HJBC

The Thesis

Wall Road’s turn into far too sharp over time, and fairly good at pricing within the cyclicality of earnings. A lot so, that they could have overdone it with commodity firms like TTE, which now trades at 7.4x our estimate of normalized earnings. The mantra on the road for many years has been to purchase when earnings are close to zero and promote once they’re rocketing up. However, we predict the higher strategy is to take the mentality of a enterprise proprietor. Ask your self, “What is the common amount of money I can anticipate from this enterprise over the subsequent 10 to twenty years?” And, “Am I proud of these returns?” This mentality led Warren Buffett to outperform the marketplace for the higher a part of the previous 60 years. What’s extra fascinating is that Warren Buffett’s been shopping for oil shares like Chevron (CVX) from those self same Wall Road merchants. And, much more so, which you could purchase a superior enterprise in TotalEnergies (NYSE:TTE) at an nearly 50% low cost to Chevron.

Within the decade forward, we mission huge returns of 15% each year.

TTE Is Exceptionally Low cost

TotalEnergies has a robust steadiness sheet, with an funding grade bond ranking, manageable long-term debt, and $27 billion of working capital. Such an organization can return lots of money to shareholders.

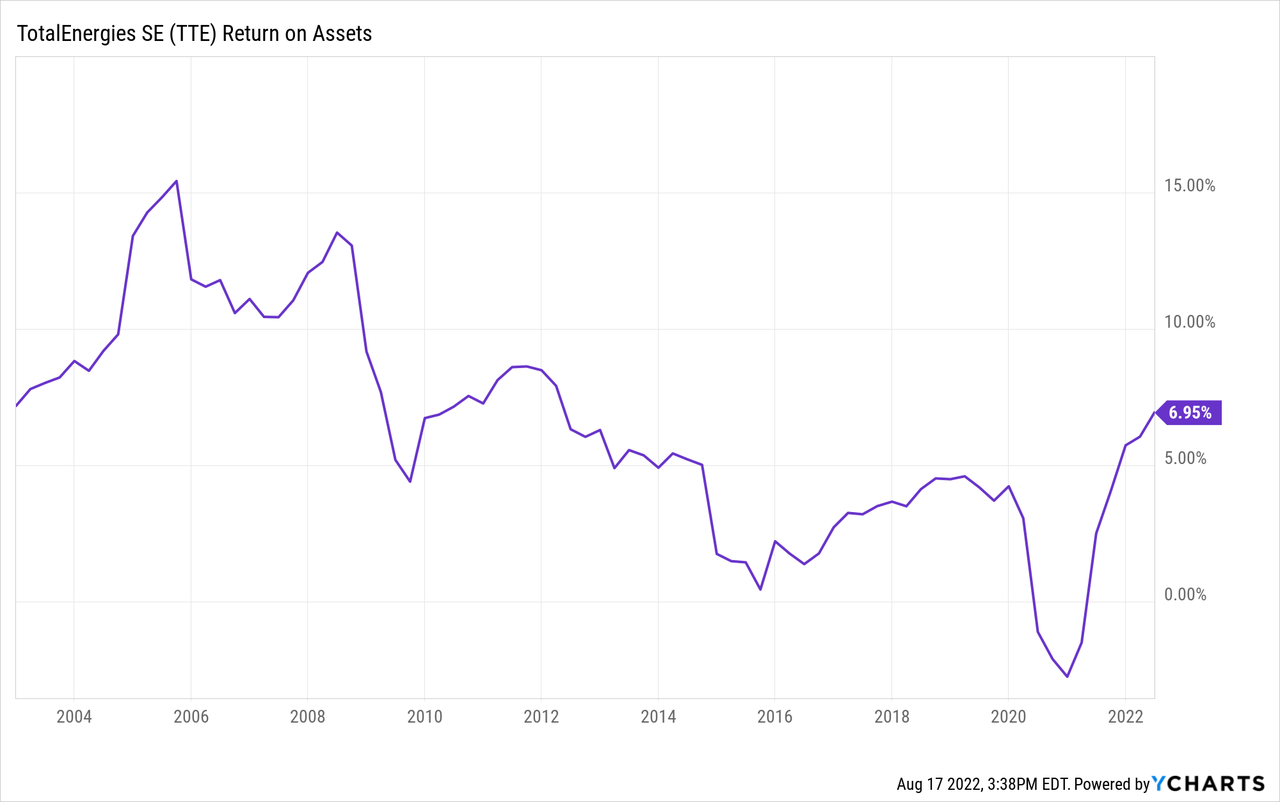

To normalize TTE’s earnings, we checked out how a lot it earns with Brent Crude at $75 per barrel. We additionally studied its common return on belongings and revenue margins. TotalEnergies’ normalized earnings got here in round $18.3 billion ($7.15 per share). This provides TTE a normalized PE of seven.4.

Trying on the ahead PE, value to e book, and free money circulation yield, Whole presents a few 45% low cost to Chevron:

| As of Aug 17, 2022 | Chevron (CVX) | TotalEnergies (TTE) |

| Ahead P/E | 8.8 | 4.9 |

| Value to E-book | 2.0 | 1.2 |

| Free Money Move Yield | 9.8% | 18.2% |

| Dividend Yield | 3.6% | 5.3% |

| Working Capital | $12 Billion | $27 Billion |

Operational Excellence

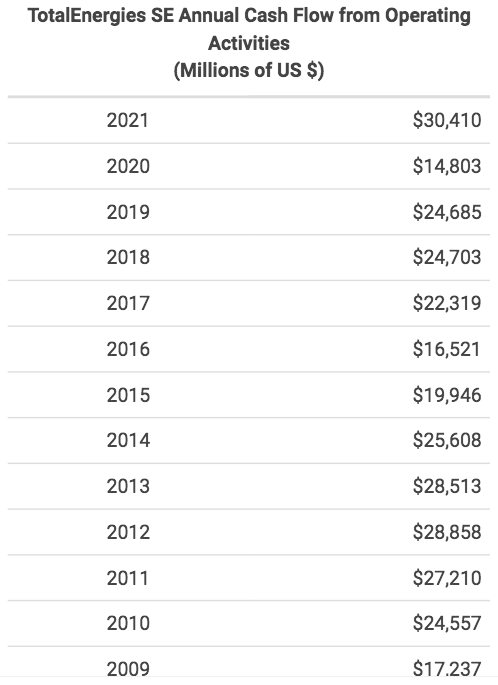

Whole Energies has a robust built-in mannequin with each upstream and downstream power. Which means the subsequent time oil collapses, you possibly can rely on Whole’s LNG, refining, and chemical compounds enterprise to hold you thru. Regardless of a tricky pricing surroundings from 2014 to 2020, Whole continued to rack within the money flows by means of thick and skinny:

TTE’s Working Money Move (Macrotrends)

