued, and the PE has languished at 8 to 9 for 4 years. The Pandemic lockdowns brought on barely damaging progress (as did the robust greenback). However now that BTI’s progress engines are firing on all cylinders, with 21% EPS progress anticipated in 2023 and 2024, the return potential is immense.

110% in two years, or 39% annual returns, are what we’ll get if BTI grows as anticipated and returns to its market-determined honest worth PE of 13.3.

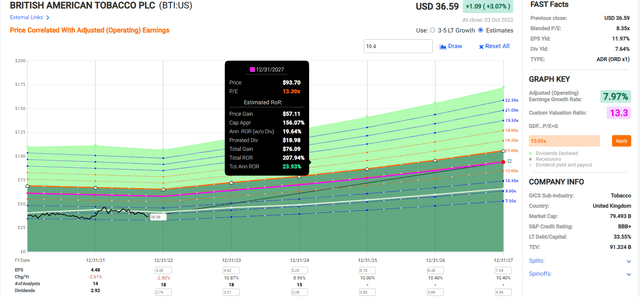

British American 2027 Consensus Whole Return Potential

(FAST Graphs, FactSet Analysis)

Over the following 5 years, BTI might greater than triple, with 24% annual complete returns.

Suppose Buffett-like returns from BTI are not possible?

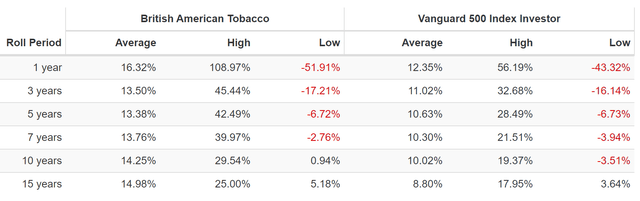

BTI Rolling Returns Since 1985

Portfolio Visualizer Premium

The final time BTI was 50% undervalued, in 2000, it went on to ship 25% annual returns for the following 15 years. By the point it flew off right into a bubble in 2017, it was up 30X from its 2000 lows.

| Funding Technique | Yield | LT Consensus Development | LT Consensus Whole Return Potential | Lengthy-Time period Danger-Adjusted Anticipated Return | Lengthy-Time period Inflation And Danger-Adjusted Anticipated Returns | Years To Double Your Inflation & Danger-Adjusted Wealth |

10-Yr Inflation And Danger-Adjusted Anticipated Return |

| British American Tobacco | 6.8% | 10.4% | 17.2% | 12.0% | 9.8% | 7.4 | 2.54 |

| T. Rowe Value | 4.3% | 12.6% | 16.9% | 11.8% | 9.5% | 7.5 | 2.49 |

| Cisco | 3.7% | 7.5% | 11.2% | 7.8% | 5.6% | 13.0 | 1.72 |

| S&P 500 | 1.9% | 8.5% | 10.4% | 7.3% | 5.0% | 14.4 | 1.63 |

(Sources: DK Analysis Terminal, FactSet, Morningstar, YCharts)

CSCO is prone to modestly beat the market over time. BTI is prone to crush the market, the aristocrats, and even the Nasdaq.

All whereas paying 2X the yield of CSCO, and that is earlier than the British pound even normalizes.

Administration steerage is for 7% to 9% CAGR progress, which, when mixed with the normalized yield of 8.9%, delivers BTI’s distinctive 14% to fifteen% returns for many years to come back.

British American Funding Resolution Rating

DK Dividend Kings Automated Funding Resolution Instrument

BTI is a doubtlessly wonderful ultra-yield Extremely SWAN aristocrat alternative for anybody comfy with its danger profile.

- 6.8% secure yield vs. 1.9% S&P (3.6X larger and far safer yield)

- 70% larger annual long-term return potential

- 2.5X larger risk-adjusted anticipated returns

- 3.5X the consensus 5-year earnings

In comparison with both CSCO or the S&P 500, BTI is a transparent winner and certainly one of my favourite suggestions to anybody who does not thoughts the chance profile of the tobacco trade.

- sooner or later, BTI will likely be no extra “evil” than alcohol corporations

T. Rowe Value: Bear Markets Are The Good Time To Purchase The King of Energetic Fund Administration

Additional Studying

- Purchase BlackRock And T. Rowe Value Right this moment, And You will Thank Me Tomorrow

- a deeper have a look at TROW’s funding thesis, progress outlook, danger profile, valuation, and complete return potential

