SeregaSibTravel

The cruise traces have, unsurprisingly, been canine since COVID started. There have been durations of hope for the shares, however these have all turned out to be false. Carnival (NYSE:CCL) reported earnings for the third quarter on Friday, and outcomes dissatisfied the market such {that a} inventory that was already very close to its lows of the previous thirty years (!) fell an additional 23%. As we’ll see, even at $7, I nonetheless don’t discover trigger to purchase Carnival.

The final time I coated the inventory, it was buying and selling for $28, and I stated the rally that was ongoing on the time was unsustainable. Shares are down 75% since then, however I don’t assume the inventory has fallen far sufficient but.

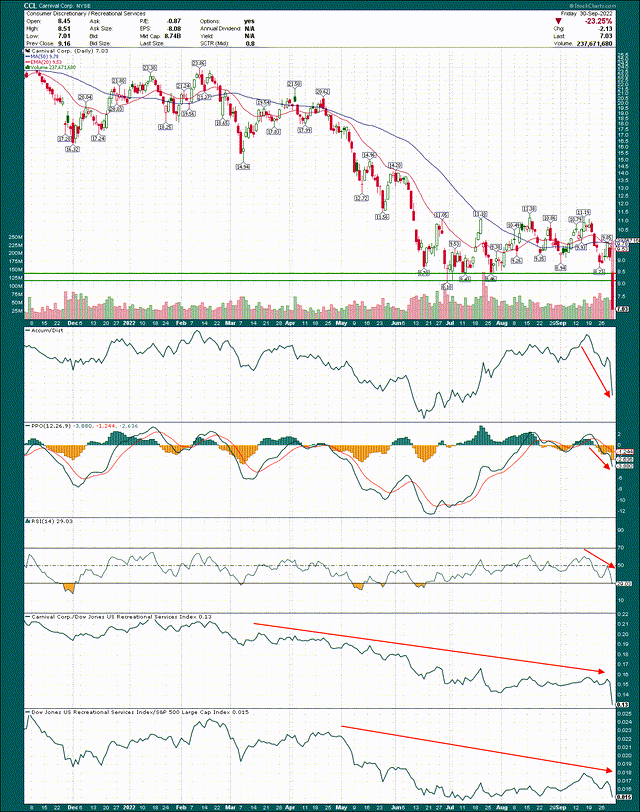

Key assist damaged

We’ll begin with the technical image, and we’ll start with the each day chart. The motion on Friday broke a key assist stage at a time when the indications proceed to weaken, so the ground has disappeared from the inventory as I see it.

StockCharts

The summer season lows produced a zone of assist between $8.10 and $8.40 (roughly) that held a number of instances. Nevertheless, Friday’s selloff was just too intense and the inventory made new lows, and completed on the low of the day. That’s about as bearish because it will get for a day’s buying and selling, and the momentum indicators all proceed to worsen because of this.

The buildup/distribution line plummeted yesterday given the heavy quantity and the truth that the inventory bought off proper to the closing bell. The PPO and 14-day RSIs are headed straight down for the time being, as is relative energy. The inventory may be very weak, in a really weak group, and is underperforming that very weak group. There merely isn’t something to cling to should you’re bullish right here.

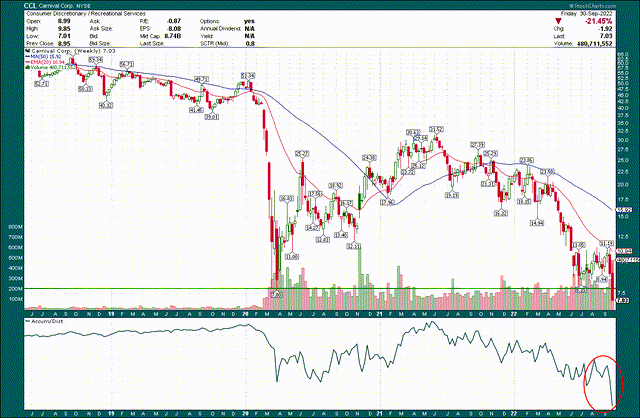

Let’s zoom out to the weekly chart to get an thought of the longer-term image.