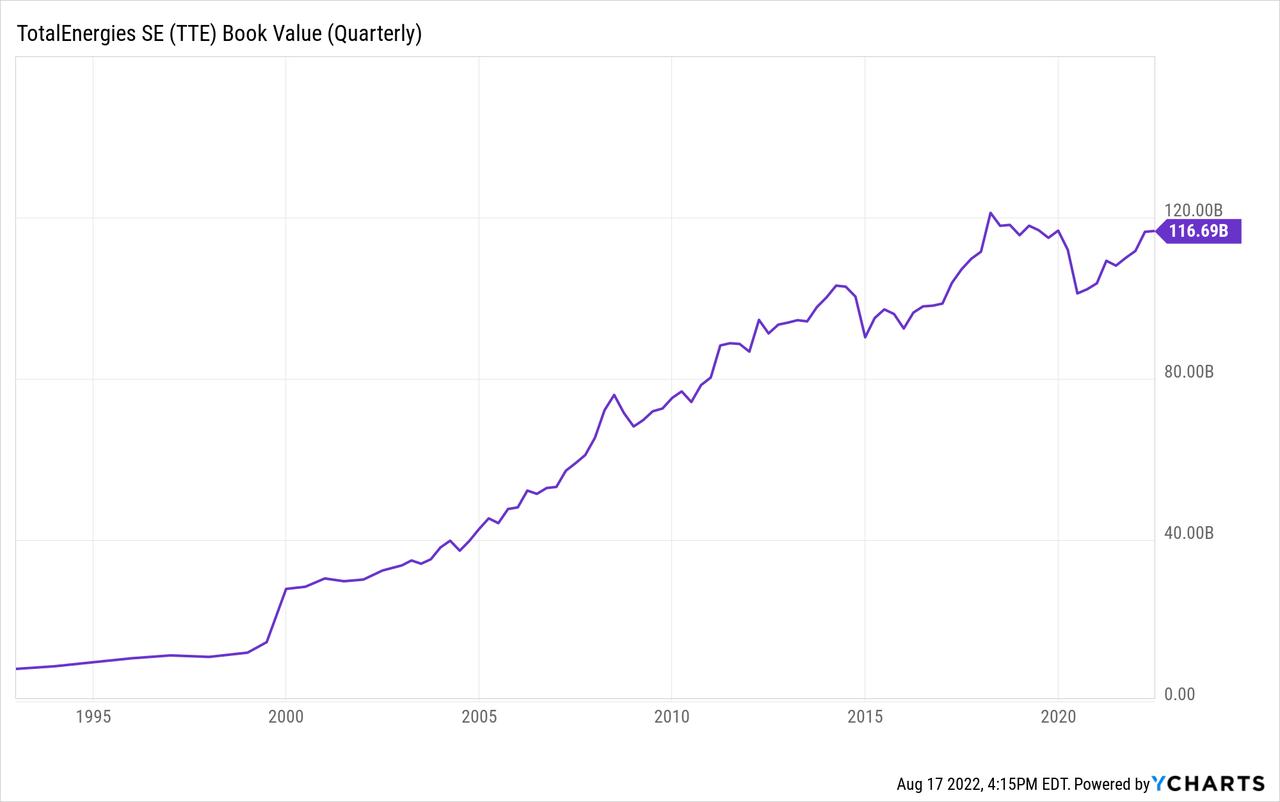

TotalEnergies has an incredible observe report of rising shareholder’s fairness over the long-term:

The Hyper-Development Of Renewables

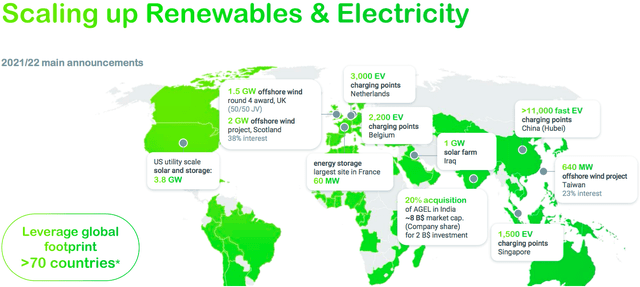

Administration is doing an distinctive job with Whole’s built-in fuel and renewables enterprise. The section’s income grew by 29% each year over the previous two years. And, working earnings within the section grew 68% each year. That is what excites us about TTE’s future. Whole is concerned in wind, photo voltaic, EV charging, inexperienced hydrogen, you title it.

International Participant In Inexperienced Vitality (TotalEnergies)