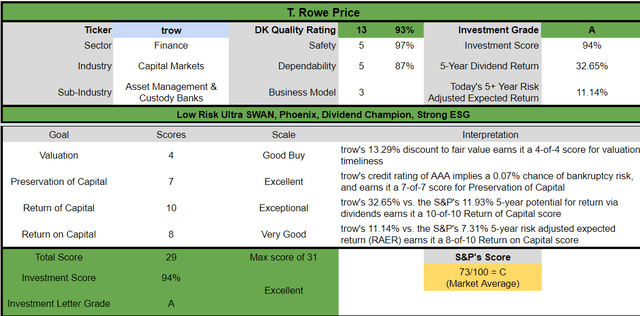

Causes To Probably Purchase T. Rowe Value Right this moment

| Metric | T. Rowe Value |

| High quality | 93% 13/13 Extremely SWAN (Sleep Properly At Evening) Dividend Aristocrat |

| Danger Score | Low Danger |

| DK Grasp Record High quality Rating (Out Of 500 Firms) | 49 |

| High quality Percentile | 90% |

| Dividend Development Streak (Years) | 36 |

| Dividend Yield | 4.3% |

| Dividend Security Rating | 97% |

| Common Recession Dividend Lower Danger | 0.5% |

| Extreme Recession Dividend Lower Danger | 1.15% |

| S&P Credit score Score |

Efficient AAA Outlook (internet money steadiness sheet) |

| 30-Yr Chapter Danger | 0.07% |

| Consensus LT Danger-Administration Business Percentile | 75% Good |

| Honest Worth | $125.62 |

| Present Value | $112.19 |

| Low cost To Honest Worth | 11% |

| DK Score |

Probably Good Purchase |

| PE | 13.5 |

| Money-Adjusted PE | 9.5 |

| Development Priced In | 2.0% |

| Historic PE | 15 to 17 |

| LT Development Consensus/Administration Steering | 12.6% |

| PEG Ratio | 0.75 |

| 5-year consensus complete return potential |

12% to 29% CAGR |

| Base Case 5-year consensus return potential |

15% CAGR (2X the S&P 500) |

| Consensus 12-month complete return forecast | -2% |

| Basically Justified 12-Month Return Potential | 16% |

| LT Consensus Whole Return Potential | 16.9% |

| Inflation-Adjusted Consensus LT Return Potential | 14.6% |

| Consensus 10-Yr Inflation-Adjusted Whole Return Potential (Ignoring Valuation) | 3.91 |

| LT Danger-Adjusted Anticipated Return | 11.82% |

| LT Danger-And Inflation-Adjusted Return Potential | 9.53% |

| Conservative Years To Double | 7.55 |

(Supply: Dividend Kings Zen Analysis Terminal)

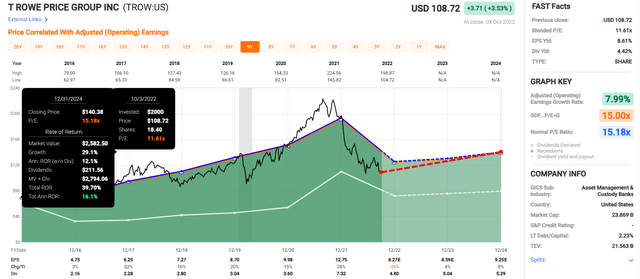

TROW, like many fund managers, is struggling as a consequence of this bear market. However bear markets are exactly the most effective time to purchase asset managers as a result of from bear market lows, life-changing returns comply with.

TROW Rolling Returns Since 1989

(Supply: Portfolio Visualizer Premium)

From bear market lows, TROW delivered as a lot as 39% annual returns for 10 years and 28% annual returns for 15 years.

- 27X return in 10 years

- 41X return in 15 years

TROW at 9.5X cash-adjusted earnings is priced for simply 2% annual long-term progress.

Analysts count on it to really develop at 12.6% CAGR over time.

What in regards to the rise of passive investments?

In an surroundings the place lively fund managers are underneath assault for poor relative efficiency and excessive charges, we consider wide-moat-rated T. Rowe Value is among the finest positioned of the U.S.-based lively asset managers we cowl. The most important differentiators for the agency are the scale and scale of its operations, the energy of its manufacturers, its constant document of lively fund outperformance, and cheap charges. T. Rowe Value has traditionally had a stickier set of shoppers than its friends as properly, with two-thirds of its property underneath administration derived from retirement-based accounts.” – Morningstar

Why is TROW Morningstar’s favourite lively supervisor? As a result of since 1937, they’ve been constantly outperforming their friends.

On the finish of June 2022, 65%, 66%, and 77% of the corporate’s fund AUM have been beating the Morningstar class median on a three-, five-, and 10-year foundation, respectively, with slightly below 50% of fund property closing out the primary half of the 12 months with an total ranking of 4 or 5 stars, higher than simply about each different U.S.-based asset supervisor we cowl.” – Morningstar

77% of its 110 funds beat their friends and benchmark over time, and no fund supervisor has extra 4 or 5-star rated funds than TROW.

TROW’s target-date funds are additionally outperforming their friends and make up 25% of its property underneath administration.