StockCharts

We will see, critically, that the inventory simply blasted via the COVID panic low of $7.80 that was set in March of 2020. That low had completely no bearing on buying and selling exercise on Friday, because the bears are utterly in management. The buildup/distribution line made one other low that was far decrease than the prior one, so once more, assist ranges are being ignored and there’s nothing to cling to.

This enterprise is impaired

Income was up virtually 80% sequentially, as Carnival and different operators proceed to get again to some semblance of regular with cruise operations. Carnival is sort of at 100% by way of working capability now, which is an enormous enchancment over the prior a number of quarters. That’s excellent news, but it surely was anticipated, and it’s not sufficient.

Passenger cruise days had been up 55% from Q2, however keep in mind that Q2 had decreased capability. Occupancy was up 15 share factors, hitting 17.7 million passenger cruise days on capability of 21 million. Carnival stated onboard spending was robust in Q3, which is one other good signal, and it hit constructive adjusted EBITDA for the primary time because the pandemic began.

All of that’s positive but it surely was additionally all anticipated. We knew cruise traces had been going to extend capability, we knew passengers would return, and we knew they’d spend whereas onboard. That’s simply getting the enterprise again to regular, however the place it stays an unlimited problem for Carnival is with profitability and financing.

Cruise traces require huge capex yearly, even when no new ships are constructed. Operating cruise ships is ruinously costly so even in good instances, capex for Carnival is billions of {dollars} a yr. The corporate had over a yr of basically no income, which meant financing needed to be completed elsewhere. That “elsewhere” occurred to be big quantities of latest debt and customary share issuances.

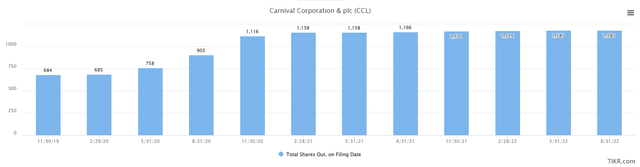

The corporate issued one other $1.15 billion of widespread inventory throughout Q3, utilizing the proceeds to pay down 2023 debt maturities. If this isn’t a sign that this enterprise can not sustainably finance its personal operations, I’m undecided what can be. The corporate additionally exchanged $339 million of convertible debt due 2023 for a similar due in 2024, that means but extra dilution is on the way in which. These further shares might not matter whereas the corporate is making losses, however when income return, every share of inventory excellent could have much less and fewer of every greenback of revenue.

TIKR

We will see the issuances right here, the place the share rely practically doubled from pre-COVID ranges. That’s a big quantity of dilution and what it means is that the corporate must earn about double the amount of cash it did pre-COVID simply to satisfy the identical EPS ranges. It additionally means its skill to proceed to make use of widespread shares as a piggy financial institution is impaired as a result of it’s already completed a number of harm simply to drift the corporate’s working prices throughout COVID.

Wanting forward

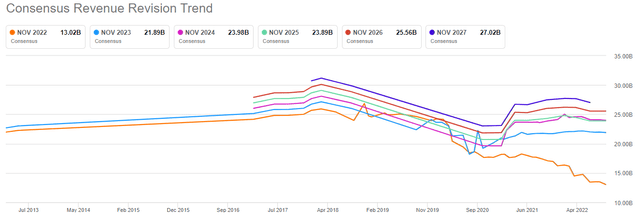

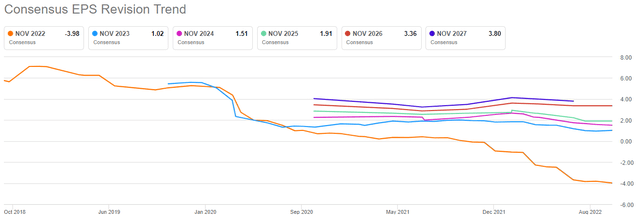

Let’s begin with income revisions as we glance ahead, as they present at the least a little bit of hope for the remaining bulls on Carnival.