Whole’s Aggressive Benefit

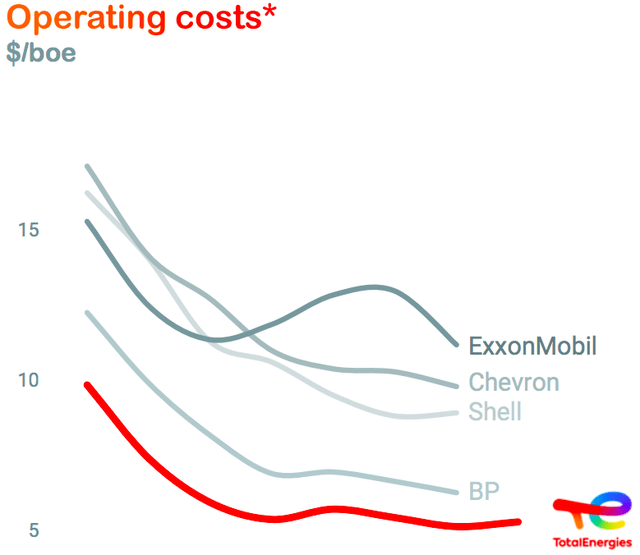

Administration at Whole claims to have business main break-even costs and prices with regards to producing a barrel of oil. If that is true, TTE shareholders personal a number of the world’s premium oil and fuel belongings. This is a chunk from the businesses’ 2021 outcomes, evaluating its working prices to friends:

Working Prices Per Barrel Of Oil (TotalEnergies)

There’s All the time Danger

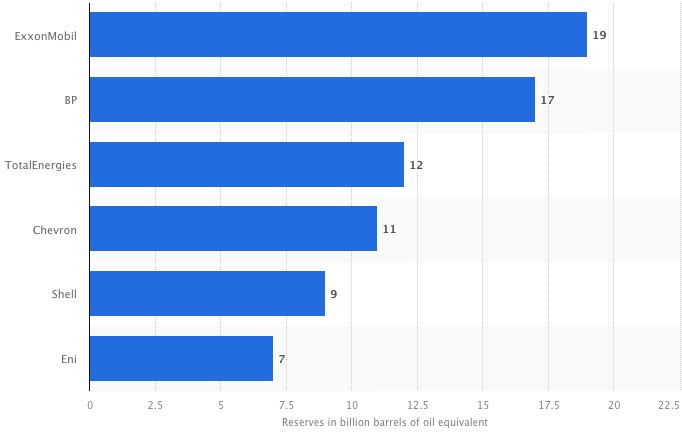

Quite than concentrate on the short-term, we’ll have a look at the long-term dangers for shareholders. First, upstream oil companies will ultimately enter secular decline because the world continues to transition to electrical automobiles. Oil demand is projected to peak someplace between 2025 and 2035. We have heard TTE’s CEO say he expects demand to peak in 2030, so no less than he is ready for this transformation. In the meantime, TTE’s present oil reserves will not final endlessly. This is a have a look at TTE’s confirmed oil reserves versus its opponents:

Confirmed Oil Reserves (Statista)

The Steadiness expects oil costs of $66 per barrel in 2025, $89 in 2030, and $132 in 2040. However, if the business begins investing closely in exploration and price reductions, there’s an opportunity oil costs may are available in on the low finish. Oil firms are terribly reliant on what the value of oil does over time.

Lengthy-term Returns

Our 2032 value goal for TTE is $151 per share, implying returns of 15% each year with dividends reinvested.

- We expect TTE can simply cowl its dividend whereas rising its normalized EPS at 5% each year, reaching earnings of $11.65 per share by 2032. We have assumed a 2032 oil value of $95 per barrel, permitting for some natural progress in TTE’s upstream enterprise. TotalEnergies’ quick rising LNG and renewables companies ought to offset declines in a few of its different operations. The corporate has ample money to purchase again shares at a charge of 1.5% each year, and to spend roughly $5 billion per yr on acquisitions. We have assigned a terminal a number of of 13x.

Conclusion

We actually like what we see with TotalEnergies, each from a administration and a valuation standpoint. This funding may ship market crushing returns of 15% each year. Take into account that TTE should construct out its renewables and LNG companies, and make investments its capital prudently to realize this consequence. This firm has a robust steadiness sheet, business main working prices, and a few very fast-growing income streams. We have analyzed lots of oil firms right here on Looking for Alpha, and TTE is up to now our favourite. If you understand of some hidden dangers we did not catch, please drop a remark down beneath. As for now, now we have a “robust purchase” ranking on the shares.