It’s true that TROW’s short-term returns will likely be damage by the truth that constructive fund flows aren’t anticipated till 2024. Because of this, in comparison with 2021’s bull market-led progress, TROW is predicted to expertise barely damaging progress for the following few years.

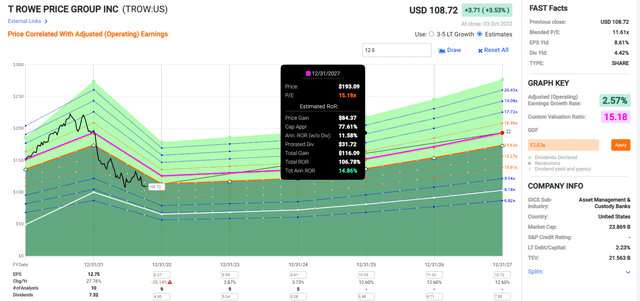

TROW 2024 Consensus Whole Return Potential

(FAST Graphs, FactSet Analysis)

Extra particularly, earnings are anticipated to take a giant hit in 2022, and begin progressively recovering within the following years.

However TROW nonetheless presents the potential for market-beating 16% annual returns and from one of many world’s most secure high-yield dividend progress blue-chips.

TROW 2027 Consensus Whole Return Potential

(FAST Graphs, FactSet Analysis)

Over the following 5 years, TROW might double, delivering strong 15% annual returns.

- about 2X greater than the S&P 500

- barely greater than CSCO

TROW Funding Resolution Rating

DK Dividend Kings Automated Funding Resolution Instrument

TROW is a doubtlessly wonderful high-yield Extremely SWAN aristocrat alternative for anybody comfy with its danger profile.

- 4.3% secure yield vs. 1.9% S&P (2X larger and far safer yield)

- 70% larger annual long-term return potential

- 2X larger risk-adjusted anticipated returns

- 3X the consensus 5-year earnings

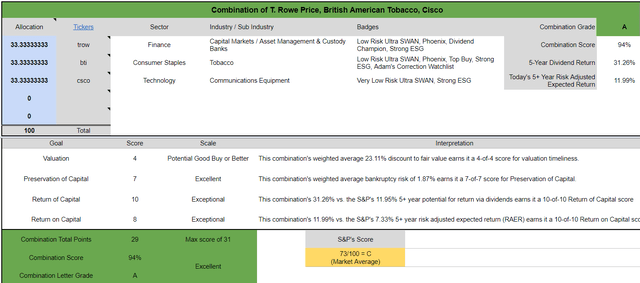

Backside Line: Cisco Is A Robust Purchase, However Contemplate These 2 Quicker Rising Excessive-Yield Dividend Aristocrats

Dividend Kings Automated Funding Resolution Instrument

Cisco is a superb firm, at a strong 18% low cost to honest worth. It is a doubtlessly robust purchase for anybody comfy with its danger profile.

However combining it with BTI and TROW creates a good higher funding, with:

- 4.7% extremely secure yield

- 10.2% CAGR long-term progress consensus

- 14.9% CAGR long-term return potential (historic 16% CAGR)

- A- secure common credit standing

- 23-year common dividend progress streak

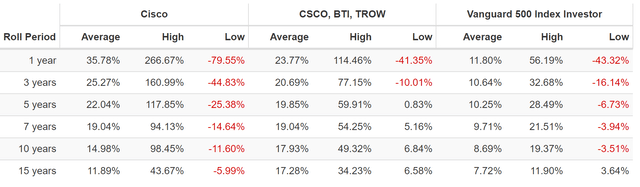

Cisco + British American + T. Rowe Value Since 1990

Portfolio Visualizer Premium

Higher returns, safer dividends, and far more constant returns.

That is the facility of mixing world-beater blue-chips on this bear market.

Every of those is a superb high-yield Extremely SWAN, and you may’t go improper with any of them.

Personally, I’d purchase BTI 1st, then TROW 2nd, and CSCO third, however that is my private danger profile.

The purpose is to suppose outdoors the field at any time when contemplating a blue-chip funding.

- Is what I am contemplating shopping for an affordable and prudent funding?

- Are there higher alternate options?

- What blue-chip mixtures can I create that can improve yield right now whereas doubtlessly boosting long-term returns tomorrow?

When you might have the correct watchlist to work with, you by no means have to fret about settling for “adequate” as a result of it is at all times and eternally a market of shares, not a inventory market.

On this bear market, blue-chip bargains are in all places. Deep worth and sky-high margin of security is simple to search out. You possibly can’t swing a lifeless cat with out hitting a doubtlessly life-changing long-term alternative.

That is what I like about my job, bringing you the world’s finest dividend blue-chip concepts, and instructing you discover extra, so you can also make your personal luck on Wall Road.

Whenever you’re centered on security and high quality first, and prudent valuation, and sound risk-management at all times, retiring wealthy, and staying wealthy in retirement just isn’t a matter of luck. It is a matter of time and endurance.