Searching for Alpha

This yr’s estimates simply proceed to soften away however in a silver lining, there may be some upward momentum for the out years. Whether or not any of that involves fruition is anybody’s guess, as a result of analysts have been fairly improper on this inventory earlier than. Nevertheless, this might actually be worse. And as I stated above, it’s anticipated that income ought to recuperate strongly as a result of cruise traces are capable of function just about as they did previous to COVID at this level. Until folks simply resolve they don’t like cruises anymore, income will transfer rather a lot greater.

The place issues get dicey for the bulls is with earnings, for lots of the explanations we’ve already mentioned.

Searching for Alpha

There’s no silver lining right here, because the out years are flat-to-down. However as the corporate continues to concern new shares, these estimates have to come back down, given the shares are being issued to easily afford to function; they’re not being issued to finance an acquisition or another progress avenue. It’s simply an additional price to beat, so given the debt and dilution issues Carnival has, I’ve a tough time seeing any upside right here.

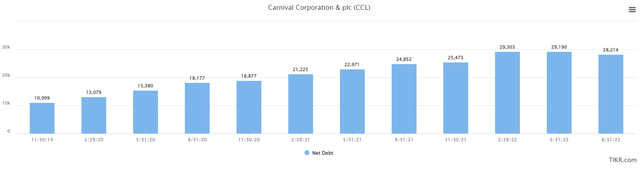

Talking of debt, beneath we have now quarterly excellent internet debt, which takes under consideration money and long-term debt positions.

TIKR

Carnival had a number of debt previous to COVID, as a result of like I stated above, cruise traces are very costly to function, so they have an inclination to have a number of leverage. Carnival’s internet debt load remains to be ~$28 billion, which is an quantity it has no probability to pay again anytime quickly via working income. Annual working revenue was roughly $3.5 billion pre-COVID throughout the perfect of instances. I’ve my doubts it will likely be that prime at any level within the subsequent a number of years given how the corporate’s capital construction has modified, which implies that even when 100% of working income had been devoted to debt discount, it might take years and years simply to get again to pre-COVID ranges of debt.

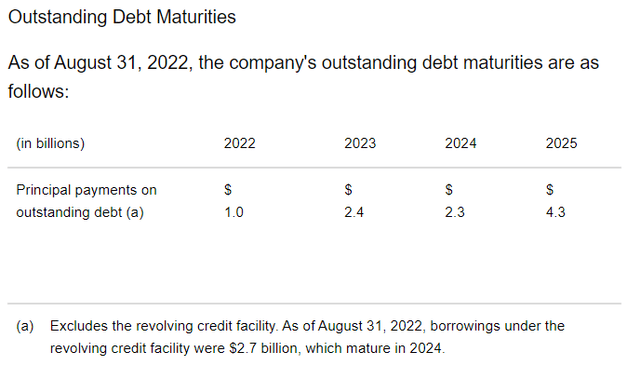

Q3 Earnings Launch

The corporate has the above maturities within the subsequent handful of years, so both these will get reissued at greater charges – in case you hadn’t observed, rates of interest are rather a lot greater as we speak than they’ve been up to now decade – or extra widespread shares will have to be issued. Neither of these is an effective end result for shareholders, however Carnival has no alternative.

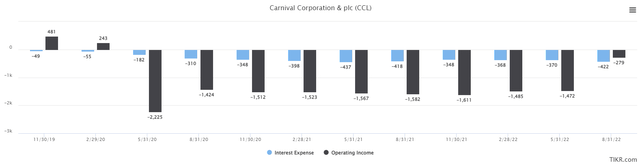

Let’s now flip our consideration to the harm on the earnings assertion from all that debt. Beneath we have now quarterly curiosity expense and working earnings to point out simply how large this downside is.

