SolStock/E+ through Getty Pictures

The central financial institution recreation appears to be dominating the world today.

Within the New York Occasions we learn:

“Shares nose-dived, authorities bond costs plummeted, the pound dipped towards the greenback, oil costs slumped and cryptocurrencies wobbled on Friday as traders, already anxious about rising rates of interest and stubbornly excessive inflation, began quaking on the rising probability of a recession.”

“Their worries grew all through the week as central banks all over the world, from Sweden to Indonesia, as soon as once more wielded their blunt however highly effective tool–interest charge increases–to fight inflation.”

“Additional ones might augur a interval of upper unemployment and slower financial progress.”

“Buyers don’t love that prospect.”

Wow! These darn central banks!

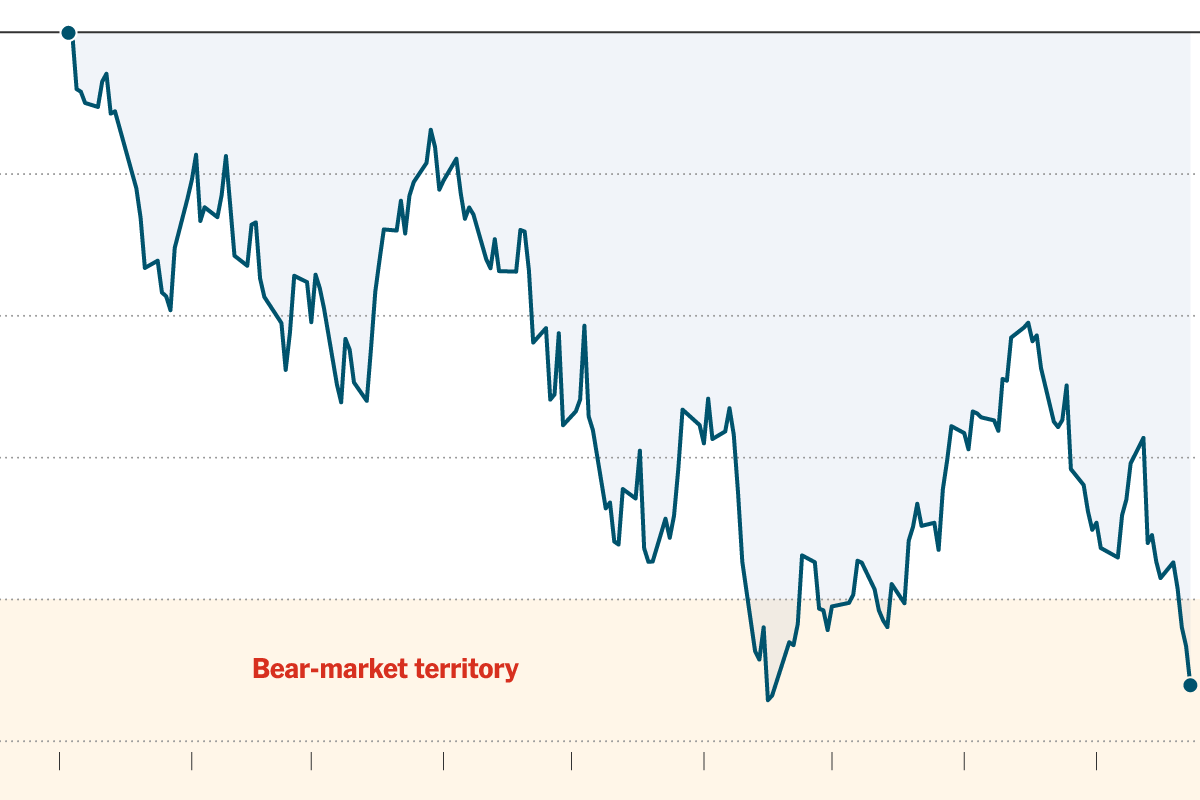

We Are In Bear Market Nation

Guess what?

The inventory market is now in “Bear Market Nation.”

S&P 500 Inventory Index

Proportion Change In S&P 500 since its peak on January 3, 2022

S&P 500 Inventory Index: Proportion Change Since January 3, 2022 (New York Occasions)

The Bear Market kicks in with a 20 p.c discount in value.

So, the sport has expanded. For many of the summer season, the discuss was all concerning the Federal Reserve, what it ought to do, what it should not do, what it was doing, and what it wasn’t doing.

Maybe the largest query needed to do with whether or not or not Fed Chairman Jay Powell was going to place the strain on and preserve the strain on, combatting inflation.

Buyers felt that previously, Mr. Powell all the time appeared to wish to err on the aspect of financial ease in order to not trigger a market drop that will spoil his report.

However, this all passed off when Mr. Powell was overseeing the Federal Reserve’s buy of $120.0 billion in securities monthly so as to add to the Fed’s portfolio.

Mr. Powell needed to guarantee that he was “greater than lined” towards such an error.

This time round, traders are involved that Mr. Powell will once more wish to err on the aspect of financial ease, however on this case, he can be working towards making financial coverage sturdy sufficient to essentially break the again of inflation.

Mr. Powell made use of his August speech on the Jackson Gap convention on financial coverage to attempt to persuade the market that he was, actually, very critical about doing what was essential to cease inflation.

The Fed’s actions since then, together with the 75 foundation level improve within the Fed’s coverage charge of curiosity this previous Wednesday, have helped to persuade traders that he was truly “going to do what was obligatory.”

Properly, Mr. Powell has seemingly satisfied U.S. traders that he’s going to do the job, however he has additionally seemingly satisfied different central banks all over the world that the US could be very critical about combating inflation.

Notice the emphasis that the New York Occasions article talked about above:

“The plan of action wasn’t stunning to traders.”

That’s, traders believed that these central banks had greater than sufficient purpose to lift their coverage charges.

“Quite, it was the pace with which central banks moved this week that despatched them right into a frenzy.”

Ryan Detrick, chief market strategist at Carson Group, is quoted as saying,

“It is a continuation of the troubles we have had all week that world central banks being led by the Fed are climbing charges earlier than we thought to fight inflation and sure leaving charges larger for longer.”

And, as is well-known, the Federal Reserve is anticipated to lift its coverage charge of curiosity once more at its November and December conferences of its Federal Open Market Committee, the group that units the targets for the Federal Funds charge.

Now, these Federal Reserve modifications usually tend to be met with additional will increase within the coverage charges of those different central banks all over the world.

Recession?

Extremely possible!

Additional declines in inventory market costs?

Extremely possible!

The Future

The current…and the long run…are being dominated by what the Federal Reserve…and now, what different central banks all over the world…are going to do sooner or later.

However, the magnitude of the response has modified.

From the sooner concern that the US financial system may drift off right into a recession, now we’ve the prospect of a lot of the Western world drifting off into recessions.

This modifications the image a bit bit.

Do we glance into 2023 and see a worldwide recession?

We do hear discuss what is occurring to grease costs. We hear discuss what may occur in Ukraine. We hear discuss what may occur in Russia. We hear discuss what may occur in China.

However, on the subject of a dialogue about the way forward for the monetary markets, discuss of the Fed comes again to dominate the image.

And, for a change, it seems as if ALL of the central banks appear to be shifting in the identical course. To struggle inflation.

That is a reasonably clear image that’s creating.

What sort of an image can we draw from this for the inventory market?