TIKR

Curiosity expense is within the billions of {dollars} as we speak, with unfavourable working earnings in addition. Whereas working earnings will flip constructive – doubtless subsequent yr – this curiosity price isn’t going wherever. And because the firm reissues maturing debt it can not afford to pay down, it will solely worsen as charges have moved greater.

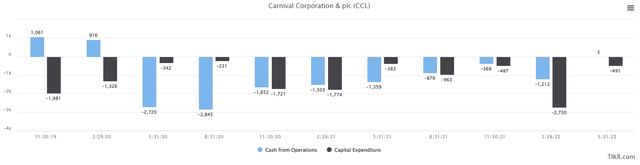

I discussed capex above as properly, which is only one thing more Carnival has to finance. Beneath is quarterly capex and working money circulation as an example this concern.

TIKR

Working money circulation wasn’t even sufficient pre-COVID in some circumstances to cowl capex, however working money circulation has been unfavourable for nearly three years now. Even when it returns to being constructive, capex should compete with curiosity expense and debt discount in methods it by no means did earlier than.

Q3 Earnings Launch

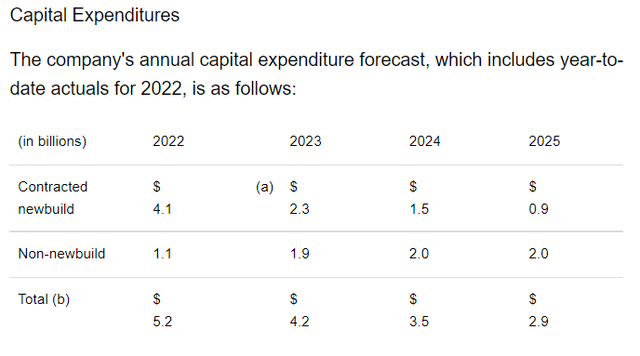

We will see right here the corporate’s resolution is to drastically scale back new builds within the coming years, and whereas that may scale back capex, it has the chance of lowering competitiveness as properly. Clients in leisure actions similar to cruises need the perfect facilities and fashionable designs, and an getting older fleet for Carnival leaves the door open for its rivals.

Let’s worth this factor

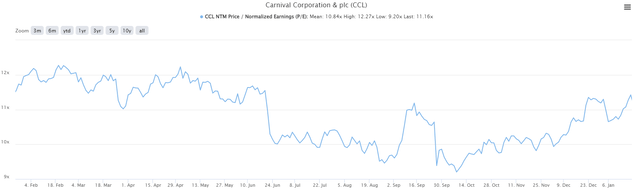

Valuing a inventory with no earnings might be difficult, however let’s begin with Carnival’s pre-COVID valuation. This chart exhibits the yr main as much as COVID, which needs to be fairly consultant of “regular” circumstances.

TIKR

The typical ahead P/E throughout this time was 10.8, with the height at 12.3 and the trough at 9.2. That places us in a fairly great spot to say a standard valuation can be one thing like 10 or 11 instances ahead earnings. Nevertheless, this was earlier than the huge share issuances, earlier than the slashed capex, and earlier than the practically tripling of internet debt. These elements completely warrant a decrease valuation, so my estimate of honest worth is now 7 to eight instances ahead earnings.

Searching for Alpha

If you happen to consider these estimates, the inventory is pretty priced for subsequent yr’s earnings, and low-cost for 2024. Nevertheless, given the elements we mentioned above, I consider the draw back danger of those estimates is far greater than upside danger. I consider that’s what Wall Road informed us on Friday with the huge selloff as properly, and that institutional traders have positioned for decrease estimates through promoting the inventory closely.

The underside line right here is that I nonetheless assume Carnival is an impaired enterprise. It has little to no skill to finance its personal operations, and I don’t know when or if that may change. It has massively diluted shareholders – and continues to – as a result of its stability sheet is already a large number. I merely don’t see any motive to purchase this inventory, significantly since assist ranges on the chart are being ignored. There are such a lot of nice companies on sale as we speak, there may be merely no motive to waste your capital on this one.